Outlook 2026: Decoupling driving resilient opportunities

By Nils Rode, Chief Investment Officer, Private Markets at Schroders

Resilience has become the key watch word for investors in an era shaped by persistent uncertainty.

In fact, in Schroders’ Global Investor Insights Survey for 2025, published in June, portfolio resilience was selected as by far the highest priority for investors for the remainder of 2025 and into 2026.

The surface calm of markets today – reflected in strong public equity market performance and benign bond yields – masks a complex backdrop. Inflation remains sticky, fiscal pressures are building, and geopolitical flashpoints continue to test global stability.

Even the enthusiasm around artificial intelligence, while transformative, risks fuelling new valuation imbalances.

Rising economic, political and financial uncertainties

Source: Schroders Capital, 2025. As of end of November 2025.

Periods like this challenge investors to look beyond short-term momentum and focus instead on the durability of returns – and on bottom-up value creation. In this context, private markets can be seen as a key area where cyclical and structural forces are aligning to create opportunity.

Decoupling creates opportunity

While many public markets are priced near record highs, private markets are at a different stage of the cycle. Fundraising, deal activity and exits have broadly all fallen over the past several years, which has fuelled a valuation reset across asset classes and segments.

This cyclical decoupling creates a healthier environment for new investments, supporting attractive entry prices and improved yield potential. Meanwhile existing portfolios have been largely insulated thanks to a focus on fundamentals and the robust, if volatile, macro backdrop.

At the same time, structural trends continue to drive where value is created. The global energy transition, reshoring of supply chains and ongoing digital transformation continue to provide tailwinds to long-term growth.

Differentiated resilience across strategies

Of course, not all private market strategies are positioned to respond equally to this environment. Resilient return opportunities thrive where a combination of inefficiency, disruption, differentiated risk and tangible asset-backing exist.

Think small buyouts or continuation investments in private equity, specialty finance and real asset debt within private credit, energy transition infrastructure, or select operational real estate.

As we move toward 2026, the most successful investors will be those able to combine steady deployment with selectivity. Private markets, with their long-term capital and active engagement, are not immune to uncertainty – but they are well positioned to contribute to diversified, resilient portfolios.

Private equity: Resilience through recalibration

Private equity continues to be in a period of recalibration. Fundraising and deal activity remain below pre-2022 levels, while exit routes have narrowed and holding periods have lengthened.

These cyclical influences, combined with tighter financing and persistent macro volatility, are reshaping the investment landscape. Yet rather than signalling weakness, this phase is restoring balance and discipline.

In short, lower competition, more selective deployment and wider dispersion in pricing are setting the stage for stronger vintages ahead.

From recalibration to resilience

The current market favours strategies that are able to harness three complementary sources of resilience: local champions, transformative growth, and multi-polar innovation.

- Local champions: Businesses rooted in domestic markets and which benefit from more stable demand, shorter supply chains and, as such, lower exposure to trade frictions. Their locally anchored earnings can help insulate portfolios from geopolitical shocks.

- Transformative growth: Companies where operational improvement, innovation, or complexity drive intrinsic value creation. As financial engineering gives way to hands-on ownership, value-add has become a decisive differentiator.

- Multi-polar innovation: Disruptive innovation is now distributed across, and driven from, multiple hubs – from the US and Europe to China, India and broader Asia-Pacific. This reduces dependency on any single market.

Three strategic areas of opportunity

These themes converge in three areas offering differentiated potential.

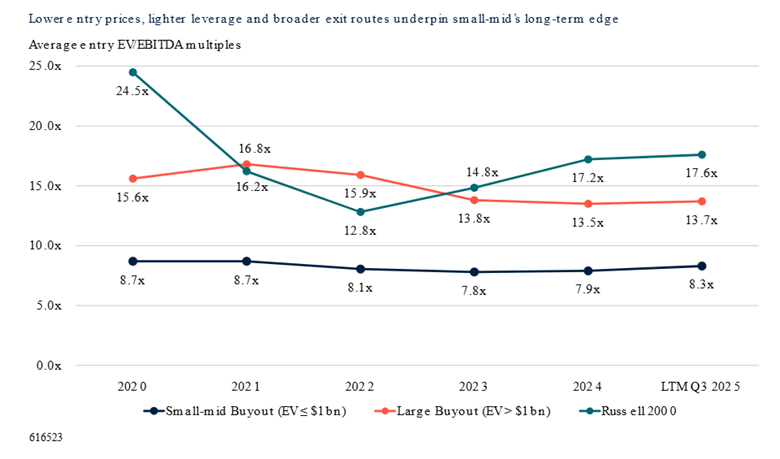

Small- and mid-market buyouts (for us, transactions with enterprise values below $1 billion) have become private equity’s resilience engine. With a concentration of capital driving up competition elsewhere, these investments offer attractive entry valuations that are on average 40–50% below large buyouts and listed small-cap public peers.

Small-mid buyouts trade 40–50% below large-cap and public benchmarks

Past performance is not a guide to future performance and may not be repeated. Source: Capital IQ, Bloomberg, Global M&A Outlook 2025, Robert W. Baird & Co., Schroders Capital, 2025. North America and Europe M&A. Completed deals. Russell 2000 EV/EBITDA is calculated using EBITDA from the latest trailing twelve months. The views shared are those of Schroders capital and may not be verified or might be subject to change.

Smaller buyouts also rely less on leverage – and more on operational agility and value creation. Most also target service-oriented, domestically or regionally focused companies, limiting exposure to global capital market swings and providing steadier exit routes through trade sales and sponsor transactions.

Continuation investments allow existing private equity owners to extend ownership of high-conviction assets and so access new phases of transformation growth. Slower exit markets have catalysed long-term, structural growth, enabling these vehicles to become an established, mainstream liquidity solution. We expect the market to grow to $300 billion in the coming ten years.

For investors, continuation investments align value creation with liquidity. They combine shorter holding periods (1.5 years less than traditional buyouts), with more efficient fees compared to sponsor-to-sponsor sales (secondary buyouts) and with more predictable historic returns.

Early-stage venture can capture the expanding geography of innovation. Beyond artificial intelligence, where rising valuations warrant later-stage caution, advances in biotechnology, climate technology, fintech and deep tech offer diverse entry points at more compelling valuations. The recent cooling of the biotech VC market, in particular, is opening contrarian opportunities.

Private debt and credit alternatives: Giving credit its due

Corporate and consumer balance sheets remain solid, despite some stress at the lower income or higher leverage end of the spectrum. At the same time, and as the focus of policymakers shifts from inflation to employment, central banks – led by the Federal Reserve – have adopted an accommodative stance.

This supports borrowers that finance at short-term rates, including smaller businesses and commercial real estate developers, and points to a relatively contained default outlook across much of the credit spectrum.

Meanwhile, after decades of very low interest rates and with a substantial transition of assets into the hands of more yield-oriented investors, such as insurers, income allocations are increasing.

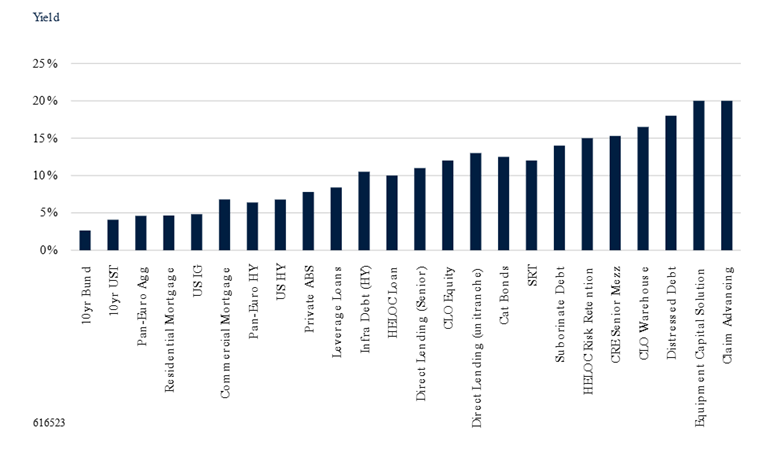

Thanks to this increased demand we see risk premiums compressing, particularly in syndicated markets. This means inefficient markets – including those that are secured, shorter tenor or where regulated banks or insurers have been more heavily involved – are increasingly more attractive.

A look at the continuum of returns

Source: Schroders Capital, Bloomberg. Pan-European yields are hedged to USD. As of September 2025. Shown for illustrative purposes only and should not be interpreted as a recommendation to buy or sell any security. Diversification cannot protect against the loss of principal.

Real estate debt: Repricing creates opportunity

After several years of adjustment, signs of stabilisation are emerging in commercial real estate. The steep price declines following the 2021–2022 peaks have largely run their course, with US property values broadly flat over the past year and select industrial and retail segments showing renewed strength.

From this lower base, and as policy rates begin to ease, transaction activity and demand for financing are recovering. This is coming at a time when banks have considerable pressure around their real estate exposure.

A meaningful gap therefore exists in both debt and equity capital provision, creating attractive opportunities for private lenders. Development, construction and heavy refurbishment bridge loans currently offer some of the highest return potential in real assets.

Infrastructure debt: The defensive income engine

Infrastructure debt continues to serve as a reliable source of stable, defensive income. With steady capital demand and tangible asset backing, it provides a secure foundation for long-term credit portfolios.

Many infrastructure projects benefit from inflation-linked revenues or regulated frameworks, which help preserve real yields even if inflation pressures re-emerge. In this environment, infrastructure debt remains one of the most effective ways to combine yield stability with downside protection.

Asset-based finance: Diversification through scale and structure

As investor demand for income endures, diversification has become increasingly important. Asset-backed finance offer access to large, scalable markets where inefficiencies support attractive spreads.

Specialty and consumer finance, in particular, continue to deliver compelling income opportunities supported by healthy consumer fundamentals and strong housing wealth. But it is important to stay within the stronger consumers, and within well collateralised assets.

These highly diversified pools of exposure also provide protection, with less exposure to idiosyncratic risks and stronger secondary market liquidity.

Insurance-linked securities: A true diversifier

Insurance-linked securities (ILS) remain a distinctive and resilient source of return. Their performance is driven by insured event outcomes rather than economic growth, offering valuable de-correlation to market and credit cycles.

Current valuations are attractive, as limited loss activity in recent years has enabled repricing and strong expected returns. In a broader credit context, ILS continues to provide an important stabilising force through uncorrelated performance and consistent income.

Infrastructure equity: Renewables remain a resilient opportunity

Energy transition infrastructure stands out as one of the most compelling long-term investment themes, offering potential for strong inflation linkage, secure income and premium growth, with the additional benefit of portfolio diversification through differentiated risk premia such as energy prices.

Decarbonisation and energy security

Global efforts to decarbonise, combined with heightened energy security concerns stemming from ongoing geopolitical tensions, continue to support renewable energy build-out. At the same time, cost-of-living pressures have reinforced the importance of energy affordability, with renewables now representing the most cost-effective source of new electricity in many regions.

Emerging technologies such as hydrogen, heat pumps, battery storage and electric vehicle charging infrastructure are critical to achieving deep decarbonisation in sectors such as transport, heating and heavy industry. In parallel, the rapid expansion of data centres and digital infrastructure continues to boost demand for clean, reliable power sources.

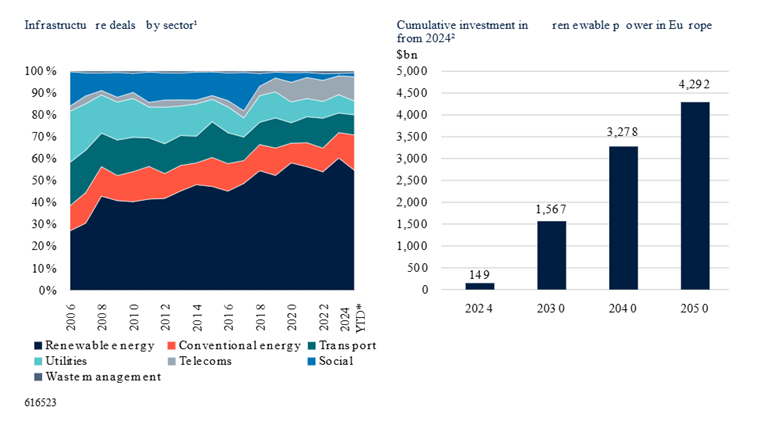

We currently see the strongest investment opportunities in Europe and Asia, where governments continue to strengthen policy frameworks and accelerate commitments to renewable energy.

In Europe alone, renewable infrastructure represents a base of roughly €600 billion, accounting for nearly half of infrastructure transactions. By the early 2030s, we expect to more than double to around €1.3 trillion, making renewables and energy-transition infrastructure the dominant asset class within the sector.

The US: Slower but steady transition

In the US, recent fiscal and budget legislation will phase out federal tax credits for renewables on a faster timeline, likely triggering a near-term surge in project activity as developers seek to secure incentives before they expire. Thereafter, we expect a moderation - but not a halt - in new wind and solar development.

The inherent cost competitiveness of renewables and ongoing demand for new generating capacity, reflecting powerful demand from areas such as data centres, should continue to underpin the long-term growth of US renewable infrastructure.

A buyer’s market creates opportunities

The renewables market has shifted decisively toward a buyer’s market. The recalibration of return expectations – driven by higher interest rates and reduced dry powder – has opened a capital supply-demand gap, creating attractive entry points for long-term investors.

Core and Core+ strategies remain well positioned, with equity return expectations up since 2024, with returns approaching (for Core) and exceeding (for Core+) the 10% mark.

We favour strategies focused on high-quality operating and construction-phase assets that offer strong cashflow visibility and the potential for enhanced returns through active management. Selectively, higher-return opportunities exist in emerging and ancillary areas, though we remain cautious toward early-stage developments.

The valuation dislocation between listed and unlisted assets has also spurred a wave of take-private transactions.

Past performance is not a guide to future performance. Source: Listed Greencoat fund quarterly reports Q1 2015 - Q1 2025 (Total Return Index NAV, (NAV + Reinvested Dividends). Past performance is not a reliable indicator of future results. There is no guarantee that this rate trajectory will remain the same in the near future. Discount rate refers to UK wind assets.

Real estate: Why we expect a compelling sequence of vintages

Following an extended period of price discovery and uneven adjustment, evidence is mounting that the global real estate market has reached an inflection point, with a recovery underway.

Our proprietary valuation framework indicates a growing share of attractively priced opportunities across multiple sectors and regions. As such, we believe that we are in the midst of a compelling sequence of investment vintages to deploy into the asset class.

We are particularly drawn to sectors where operational improvement can unlock alpha. This includes logistics, living and storage formats, and hospitality, which now offer meaningful pricing dislocations relative to their long-term income growth potential.

More recently investor sentiment has been aided by easing global tensions and greater certainty concerning the tariff environment.

Pricing correction – and uneven recovery – creates opportunities

Source: MSCI, 2025.

Supportive supply side

While our economic and rental growth expectations remain modest, a lack of supply continues to underpin operational performance.

Elevated construction costs and reduced debt availability have significantly slowed new project pipelines. We see increasing evidence of a “cost-push” impact on rents, with rising construction expenses driving rental increases to maintain development viability.

Should economies regain momentum, these dynamics could allow well-positioned assets to deliver real income growth. Tight supply conditions and growing construction costs, coupled with rebased valuations, are therefore laying the foundation for improved long-term performance.

Greater focus on asset specifics

Our preferred portfolio positioning has firmly shifted to a more neutral stance across sectors. This is owing to greater visibility on ‘rental floors’ within the retail and office sectors, as well as the elevated yields available for future-proofed assets. More broadly, we expect asset and micro location considerations, for example building sustainability profiles, to have a greater influence on relative performance going forward when contrasted with recent years, which saw record sector-level total return divergence.

The retail sector, after years of underperformance, has surprised to the upside, supported by improved operating models. Meanwhile, living and operational segments – such as rental housing, student accommodation, and healthcare – continue to demonstrate strong fundamentals, offering inflation pass-through and lower economic sensitivity.

Abundant recapitalisation opportunities

The current environment is catalysing compelling recapitalisation and secondaries opportunities across real estate platforms and other holding entities. These involve providing capital solutions to established management teams facing time and/or capital constraints in optimising value.

Opportunities are being further fuelled by favourable cyclical and structural dynamics – particularly the need to address operational complexity and sustainability requirements - and capital value declines that have exacerbated funding challenges.