Minding the gaps

Izak Odendaal, Old Mutual Wealth Investment Strategist

It is often said that nature abhors a vacuum. Meanwhile, financial and economic commentators distrust a gap. Whenever two variables that normally run together diverge, some explaining is required. Why did this happen, and what will cause convergence? Does one catch up, or the other catch down? Or are we witnessing a permanent misalignment?

If the latter, we are confronted with a case of “this time is different,” four words no investment professional utters lightly. Historically, many financial and economic data series show strong mean-reverting tendencies or persistent underlying trends. There are cycles, but these do turn eventually. That is the basis of using valuation as a framework for portfolio management, for instance, that cheap and expensive assets eventually drift back to fair value.

Jobless growth?

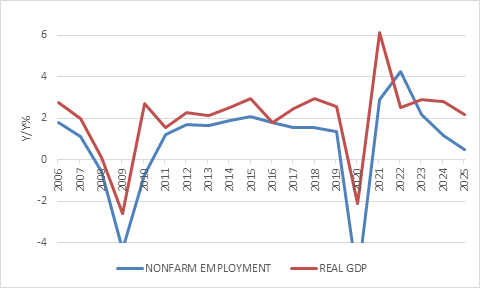

The divergence between US economic and employment growth is a recent example of such a gap, and also one that matters greatly to investors everywhere. The US economic and interest rate outlook remains the main driver of global market cycles. A US recession will pull global markets down, while an overheating economy can have a similar effect by leading to higher interest rates.

Growth in real GDP, the broadest measure of economic activity, was solid for most of 2025, though the fourth quarter was softer than expected due to the government shutdown. The economy grew 2.2% in 2025, but only added 181,000 new jobs on net, the slowest pace of job creation outside a recession this century. In contrast, 2024 saw 1.4 million jobs added. The first employment report of 2026 showed some improvement, but not strong enough to resolve the apparent contradiction between solid economic growth and weak jobs growth. Nor did the fourth quarter’s disappointing 1.4% annualised increase in real GDP.

In normal times, one would expect the gap to be closed by employment growth accelerating or GDP growth slowing further. Without job creation, it becomes difficult to sustain the aggregate growth in worker incomes needed to fuel broad-based consumption spending. However, these are not normal times.

Chart 1: US economic growth and job creation

Source: LSEG Datastream

The labour market has also suffered years of distortion. There were mass layoffs during Covid, but not long after companies were struggling to find workers in the wake of the “Great Resignation” even as the economy rebounded strongly. Many responded to disruptive labour shortages by clinging on to workers, preferring the risk of having too many rather than too few. Fast forward a few quarters, however, and this labour hoarding has left some firms overstaffed again, contributing to the weak hiring we saw last year.

Last year’s tariff uncertainty probably caused increased caution on the part of firms. This hasn’t resulted in layoffs, but rather in reduced labour demand. Meanwhile, the immigration crackdown has restricted the supply of workers. Since demand and supply are both lower, the unemployment rate has not moved much and remains historically low at 4.3%.

Finally, while data on the impact of artificial intelligence (AI) is still inconclusive, it is reasonable to assume that some companies are holding off on adding new staff while experimenting with automation. This would imply that the gap between employment growth and economic growth is a productivity miracle (more output with fewer inputs), rather than an anomaly.

AI is already used daily by hundreds of millions of people around the world, the fastest adoption of a new technology ever. However, daily use is not the same thing as becoming more productive in your job. In some roles and companies, that will be case, but it would be remarkable if economy-wide productivity gains materialised so quickly.

There is a very real possibility, however, that AI could weigh on employment growth in the years ahead. Over time, entirely new categories of jobs will emerge allowing overall unemployment to stabilise. However, the transition could be difficult. For young people entering the labour force, bewildering. The careers they prepared for could be vanishing before their eyes, and with it, the ability to build invaluable, life-long skills in junior roles.

Valuation gaps

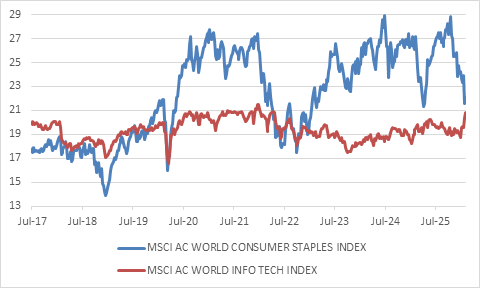

This brings us to a second prominent gap in equity valuations. Until recently, technology shares traded at a significant premium, partly driven by the excitement around AI, though it predates AI by some years. In essence, investors were prepared to pay up for businesses that were able to scale up without encountering diminishing returns, grow earnings rapidly and do so while remaining relatively asset light. Once software is written, it can be replicated infinitely and cheaply, unlike traditional “asset heavy” businesses where each unit produced requires significant capital investment.

Now, however, with the unprecedent levels of capex needed to sustain AI, this distinction starts to fade. If AI datacentres are not too different from the factories that produce cars, mobile phones, or potato chips, it is fair to ask if tech companies should not be valued somewhat closer to more traditional capital-intensive businesses. Especially since competition is likely to be fierce, including Chinese AI firms. These firms are not at the leading-edge of AI, but for most people and in many situations, they probably don’t need the best models.

In the broader tech universe beyond the big AI producers (several of whom are unlisted anyway, such as OpenAI and Anthropic), there has been a big sell-off as the lucrative business models of some software companies appear under threat from AI. The panic may well be overdone. Not all customers will build their own software, and these companies provide important services beyond software. They will also be able to utilise AI internally to enhance their own productivity. Even so, it still raises questions as to whether these businesses should trade at a premium.

Many investors have therefore rotated out of the tech sector towards consumer staples, industrials and other sectors usually derided as boring or old economy. These sectors have outperformed, and because the US has such a large tech weight, its benchmark S&P 500 index has lagged other markets.

Chart 2: Forward price: earnings ratios

Source: LSEG Datastream

Such rotations are normal, but can be quite turbulent. With overall economic growth in the US and the global economy likely to remain steady, there is no reason to fear that a rotation will lead to a collapse in share prices. The valuation gap between sectors has closed somewhat, as chart 2 shows, but leaves the overall global equity benchmark trading at 19 times forward earnings. This is well above the long-term average. There are many attractive shares in a global universe of more than 3 000 listed companies. However, at the index level, valuations point to more subdued returns over the next decade than in the past.

Meanwhile, there are good reasons why South African equities should trade at a discount to global equities, but the gap remains in the 80th percentile over the past 40 years. It has only been larger 20% of the time, in other words.

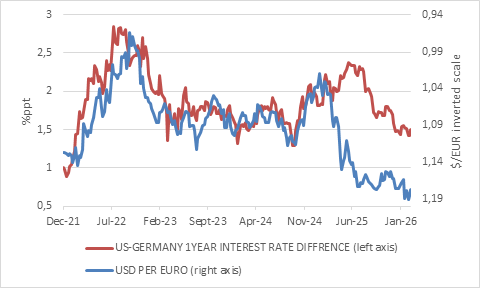

Chart 3: Dollar-euro exchange rate and interest rate differentials

Source: LSEG Datastream

Dollar gap

A gap between the US dollar and implied interest rate differences has also been striking and significant. Striking, because the difference between what investors can earn in one currency versus another is typically a key driver of the exchange rate between the two. Significant, because a weaker dollar over the past year has been a boon for emerging markets who tend to struggle when the greenback is strong.

In the case of the US, the timing of the wider gap unmistakenly coincides with the start of the Trump administration. Not only does the administration have a widely perceived preference for a weaker dollar since it could reduce the massive US trade deficit, but its approach to policymaking has spooked investors. In particular, the roll-out of steep trade tariffs on “Liberation Day” in April last year and the claims to Greenland this year have seen the dollar weaken as international investors, long used to a strong dollar boosting the returns on their US bond and equity holdings, rushed to hedge currency risk.

This doesn’t mean, however, that interest rate differences don’t matter anymore. If the US economy reaccelerates and the Federal Reserve’s stance on rates changes relative to expectations, the dollar could regain some lost ground.

Minutes from the January FOMC meeting, released with the customary three-week lag, show that there is disagreement on how officials view the central bank’s next steps. If inflation continues moderating, most members are happy to cut rates further. But most officials also indicated that they are less worried about the state of the labour market, suggesting little need for immediate stimulus in the form of lower rates. Data released on Friday showed the Fed’s preferred inflation measure, the personal consumption expenditure deflator (always a mouthful), rising to 2.9% year-on-year in December, while it was 3% excluding fuel and energy. This is above the Fed’s 2% target, but now that the Supreme Court has ruled much of Trump’s tariff regime unlawful, some of the upward price pressures should dissipate.

The ruling introduces fresh uncertainty, as Trump will try to reimpose tariffs through other legal mechanisms, but should still restore some of the trust international investors lost in the rule of law and separation of powers in America. At the same time, it raises renewed questions about the US government’s debt levels, especially given the roughly $30 billion a month in additional tax revenue form tariffs. When viewed from a long-term perspective, the dollar remains elevated, having only been stronger 17% of the time over the past 55 years on a real trade-weighted basis. From this lofty level, it should continue weakening over time, though this will not happen in a straight line.

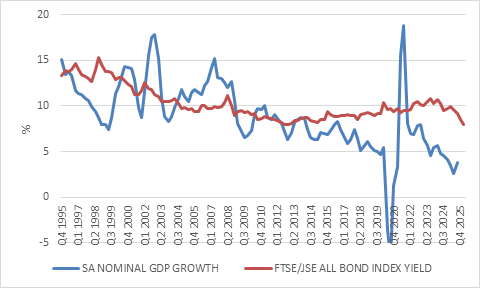

The fiscal gap

Finally, with Budget week underway in South Africa, the most important fiscal gap comes into focus. It is an old rule of thumb that bond yields should move in line with nominal GDP growth (real growth with inflation). This was the case in South Africa too, until around 2013, when the economic performance deteriorated sharply, and with it, government’s creditworthiness. The latter put upward pressure on bond yields, kicking off a vicious cycle since weaker growth meant lower tax revenues, further losses in creditworthiness, and higher borrowing which further depressed growth. We are in the early stages of closing the gap and reversing the vicious cycle. But to do so requires the Budget to stick to fiscal discipline while accelerating growth-enhancing reforms.

Chart 4: South African economic growth and bond yields

Source: LSEG Datastream

Behaviour gap

For the typical investor, the gap between expectations and reality also matters. When expectations are low, there is room for upside surprises. However, when expectations are too high, disappointment can set in.

Expectations are not just about returns, but also volatility. Anyone expecting a smooth ride from the markets will be disappointed and might sell out as soon as they get spooked. For most investors, this is the biggest risk to their long-term financial health, and not any of the macro factors commentators obsess about. Patience is therefore always important, as is not making portfolio decisions based on news headlines such as the current sabre rattling in the Persian Gulf. Investment writer Carl Richards coined the term “Behaviour Gap” to refer to the well-documented phenomenon that investor returns tend to lag fund returns due to switching, market timing and chasing performance. Unlike the gaps mentioned above, this is one that investors can control.