Investment Note: Shadows cast

By: Izak Odendaal, Old Mutual Wealth Investment Strategist

People across North America were treated last week to the spectacle of a total solar eclipse. It is a rare event where the moon briefly blocks out the sun, leaving only a slim halo (or corona) visible while day turns to night for a few eerie moments.

The sun is about 400 times larger than the moon but also much further away. When the moon is perfectly positioned between the earth and the sun, and closer to earth than usual, it blocks out sunlight over an area around 150km wide. This shadow is called an umbra.

Since the earth moves in a predictable orbit around the sun, and the moon around the earth, scientists can pinpoint when and where eclipses will take place. According to NASA, there will be 224 solar eclipses in the 21st century, of which 77 will be total eclipses. For any given location on earth, it can be hundreds of years between total eclipses, though partial eclipses happen a bit more frequently. There will be a partial solar eclipse over parts of South Africa in February 2026 and a total eclipse in November 2030.

In the investment universe, the sun is the US Federal Reserve (the Fed). Just as the planets revolve around the sun, so do all financial assets worldwide price off the Fed’s policy interest rate since US financial markets dwarf all others, and the US dollar is the global reserve currency.

Eclipses happen from time to time, where the Fed’s influence is overshadowed by other events or narratives, but its gravitational pull is ultimately overwhelming. Hence the old market adage, “don’t fight the Fed”.

Twin goals

The Fed in turn makes decisions based on achieving two objectives, stable prices, and maximum employment. The first is interpreted as an inflation target of 2%. The employment goal is a bit fuzzier, but a range of 3.5% to 4.5% unemployment is probably ideal. Above that, there are people who want to work but can’t find jobs; below that, there is a shortage of workers, and an overheating economy. This in turn could undermine the inflation goal.

Not all central banks have this explicit dual mandate. The European Central Bank, for instance, has only an inflation objective. The South African Reserve Bank’s mandate is stable inflation “in the interest of balanced and sustainable growth”.

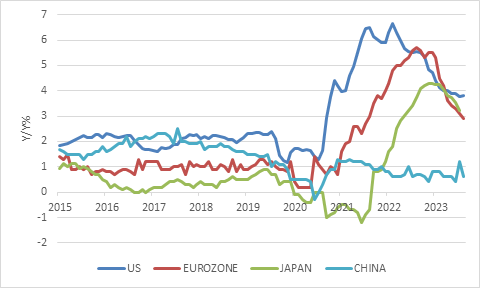

When inflation surged worldwide in the post-pandemic reopening, the Fed gave priority to the inflation objective. By hiking rates aggressively, it was prepared to cause rising unemployment (a recession) to return inflation to its target. Whether through luck or skill, consumer inflation has declined substantially from a peak of 9% in April 2022 to 3.8% in March without requiring sacrifices on the jobs side. In fact, unemployment remains low at 3.8% and the economy seems to be humming along.

Chart 1: Consumer price inflation excluding food and energy, %

Source: LSEG Datastream

Inflation declines in the last few months of 2023 were unexpectedly quick, leading to markets pricing in up to six rate cuts this year. Bonds and equities rallied, and the dollar pulled back. However, inflation in the first three months of this year have come in higher than expected and point to persistent price pressures in service categories.

This was always the fear. Solid economic growth means people have money to spend, which puts upward pressure on prices, while a tight labour market puts upward pressure on wages. When consumer demand is robust, companies can pass on wage costs. In many service industries – healthcare is a current pertinent example – salaries and wages are the biggest single input cost for businesses.

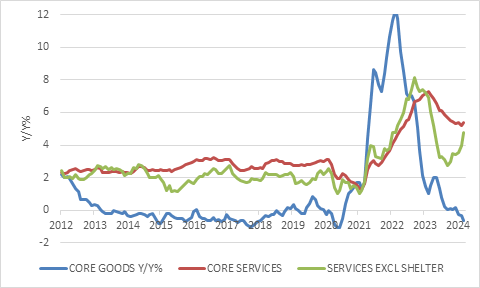

Goods price inflation remains low and is in fact still negative in many categories. Despite the Houthi attacks on Red Sea shipping and the recent dramatic bridge collapse in Baltimore, global supply chains are nowhere near as clogged up as in 2022. Goods inflation should remain under control, helped by falling Chinese factory prices.

Chart 2: US core goods and service inflation

Source: LSEG Datastream

The recent increase in oil and other commodity prices is a concern, particularly given the weekend’s dramatic escalation in the Middle Eastern conflict, but so far, the Brent oil price remains around $90 per barrel. The oil market response is nowhere near the scale of what happened immediately following Russia’s invasion of Ukraine.

It should be noted that the Fed actually targets another inflation measure, the personal consumption expenditure deflator. It is calculated differently to the consumer price index and usually increases at a slightly slower pace. In particular, it has a smaller weight to rental inflation, which has been particularly strong. Wage growth has also receded gradually over the past year.

Nonetheless, Fed officials repeatedly spoken about the need to have confidence that inflation is moving towards 2% on a sustained basis before they can consider rate cuts. The March inflation data will do nothing for achieving this confidence.

Therefore, US bond yields jumped, and the money market now only prices in two 25 basis points cuts this year.

Chart 3: US 10-year Treasury bond yield, %

Source: LSEG Datastream

Shrug

The equity market has largely shrugged this off. As long as US economic growth remains strong, it seems hard to imagine a deep Fed cutting cycle. But it also means that companies are still going to benefit from robust sales and be able to pass on cost increases, particularly wages, to consumers.

Profit growth in a strong economy might eclipse the impact of adjusted rate expectations. But profit growth expectations are already quite high. For the S&P 500, the consensus expectation for earnings per share is that it will be 10% higher by the end of this year compared to last, up 14% next year and 11% in 2026.

Moreover, there is the question of what is the appropriate multiple to put on each dollar of earnings. At 21 times forward earnings, the price:earnings multiple on the S&P 500 does not leave much room for disappointment. Given the highly uncertain macro environment – let’s face it, the consensus has swung wildly between underestimating and overestimated inflation – and increasing competition from fixed income yields, equity investors should surely demand a bigger margin of safety.

The other problem of course is that the longer interest rates stay high, the more pressure builds on the weak links in the US economy. For instance, mortgage rates are back above 7%, a level that might undermine the nascent housing recovery. Companies with fixed rate debt that were insulated against the initial rise in interest rates are vulnerable if that debt matures over the next year or so and must be rolled over at a much higher interest rate.

Now if real economic weakness were to show up, the Fed has a lot of room to cut rates from the current level of 5.5%. Inflation might still be on the high side, but it is low enough to give greater weighting to the employment side of the twin mandate. However, this turn of events would not be good for an equity market seemingly priced for perfection.

Jupiter

Other central banks largely operate in the Fed’s shadow. The European Central Bank has leeway to start cutting rates sooner, since inflation has fallen much. The one source of concern to the ECB is robust wage growth given labour shortages (unemployment is at a record low in the eurozone, despite a sluggish overall economic performance).

Therefore, while the ECB has kept its main interest rate unchanged at 4%, the highest level since its creation in 1999, it signalled at its policy meeting last week that rate cuts were coming.

However, as big and important an institution as the ECB is – it is a Jupiter in the monetary policy galaxy, not a little Venus – it is still constrained by the Fed’s decisions, even if its officials would argue otherwise. If its interest rates move too low relative to the Fed’s, the euro could fall and reignite inflationary pressures.

Notably, the Chinese inflation statistics, also released last week, went in the opposite direction to America’s inflation. Chinese headline inflation dipped to 0.1% year-on-year, while core inflation has been below 1% for all but three of the last 24 months. The People’s Bank of China might feel itself to be more immune to the Fed’s gravitation pull due to capital controls, but there has been pressure on the yuan nonetheless. This in turn is possibly one of the reasons its response to the property crisis has been rather tepid.

When it comes to South Africa, there is no question that the Fed looms large in the Reserve Bank’s thinking. The US inflation numbers interrupted a promising little rally in the rand last week (it wasn’t because of pre-election polls as some headlines claimed).

As the timing and depth of US interest rate cuts gets pushed back, the same is probably also true for local rates. In fact, the local money market is no longer pricing in any rate cuts this year, though such a view is probably overdone.

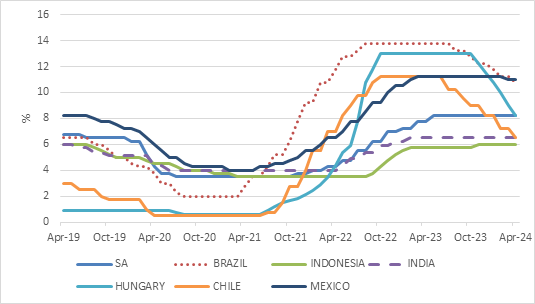

Chart 4: Emerging market policy interest rates, %

Source: LSEG Datastream

There is a notable exception to the usual Fed story. The big emerging market crises of the past few decades – especially the 1980s and 1990s – were caused by Fed cycles. There have been isolated cases of sunburn, with debt defaults by Sri Lanka, Ghana, Zambia and Argentina, a serial defaulter, but no widespread emerging markets contagion. Many emerging economies adopted floating exchange rates, built up foreign exchange reserves and reduced foreign borrowing. Some emerging markets hiked rates aggressively and early, even before the Fed got going in 2022. These countries, including Brazil, Chile and Hungary, are now in a position to cut rates as domestic inflation has declined, even though the Fed has yet to move lower. This counts as progress.

As they cut, South Africa’s short-term interest rates no longer seem relatively low in the peer group, and that should take some pressure off the rand.

Stars and cloudy skies

As noted above, celestial bodies move in predictable orbits. Economic cycles, driven by human needs, wants and capacities, not so much. The future is unpredictable and calls for a balanced investment approach. The comment Fed Chair Jerome Powell made in August, that central bankers were “navigating by the stars under cloudy skies” is still apt today for policymakers and investors alike.