The Complete Risk Manager

Tight margins and “grudge purchases” don’t usually set the stage for positive relationships - especially when it comes to de-risking strategies. But what if they could?

Traditionally, businesses have viewed external risks as threats to be avoided and internal risks as operational challenges to be managed. By recognising both perspectives, organisations gain a more complete understanding of their total risk landscape and can develop stronger, more efficient strategies to mitigate it.

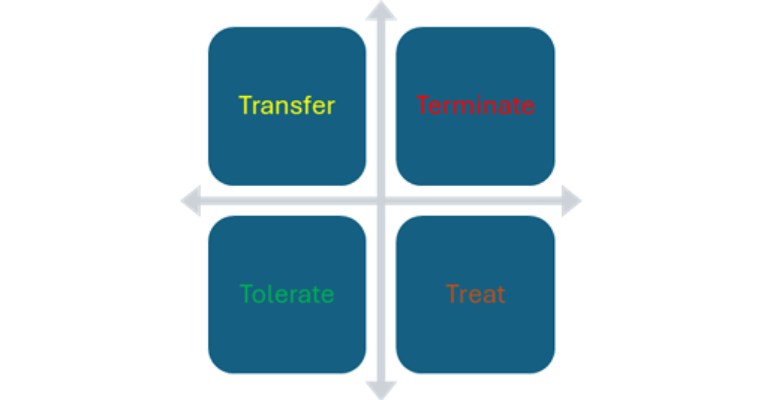

In this environment, the short-term insurance broker’s role has or at least should have, evolved to beyond policy placement. For many organisations, a broker functions as a strategic de-risking partner, analysing which risks are best to retain, transfer or reduce, or a combination of. This process typically involves three key steps:

- Risk identification - Analysing internal and external exposures.

- Risk quantification - Measuring their potential financial and operational impact.

- Risk management - Developing and implementing effective mitigation strategies.

While insurance remains a vital part of the de-risking framework, interpreting policy terms, conditions, limits and exclusions is rarely a simple process, where there is no one size fits all. A seasoned broker will be able to interrogate and translate the complexities into actionable decisions, advising the business on the various and the most appropriate options that are available. From here, your broker would be able to secure the best terms at a sustainable cost with policy wordings that is aligned with expectations, leaving the business with no unfortunate surprises at claims stage.

A critical challenge lies in aligning a business’s appetite for risk with the insurer’s willingness to accept it. The most effective brokers don’t just facilitate cover, they position risks strategically to achieve optimal cost-efficiency. In doing so, they become an integral part of an organisation’s overall risk strategy.

Defining the complete risk manager - The value of a broker goes beyond just premium savings, especially where such savings can leave gaps in cover. The value is derived from how effectively they can optimise the insured’s Total Cost of Risk (TCoR), the full cost of managing risk across the business. TCoR includes amongst other costs, premiums, retained losses, risk mitigation investments, administrative costs and opportunity costs. A well-managed TCoR program delivers long-term resilience, not just short-term premium savings.

To achieve this, three principles apply in an ongoing cycle:

- Clear risk definition - Objectively assessing risks in terms of likelihood and impact.

- Empowered advice - Enabling brokers to interrogate and advise on optimal mitigation and insurance strategies.

- Beyond insurance - Exploring non-insurance solutions, ensuring the program remains relevant, efficient and aligned with business objectives.

A complete risk manager challenges assumptions, quantifies exposures and helps the organisation evaluate each mitigation option’s residual value against its cost. This structured approach highlights where strategic investments can deliver the greatest results.

Example (Basic):

A warehouse with a loss exposure of R100 million could:

- Install sprinklers for R7 million (meeting insurer requirements but still leaving the Maximum Possible Loss (MPL) expected value at R100 million, while reducing the Expected Maximum Loss (EML) to R20 million. Alternatively, it might be feasible to:

- Add a fire wall and fire-rated doors for around R2 million, reducing the MPL exposure to R40 million, depending on where the wall is installed.

- Combine both for layered protection.

The best choice depends on the business’s risk appetite, and a complete risk manager ensures that choice is made with clear financial rationale.

“It’s not simply about lowering premiums; it’s about optimising the Total Cost of Risk. When the broker acts as a true strategic partner, risk becomes a business advantage, not just a grudge cost.”