Sovereign debt dynamics: the alarming backdrop to rising geopolitical risk

By David Rees, Head of Global Economics and Johanna Kyrklund Group Chief Investment Officer at Schroders

Behind the headlines that rattle markets daily is another, deeper problem: the enormous debts weighing down major world economies. Which countries are most vulnerable – and why is this so critical for investors?

Sovereign debt ratios have risen substantially across the world in recent decades, and ballooning budget deficits suggest that debt will continue to climb. While the period of ultra-low interest rates after the global financial crisis made it easier for governments to sustain large debt piles, the return to “normal” rates of interest has exposed poor debt dynamics in many economies that are also struggling to grow.

These gaping imbalances threaten to sow the seed for future recessions, and in the meantime are likely to have a major impact on the relative performance of sovereign bond markets and in turn wider financial markets.

Why this matters to all investors – by Johanna Kyrklund, Group CIO

Recent years have seen a shift towards populist policies, with a greater emphasis on fiscal policy as a source of demand management. Combined with the extreme effects on government finances of the pandemic, an ageing population and higher defence spending, national debt is rising rapidly in many of the world’s biggest economies and bond markets are getting more volatile.

This is likely to mean investors use bonds differently within their portfolios, focusing on their yield rather than their diversification properties, and that selectivity - the types of bonds we choose and when- becomes even more critical. The ability of bond markets to withstand higher government spending will also pose the ultimate constraint on populist policies. Overall, we see sovereign debt sustainability as a long term issue with potentially profound implications not only for investors but for wider society too.

How did national debt dynamics deteriorate to this point?

Sovereign debt positions have deteriorated almost everywhere in recent decades. The fall-out from the financial crisis of 2008 led to huge transfers from private to public sector balance sheets. The weak economic growth in the years that followed made it difficult for governments to repair the damage.

Public debt levels then took another leg-up during the Covid-19 pandemic as lockdowns and healthcare required huge additional government spending.

A series of recent bond market wobbles have placed the issue of sovereign debt sustainability squarely back onto the radar of investors.

In the UK, markets were rattled in September 2022 by short-lived premier Liz Truss’s mini budget that contained unfunded tax cuts. In France, in late 2024, political turmoil around budget negotiations upended the bond market. In Brazil in 2024 and into 2025, the Lula government’s populist spending plans forced the central bank into making aggressive interest rate hikes.

Meanwhile, the May 2025 downgrade of the US’s sovereign credit rating by Moody’s was a timely reminder of poor US debt dynamics at a time when the Trump administration is trying to deliver yet more fiscal stimulus.

Looking ahead: national debt levels into the future

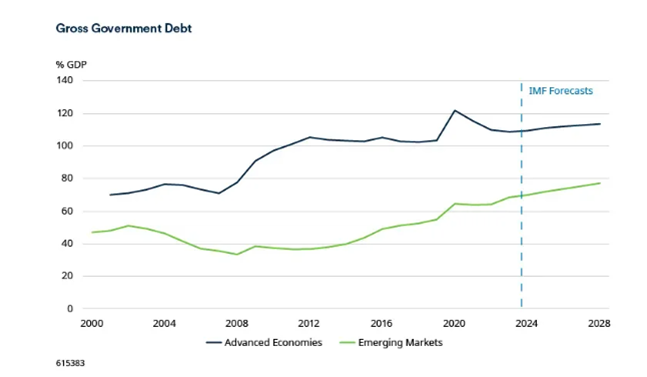

With many major sovereigns still running large budget deficits, the International Monetary Fund (IMF) expects government debt to climb even further in the years ahead to around 100% of global GDP. Within that, gross government debt is expected to touch 250% of GDP in Japan and continue to climb further above 100% of GDP in the US, Italy, France and the UK.

Health and social spending has increased significantly in recent years and ageing populations in most major economies will add to those requirements, while draining the tax base. Meanwhile, questions over future support of Ukraine’s resistance to Russian aggression is likely to see defence spending in Europe rise significantly.

While government borrowing is not necessarily a bad thing, it depends what the money is spent on. Whereas borrowing to invest in infrastructure projects can increase the supply potential of an economy and underpin future economic growth, markets tend to take a dim view of governments that use debt to fund current spending that delivers little return in the long run.

The changing face of debt sustainability

As in the business world, it is cash flow that kills you: the ability to service external debt. A common factor across historic emerging market debt crises has been that short-term external debt has often climbed to 200% or more of foreign exchange reserves. Effectively, given high shares of foreign currency-denominated debt in external obligations, governments ran out of hard currency to service debts.

Debt dynamics are now more about the interaction between government budget balances, economic growth, inflation and interest rates. When these factors get out of kilter, poor debt dynamics can lead to abrupt increases in long-term interest rates that cause both financial market and economic dislocation.

The return of “normal” interest rates

The return to “normal” levels of interest rates has caused governments a major headache as debt servicing costs have climbed, calling into question the sustainability of fiscal positions. The Covid-19 pandemic forced governments to deliver large fiscal stimuli that finally snapped the world out of the post-financial crisis era of low inflation and low interest rates. The burst of activity as economies reopened, coupled with supply chain disruptions and geopolitical tensions, led to a surge in inflation that has yet to be beaten.

As a result, interest rates have risen significantly.

Ranked by risk: which specific countries are most vulnerable to fiscal stress?

With debt positions unlikely to significantly improve in the foreseeable future, and new structural changes in the economy such as deglobalisation, decarbonisation and demographics likely to pressure inflation, interest rates and public spending for many years to come, it makes sense to think about where fiscal vulnerabilities lie.

To do this we have built a framework for assessing sovereign debt vulnerabilities. This draws on some components from Schroders’ emerging market debt team’s country risk model, which has been used in their investment process for more than 20 years. We have not incorporated all, as debt dynamics can differ between emerging and developed markets. Our focus is the G20, capturing the most significant global economies, and covering both developed and emerging worlds.

Who are the most vulnerable economies? It is striking that on the basis of our framework, debt dynamics are more of a concern in developed markets than emerging markets. That marks a major turnaround from the past.

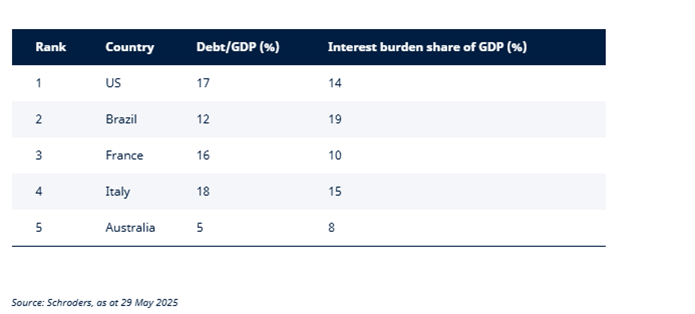

Of the top five countries that have the worst score, four are developed markets – the US, France, Italy and Australia (with the UK just below in sixth). Of emerging markets only Brazil makes the list.

Another striking point is just how bad debt dynamics are in the US. Large, twin current account and budget deficits mean that the US is reliant on foreign capital inflows to sustain its debt pile.

Below we show just the five countries most at risk, ranked on the 11 metrics that make of our debt vulnerability framework. The complete table showing all 20 countries, and incorporating the different risk metrics, is included in the full document, linked here and below.

Sovereign debt risk – scorecard showing the five countries most at risk

Germany ranks as the least vulnerable economy in the G20. Post the financial crisis, a constitutional amendment was imposed that limited the government from adding more than 0.3% to debt per year. The problem for Germany is not debt but growth – indeed it is growth which has been causing political crisis in Germany, not debt dynamics.

What options do governments have when faced with fiscal stress?

Governments facing fiscal stress have several levers they can pull to improve debt dynamics. The option chosen can have major consequences for growth, inflation, and asset prices. In essence, these involve either reducing the numerator (debt) or increasing the denominator (nominal GDP) of the public debt ratio. There are four key strategies:

- Fiscal Consolidation: This comprises austerity measures such as tax increases and spending cuts to reduce primary budget deficits. While markets may initially cheer these measures, they often fail to improve debt dynamics due to reduced nominal growth and have potential to stoke social unrest.

- Faster GDP Growth: By increasing nominal GDP governments can reduce the debt ratio and increase tax receipts. Investment-led fiscal stimulus can boost productivity and drive non-inflationary growth, but it's rarely an option for debt-constrained governments. Reforms and deregulation can also help, though they take time to bear fruit.

- Inflation or Financial Repression: By allowing inflation to run above target, governments can reduce the real value of debt. However, this is unpopular and complicated if a country has a lot of inflation-linked debt, such as in the UK. Financial repression, such as yield curve control, can depress interest rates on government debt. But this can crowd out other investments and may require increasing the money supply, which risks inflation.

- Restructuring: Governments could default on their debts and seek support from global institutions like the IMF. This often relates to the willingness to pay rather than the ability to pay. Rising populism increases the risk of defaults, which tend to come in waves after significant global events.

Ultimately, the option or combination of options chosen will depend on various domestic and external factors. The global shift towards populism raises the risk of policymakers pivoting away from conventional policies to more radical solutions, potentially leading to unintended economic and market outcomes.

Read the full paper: Government debt dynamics are flashing red: we assess who is vulnerable