Are there hidden risks lurking in your multi-asset fund?

Justin Floor, Head of Equities at PSG Asset Management

Multi-asset funds are a staple of the investment industry, both locally and abroad, where they are often exemplified by the 60/40 portfolio (60% equities, 40% bonds). Their popularity stems from the fact that they offer investors an integrated, diversified portfolio of assets, enabling the fund manager to adjust the portfolio composition as conditions change. This can help to manage investor behaviour and avoid emotional decision-making, which has been shown to have detrimental impacts on the outcomes investors ultimately achieve. These funds typically include asset classes such as equities, real estate, bonds, and cash. In some cases, they also offer exposure to more niche areas, such as private assets or commodities.

Despite their popularity, a closer look shows that many multi-asset funds rely on a rigid set of methodologies and assumptions in constructing and managing portfolios. While this approach has been successful in the past, it is less clear that it is suited to a rapidly changing environment that bears little resemblance to that of the past. Applying such methodologies and assumptions in a thoughtless manner, holds several risks for investors.

Risk #1: The fund is positioned too conservatively to achieve its long-term objectives

Investors tend to disproportionately weigh the importance of short-term pain over long-term gain. Considering that multi-asset funds are often key components of investors’ retirement savings, however, the importance of achieving enough long-term growth should be clear. Longevity and inflation are in many cases the primary risks for most investors, and those with sufficiently long time horizons should incorporate appropriate exposure to growth assets to ensure long-run objectives are achieved. Yet many growth-oriented multi-asset funds have been run too conservatively, prizing lower volatility over positioning for returns.

Riks #2: The fund manager is relying on outdated assumptions to construct the portfolio

The portfolio construction processes of many investment managers are underpinned by strategic asset allocation (SAA) models. These models often inherently assume the post-Global Financial Crisis (post-GFC) period from 2009 to 2019 provides the baseline for how markets and asset classes should behave. This reference period, however, coincided with globalisation, low and stable inflation, monetary policy dominance and very low interest rates, as well as negative bond and equity correlations. Zooming out, it becomes clear that this may have been an anomalous period.

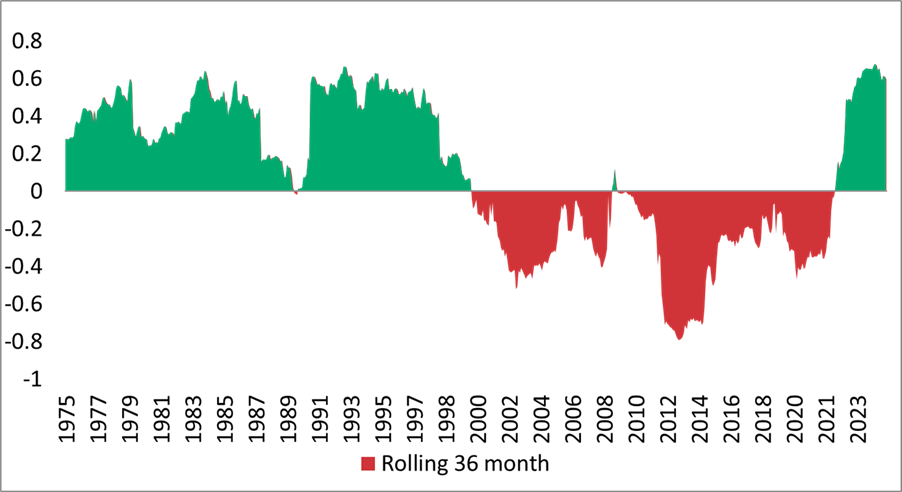

Today’s typical global 60/40 portfolio relies on this negative correlation between bonds and equities, assuming that dips in one asset class will be offset by gains in the other. However, historically this is only the case when inflation is stable and under control. More recently, bonds and equities have become increasingly correlated, with long duration bonds potentially amplifying equity risk instead of mitigating it. 2022 provides a key example of this, and the relationship is also more consistent with history. It’s the period from 2000 to 2019 that is the anomaly.

Rolling 36-month correlation between S&P500 and US bond total returns

Sources: PSG Asset Management and Bloomberg

Going forward, bonds should be owned for their income and return credentials, and not only for their portfolio hedging characteristics. Increasingly, investors need to look to alternatives that can act as portfolio diversifiers. This includes: select commodities (especially gold), inflation-linked bonds, infrastructure assets, special situation equities, and cash.

The typical SAA process also extrapolates historical returns and correlations into a mix of assets that would have delivered on the fund’s long-term targeted outcomes. Therefore, any large structural breaks in the environment could potentially leave investors unable to achieve their long-term goals.

Risk #3: The fund manager is equating volatility to risk

Many investors equate risk with volatility. This is understandable, as volatility is easy to calculate and manipulate into various financial and statistical models. While sometimes helpful, this approach does have several shortcomings. Some of these include that volatility is based on historical data and is therefore not always a reliable guide for the future (i.e. realised volatility can vary over time). Additionally, it does not distinguish between ‘good’ upside volatility and ‘bad’ downside volatility. Lastly, it is often used in models relying on normal return distributions, while research clearly shows that this is a poor proxy for the real-world distribution of outcomes.

PSG Asset Management prefers to focus on more meaningful risk measures like portfolio drawdown and time taken to recover. Focusing on maximum drawdown is a sensible alternative risk measure, in our view, given that it is the larger actual losses that inflict pain on investors. By focusing on managing overall losses, rather than short-term volatility, we believe we are able to deliver better long-term returns for our clients at appropriate levels of risk.

Ensure your fund is able to meet challenges head on

In 2025, it is becoming clearer that the future is likely to look very different and more chaotic than the relative calm of the preceding decades, which often anchor our expectations for investment outcomes and asset class behaviour. While the past can provide clues, there is no certainty about the future, and navigating an evolving and unpredictable environment successfully requires humility and an open mind. In this context, there is an opportunity to challenge some widely-held assumptions that often underpin multi-asset portfolios and investment choices. Appreciating when they are helpful and when they can be hazardous will increasingly be the difference between meeting investment goals or falling short of them.