Momentum Investments Market review and macro-outlook summary January 2026

Herman van Papendorp, Head of asset allocation, Momentum Investments

Key economic outlook takeaways

- South Africa’s (SA) economy is expected to have expanded by around 1.2% in 2025, with growth projected to improve further to about 1.6% in 2026, marking a steady upward trend from the 0.5% outcome recorded in 2024. Local inflation is expected to drift slightly higher in 2026 due to base effects. But at an expected average of around 3.5% it should remain comfortably within the new 3% target with a ±1 percentage point tolerance band, which should provide scope for the SA Reserve Bank (SARB) to support growth by cutting interest rates further without compromising price stability. The rand is supported by firmer domestic fundamentals, ongoing terms-of-trade benefits from the combination of firm gold and platinum prices and a low oil price, as well as a soft United States (US) dollar. For a detailed economic outlook by our chief economist, Sanisha Packirisamy, please click here.

Key market review takeaways for 2025

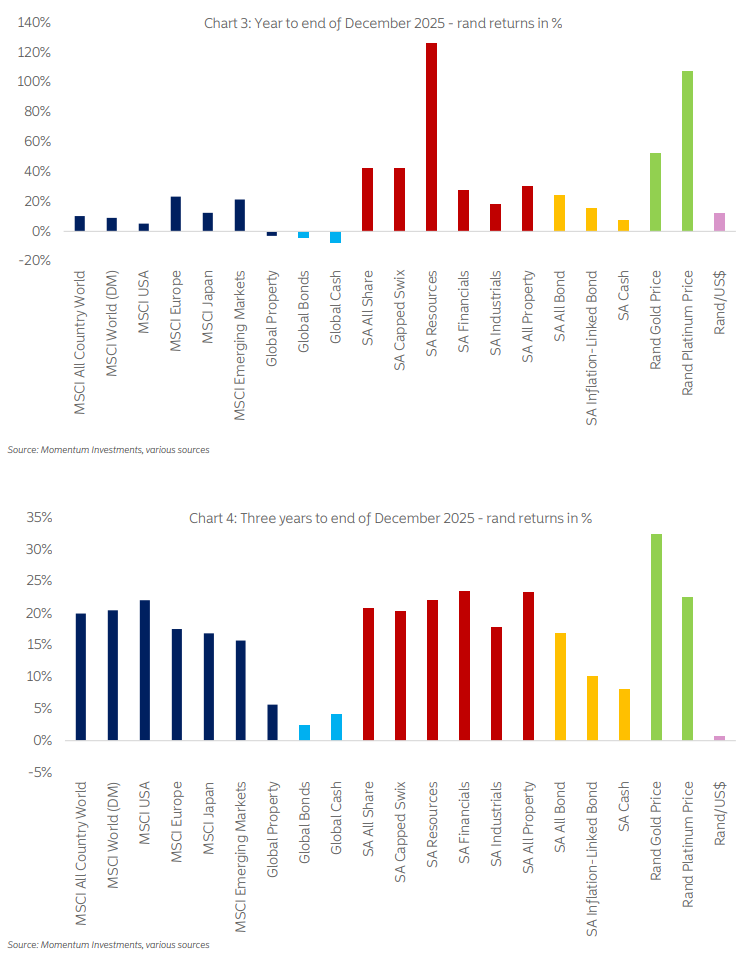

- Despite the heightened uncertainty induced by the second Trump presidency, 2025 turned out to be an exceptional year for SA investors due to rampant Platinum Group Metals (PGM) and gold prices, with broad-based strong absolute returns generated across asset classes, particularly among the local assets.

- Sharp rand appreciation on the back of rising gold and PGM prices and a weakening US dollar helped SA assets to provide superior returns relative to global assets for local investors in 2025. Within the global asset space, equities outperformed fixed income in 2025, with emerging market (EM) equities outshining developed market (DM)equities and Europe providing the best returns within DMs. Global cash was the worst-returning asset class in the year as interest rate cuts by central banks eroded returns.

- Although the strong showing by the SA resources sector was the predominant reason SA equities were the best performing main asset class in 2025, the SA financial and industrial sectors also played positive supporting roles, as the SARB cut interest rates and bond yields fell sharply. SA nominal bonds firmly outperformed inflation-linked bonds (ILBs) in 2025. SA listed property provided higher returns than the local fixed-income asset classes in 2025, on the back of the geared impact of lower local bond yields and accelerating earnings momentum. Cash was the clear lagging SA asset class in the year, as returns were eroded by local interest rate cuts.

Key financial market outlook takeaways

- Anticipated rising US inflation, fiscal stimulus measures, Federal Reserve (Fed) rate cuts amidst a potential threat to Fed independence, together with higher and more synchronised global regional profit growth in 2026, fundamentally favour global equities over bonds. Although US equities appear expensive compared to US bonds, they are likely to remain well supported as long as profit growth stays robust within a soft-landing environment. We have a cautiously constructive outlook for local asset class performance in 2026, underpinned by anticipated further rate cuts and modest growth acceleration from a low base. SA’s recent strong equity performance may help revive long-dormant foreign investor interest, as has already been seen in the SA bond market. With solid profit momentum, SA equities continue to screen attractively relative to global peers and to their own historical valuations. For our detailed financial market outlook, please click here

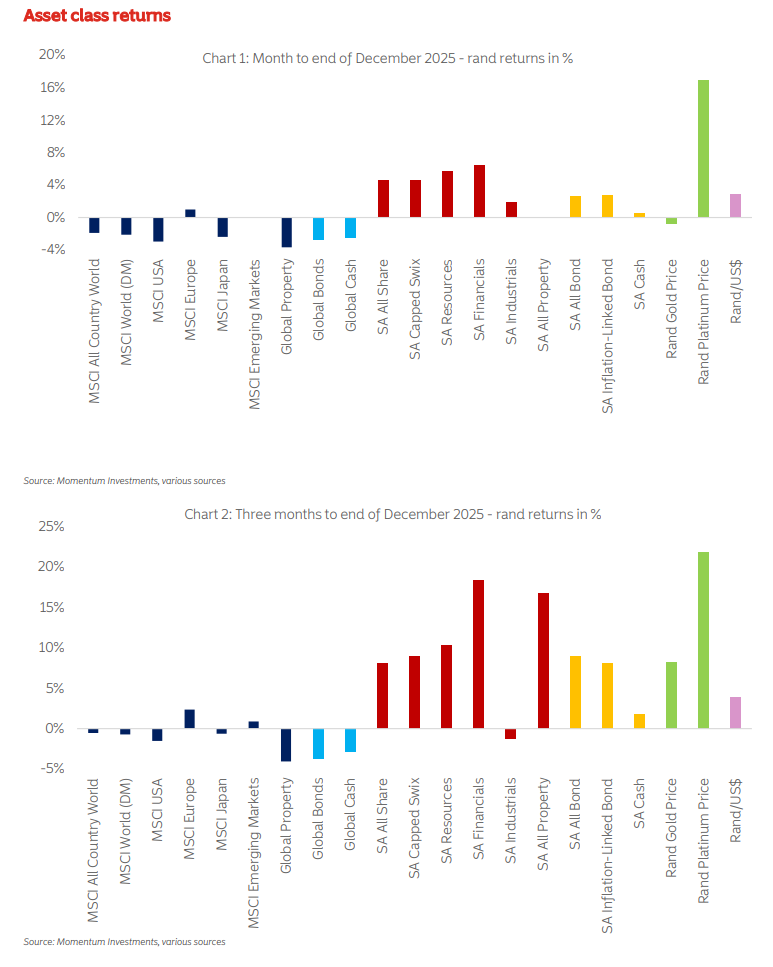

Despite Trumpolitics, 2025 was an exceptional year for SA investors due to rampant PGM and gold prices

The platinum ETF was the strongest-performing asset class in both December and the fourth quarter of 2025(4Q25) despite an appreciating rand, as supportive supply-demand fundamentals and the commodity’s increasing investment appeal as an alternative diversifier to gold in portfolios supported dollar platinum prices.

SA asset classes outperformed global assets in December and the 4Q25, partly due to commodity price-induced rand strength. Amongst global assets, equity returns outpaced those from fixed income in both December and 4Q25 as the Fed continued to cut interest rates, with global property providing the worst returns of all asset classes. Of all the main DM equity markets, only Europe gave higher returns in December and 4Q25 than EM equities.

Within SA asset classes, nominal government bonds provided slightly higher returns than equities and ILBs in the fourth quarter, with SA cash the clear return laggard. Falling local policy rates and bond yields made SA financials the equity sector winner in the fourth quarter, although sharp commodity price rises (particularly PGMs) also supported the resources sector. In sharp contrast, SA industrial shares gave negative returns in the quarter. SA listed property was the best-performing local asset class after the platinum ETF in 4Q25, driven by falling bond yields and positive profit momentum in the sector.

Despite the heightened uncertainty induced by the second Trump presidency, 2025 turned out to be an exceptional year for SA investors due to rampant PGM and gold prices, with broad-based strong absolute returns generated across asset classes, particularly among local assets.

The sharp rises in PGM, and to a lesser extent, gold prices in 2025 made the SA resources sector the standout return performer in the year. Ongoing geopolitical uncertainty throughout the year, rising expectations for Fed rate cuts, worries about the future independence of the Fed and a weakening US dollar supported gold prices and later PGM prices as an alternative to gold. Platinum also benefited from lowered expectations for future electric vehicle demand and its likely partial substitution by hybrid vehicles. Although the strong showing by the SA resources sector was the predominant reason SA equities were the best-performing main asset class in 2025, the SA financial and industrial sectors also played positive supporting roles, as the SARB cut interest rates and bond yields fell rapidly.

SA nominal bonds firmly outperformed ILBs in 2025 on the back of downside inflation surprises, the introduction of a lower inflation target and a decline in SA’s sovereign risk premium as the country was removed from the Financial Action Task Force’s (FATF) greylist and SA’s sub-investment grade sovereign rating was upgraded by S&P rating agency. These developments increasingly enticed foreign investor flows into the SA bond market as the year unfolded. SA listed property provided higher returns than the local fixed-income asset classes in 2025, on the back of the geared impact of lower local bond yields and accelerating earnings momentum. Cash was the clear lagging SA asset class in the year, as returns were eroded by local interest rate cuts.

Sharp rand appreciation on the back of rising gold and PGM prices and a weakening US dollar helped SA assets to provide superior returns relative to global assets for local investors in 2025, with only local cash lagging global equity returns. Within the global asset space, equities outperformed fixed income in 2025. Global equities were underpinned by resilient economic growth and profits, AI optimism, falling policy rates and a prevailing risk-on investor sentiment, with EM equities outshining DM equities and Europe providing the best returns within DM. Global cash was the worst-returning asset class in the year as interest rate cuts by central banks eroded returns.

Download the full market review PDF HERE