Deciphering Dollar Declines

By: Izak Odendaal, Old Mutual Wealth Investment Strategist

Apart from a brief slump in April, global equity markets have mostly taken the policy chaos coming out of the US in their stride. The US benchmark S&P 500 is back at record highs, in part due to AI optimism, and also because investors still think that President Trump’s tariff threats are just bargaining chips. The trade deal with Japan and the EU is case in point, lowering tariffs from the 25% he had threatened to 15%. However, 15% is still very high, and if this is where US tariffs will settle across the board, it will raise the effective tariff rate on US imports to a level last seen in 1930.

It is notable that the US dollar has continued falling even as equities and to some extent bonds, recovered. This is despite economic theory suggesting that the currency of a country imposing high tariffs should strengthen since it will be importing less.

Why is this the case and what does it mean? We all know that the dollar is not like other currencies and there are at least three important lenses through which to think about the dollar’s relative position: its role as global reserve currency, its day-to-day use in global finance and commerce as well as its value in foreign exchange markets.

The demise of the dollar has long been foretold and feared, often in somewhat conspiratorial terms. As far back as 1968, an author by the name of William F. Rickenbacker published a book called the Death of the Dollar. It was not the last in a genre that often blames inflation and government borrowing for the impending disaster, but these days a deliberate policy of “de-dollarisation” by US opponents also figures prominently.

Reserved

Let’s start with the dollar’s role as a reserve currency. This simply means it is the main currency of foreign exchange reserves held by central banks and other monetary authorities. Countries hold foreign exchange reserves, including gold, as a sort of rainy day fund to ensure continuity in their international economic relations. This includes being able to service foreign debt, import necessary goods and services, such as fuel, and maintain confidence in the exchange rate. For instance, if importers cannot source dollars they need privately, or if a bank struggles to find dollars to repay a foreign loan, the central bank should be able to sell them the dollars (or euro or yen) in the interest of broader economic stability. With a stockpile of dollars, a central bank can also stabilise its own currency by buying it on foreign exchange markets.

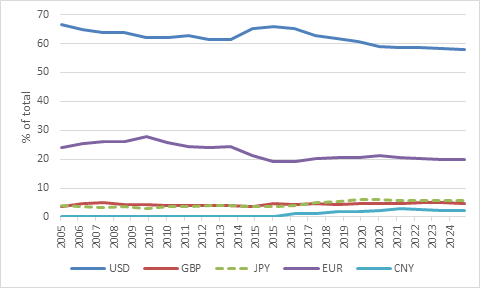

It makes sense, therefore, that the composition of foreign exchange reserves should broadly match a country’s international economic relationship. The dollar maintains the largest share of reserves, even though the US only accounts for around 9% of global trade. This is partly because a large percentage of global trade is still conducted in dollars (notably commodities), and partly because US capital markets are simply larger and more liquid than anywhere else.

Chart 1: Composition of global foreign exchage reserves

Source: International Monetary Fund

The accumulation of reserves globally increased dramatically in the wake of the Asian Financial Crisis of 1998 when countries in the region, spooked by massive capital outflows and economic devastation, started building up a stockpile of US dollars to ensure that their currencies would not come under speculative attack again. China, in particular, also accumulated dollars to prevent the yuan from appreciating too much, thereby undermining its export machine. However, the rapid growth in foreign exchange reserves has largely petered out since 2013. This is partly because the major central banks now offer swap lines to other central banks, meaning that the Federal Reserve, for instance, will swap dollars for other currencies in times of crisis, reducing the necessity for hoarding dollars.

Limited competition

The obvious competitors for the dollar as reserve currency, the Chinese yuan (also known as the renminbi) and the euro, each suffers from a major flaw, limiting their potential role. In the case of the euro, it is the lack of a large and liquid common bond market. Each of the 19 members of the euro have their own relatively small bond market and investors take on national credit risk in the process (Germany’s has a different risk profile to Greece and Italy, for instance). While there is a market for bonds issued by the European Union and backed by the joint fiscal capacity of member states, it remains relatively small. China, on the other hand, has a big bond market. The problem is that the yuan is not fully convertible and getting money in and out of China is not straightforward. As much as the Chinese government talks about a global role for the yuan, its policies still have the opposite effect.

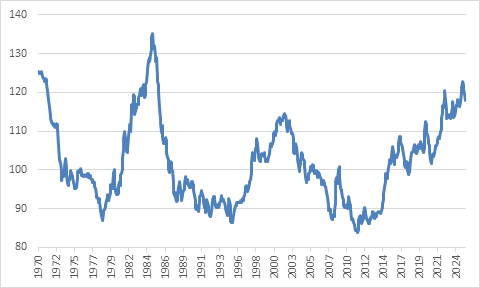

Central banks have increased gold holdings, but the gold market is also relatively small. All of this suggests that the ongoing decline in the dollar’s share of foreign currency reserves will be gradual. But does this matter? Over the past 12 years, the dollar’s share of global reserves fell and total reserve accumulation slowed. Nonetheless, the dollar’s exchange value increased as chart 2 shows, suggesting that reserve currency status has not been a major factor driving the dollar’s value. A gradual loss of reserve currency status could have an impact, but it also might not.

Chart 2: Real trade-weighted dollar index

Source: LSEG Datastream

Practicality, not politics

The second lens is the global use of the dollar by the private sector. This is mostly down to practicality, not politics. Imagine running a complex multinational company, with suppliers and customers spread across multiple countries. Being able to do business in a single currency saves time and cost. In many ways it is like the English language. That same multinational probably uses English extensively in its operations and communications even if it is headquartered in Sweden or Mexico. Having a common language that is understood across the world is immensely useful. This is what economists call a network effect. The more people who use the network (English, the dollar, a social media platform), the more useful it becomes to each individual user.

As a result, the dollar is used in the majority of global transactions to invoice and settle trade. The dollar also plays an important middle-man role in foreign exchange markets. If you want to swap Mexican peso into Swedish krone, there is a good chance that your bank will first exchange peso for dollars and then dollars for krone. Therefore, the dollar is in 90% of currency pairs traded, according to the Bank for International Settlements, a number that has barely budged over the years.

Digital currencies that settle instantaneously could replace the dollar in this role and reduce costs and time. However, there is limited movement on official central bank digital currencies, while stablecoins are touted as another alternative. However, stablecoins are linked to the dollar, and generally maintain their peg by holding dollar assets. They are not replacing dollars as much as repurposing them.

Many governments despise the dollar’s dominance, but it is private actors who mostly use it on a day-to-day basis. For instance, the Chinese government wants to globalise the yuan, as noted, but Chinese companies remain among the biggest borrowers of dollars internationally, and therefore continuously need to source dollars to service that debt. Inertia also plays a big role. For private actors to stop using the dollar in their day-to-day activities, there has to be a compelling reason, otherwise they’ll keep doing things the way they’ve done for decades.

Up and down

The third lens is the one that is most relevant for our purposes, namely the value of the dollar in foreign exchange markets. In other words, how many rands or euros or yen it costs to buy a dollar. It is of little concern to a South African investor how the central bank of India manages its foreign reserve assets, but the rand-dollar exchange rate matters a lot.

The exchange value of currency is set by the market as a result of millions of daily transactions, each with a slightly different motivation. Some of it is linked to imports and exports, some to capital flows (buying and selling financial assets), and a lot to speculation and trading. Interest rate differences matter, since higher current or expected future relative interest rates will pull in money, and vice versa. And of course, since a currency pair always involves two countries, it matters what is happening in the other country too.

The strength of the dollar over the past 15 years largely reflects stronger economic growth in the US, and consequently higher interest rates. This attracts capital. For a time, Europe and Japan had negative nominal interest rates, practically begging investors to go elsewhere. Moreover, the stunning outperformance of its large technology shares made the US equity market a must-own for investors across the globe. And as the dollar gained, it boosted the value of US investments for non-US investors (and similarly made international investments unattractive for Americans). Add in geopolitical risk, such as Russia’s war in Ukraine, and at the start of the year the real trade-weighted dollar index shown in Chart 2 was in the 95th percentile of its monthly values since 1970. In 50 years, in other words, it was only stronger 5% of the time. From this elevated level, there is naturally little upside and plenty room to decline.

Moreover, if it was any other currency, it would have fallen much further, much earlier, given the rapidly growing “twin” deficit, the combined shortfall on its current account and budget balances.

Chart 3: US current account deficit plus federal budget deficit

Source: LSEG Datastream

The catalyst for the decline so far this year was clearly President Donald Trump’s policies. Initially, the dollar rallied on his election, on the expectation that US growth outperformance would be given a boost. But since he has taken office, there is a lot about the Trump administration that has made investors nervous. This can be seen in the decoupling of the dollar from interest rate differentials as chart 4 shows – normally elevated US interest rates would have resulted in a stronger dollar. Instead, it has fallen 13% against the euro this year.

Chart 4: Dollar-euro exchange rate and interest rate difference

Source: LSEG Datastream

Apart from the tariff uncertainty, the big concerns for investors include the inexorable rise in US government debt levels and the independence of the Federal Reserve. Trump’s visit to the Fed’s headquarters last week was clearly designed to put renewed pressure on the Fed to cut rates.

Even when Trump departs the scene, deep political divisions in the US mean these issues are not going away anytime soon, and so the world’s overexposure to US assets no longer seems a sure bet. Recklessness in Washington can do much more for de-dollarisation than scheming in Beijing or Moscow, and international investors are rethinking their overweight allocations. This does not imply a mass exit from US positions, but more likely reduced inflows. It doesn’t mean that people will stop using the dollar or stop accepting it as payment. This is not the death of the dollar by any stretch of the imagination, but probably the end of a 15-year run of appreciation.

Nothing happens in straight lines, however, and if this is the start of a down cycle – as seems to be the case – there will still be dollar rallies. The extent of the cycle will also be limited by the fact that all other major currencies have problems of their own. A weaker dollar would benefit the world economy precisely because it is so widely used by businesses across the world. If it is cheaper to get hold of dollars to pay suppliers or to service debt, it is helpful. It also usually implies lower interest rates in other countries. It is no surprise that periods of strong performance in emerging markets have coincided with a weaker dollar. A weak dollar would also not be bad news in America, supporting exports and lifting the foreign earnings of multinationals.

For South African investors, the strong dollar environment of the last decade or so coincided with a falling rand. This boosted offshore returns and depressed domestic returns as global investors limited emerging market exposure. South Africa’s numerous own goals worsened matters considerably, but the dollar cycle played a big role. If that cycle has now turned, it implies less downward pressure on the rand. This definitely doesn’t mean that offshore exposure should be abandoned, but rather that investors should not bank on currency depreciation inflating their investment returns. Sensible diversification across local and global markets will remain important.