“Sell America” trend continues as investors broaden out of US tech exposure

Investors are rotating out of the Magnificent Seven into the other 493 stocks within the US, while at the same time broadening their exposure to invest outside the US to the rest of the world. Sebastian Mullins, Head of Multi Asset and Fixed Income at Schroders Australia unpacks why this isn’t just worries over AI, but a global economic backdrop supportive of more cyclical allocations, despite recent developments in the Middle East.

By Sebastian Mullins, Head of Multi Asset and Fixed Income at Schroders Australia

Calm, lacklustre global equity returns in February hid a more volatile rotation beneath the surface. Global equities delivered a meek 1.4% in local currency terms and US equities fell 0.8%. But the rotation to the rest of the world was in full force, with countries like Japan delivering over 10% and the UK delivering 7% over the month. Even within the US there was significant rotation. The S&P equal weight index outperformed the market cap S&P 500 by over 4% for the month, information technology and consumer discretionary both fell over 6%, whereas energy and utilities rallied almost 12% and 9% respectively.

The rotation trade was in full swing, as jitters over AI spend caused the Magnificent Seven to dislocate, with companies like Amazon falling 12% but companies like Apple rallying almost 2%. US software companies continued to weaken as new releases from Claude caused many to question whether Software as a Service (SaaS) has a future.

This broadening out trade is gaining traction, both within the US along with investing outside of the US, as investors seek cyclically sensitive exposures. While some of this is driven by concerns over AI, we continue to believe the global economy is strong and will benefit those linked closer to the real economy and those that can benefit from higher inflation.

Government shutdown temporarily impacts US growth

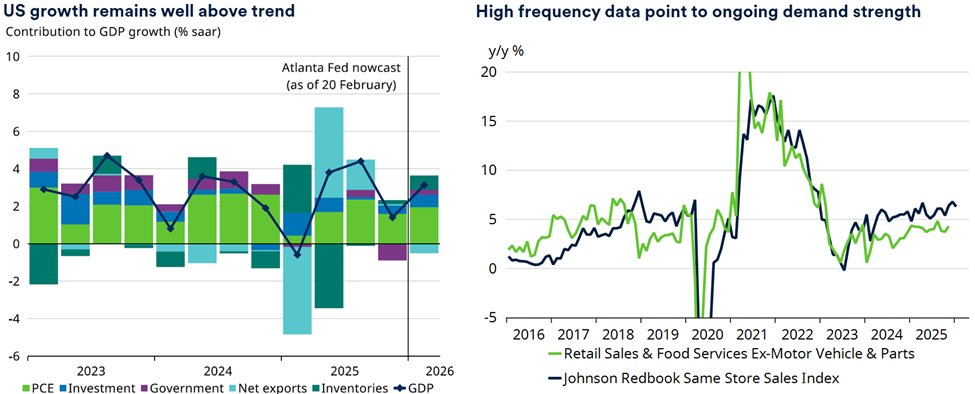

We have been vocal on the strong US economy for some time now. Real average hourly earnings remain strong at 1.2%, which is translating into continued consumption by households. Retail sales and food services, ex motor vehicles and parts, continues to be robust, which is being confirmed by the Johnson Redbook Same Stores Sales Index. This is keeping the personal consumption expenditure component of US GDP strong. The main hiccup to the view came from a lower than expected fourth quarter GDP print, which came in at 1.4% quarter on quarter, far lower than the expected 2.8%. However, the government shutdown detracted from the quarter’s growth, which is expected to be temporary and revert in the following quarter. Before the print, we calculated that the government shutdown would impact GDP by around 1-1.5% this quarter, similar to the initial survey. The Atlanta Fed GDPNow forecast remains strong with 3% expected currently in the first quarter of 2026.

Chart 1: US economy still strong despite 4th quarter hiccup

Source: Macrobond, Schroders Economics Group. 20 February 2026

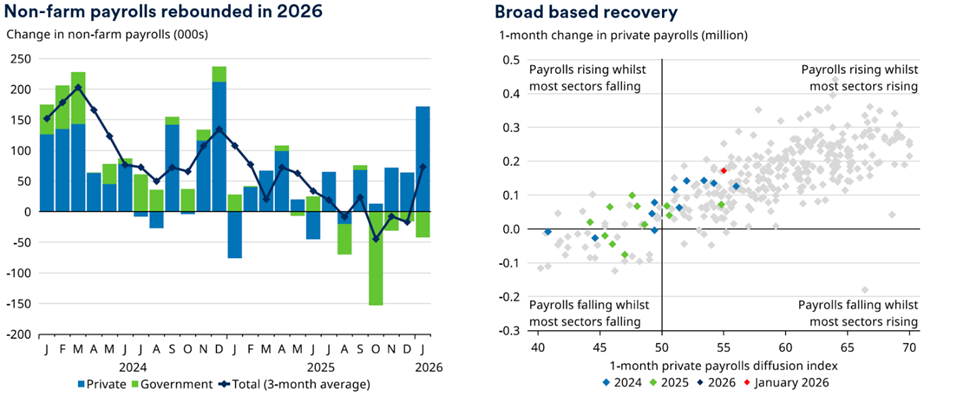

Payrolls finally rebound, but not without negative revisions first

The concern for many was that while real wages can keep consumption strong, this disappears if consumers start losing their jobs. The weak non-farm payroll prints seen ever since Liberation Day have caused many to question whether this was the start of a layoff cycle.

Whether it be high costs pressuring margins or the belief that humans can be replaced with AI agents, the lack of job growth has spooked the market. Our view was that corporates were merely waiting for more certainty over Trump’s protectionist policies. While there is unlikely to ever be certainty, corporates see a far brighter future than they did back in April 2025. We also saw 150k public sector job losses in October 2025, which was the delayed impact of Elon Musk’s Department of Government Efficiency (DOGE) program. However, in January this year we saw a market improvement with 130k new jobs being created, well above the 65k expectation. Pleasingly, this was mostly all in the private sector, showing a rebalancing of the economy from public to private and an improvement in private job needs. While some will say most of the job gains were in the health sector (which is true), job growth was seen across all sectors, implying a broad-based recovery. We will continue to watch jobs in the US, but our thesis remains the US economy will be strong in 2026.

Chart 2: Payrolls starting to pick up post Liberation Day uncertainty

Source: Macrobond, Schroders Economics Group. 15 February 2026

Middle East tensions – the black swan event?

Despite our optimistic view of the world, we have been de-risking over the last few weeks due to concern over the large troop build-up in the Middle East and lack of progress on the Iran/US negotiations.

We do not believe the tragic, recent Iranian attacks will be the black swan the market has been worrying about for years. The conflict appears to be very much dominated by the US – reducing the risk of this spiralling into something more dangerous. For now, we are looking to deploy cash if opportunities present themselves.

Important Information

This document is issued by Schroder Investment Management Australia Limited (ABN 22 000 443 274, AFSL 226473) (Schroders).

This document does not contain and should not be taken as containing any financial product advice or financial product recommendations. This document does not take into consideration any recipient’s objectives, financial situation or needs. Before making any decision relating to a Schroders fund, you should obtain and read a copy of the product disclosure statement available at www.schroders.com.au, or other relevant disclosure document for that fund and consider the appropriateness of the fund to your objectives, financial situation and needs. You should also refer to the target market determination for the fund at www.schroders.com.au. All investments carry risk, and the repayment of capital and performance in any of the funds named in this document are not guaranteed by Schroders or any company in the Schroders Group. The material contained in this document is not intended to provide, and should not be relied on for accounting, legal or tax advice.

Schroders does not give any warranty as to the accuracy, reliability or completeness of information which is contained in this document. To the maximum extent permitted by law, Schroders, every company in the Schroders plc group, and their respective directors, officers, employees, consultants and agents exclude all liability (however arising) for any direct or indirect loss or damage that may be suffered by the recipient or any other person in connection with this document.

Opinions, estimates and projections contained in this document reflect the opinions of the authors as at the date of this document and are subject to change without notice. “Forward-looking” information, such as forecasts or projections, are not guarantees of any future performance and there is no assurance that any forecast or projection will be realised. Past performance is not a reliable indicator of future performance. All references to securities, sectors, regions and/or countries are made for illustrative purposes only and are not to be construed as recommendations to buy, sell or hold.

Telephone calls and other electronic communications with Schroders representatives may be recorded.