The end of the lost decade

Izak Odendaal, Old Mutual Wealth Investment Strategist

Several countries have used the term “lost decade” to describe periods of stagnation, Britain in the 1970s, Latin America in the 1980s (“La Década Perdida”) and Japan in the 1990s and 2000s. South Africa’s own lost decade, give or take a few years, started in the mid-2010s. From the pride and excitement of hosting the 2010 FIFA World Cup, things started going downhill not long after, culminating in in the devastation of the Covid pandemic, the shame and fear triggered by the July 2021 riots, and the frustration of sustained stage 6-loadshedding in 2022 and 2023.

Some of what went wrong in South Africa’s lost decade was due to global factors, including the pandemic, volatile commodity prices, a stronger dollar and capital outflows from emerging markets. However, this was severely compounded by bad policy choices, deteriorating governance, rising systemic corruption and the hollowing out of institutions meant to check the abuse of power. This casted a long shadow over financial markets and the broader economy suffered in tow. In that regard, tomorrow’s 10-year anniversary of ‘Nenegate’ is significant and provides a marker to date the lost decade. It was the moment when both local and international investors realised, without doubt, that something was fundamentally wrong.

It was, however, also the beginning of the end for President Jacob Zuma. When he fired finance minister Nhlanhla Nene for resisting the looting of the fiscus on 8 December 2015, the market reaction was fierce. Bond prices crashed, causing a spike in government borrowing costs, and the rand slumped. Zuma was forced to backtrack on the appointment of Des Van Rooyen as Nene’s replacement. The “bond vigilantes” played as big a role as any other group to undermine his power and finally remove him from office, allowing the process of repair to begin.

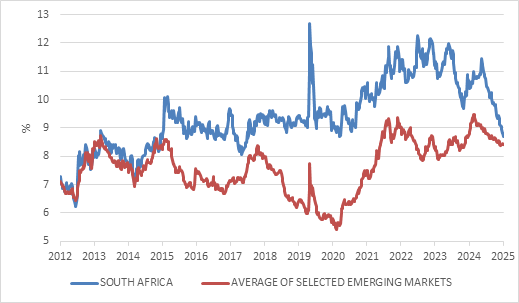

South Africa was not only downgraded by ratings agencies after Nenegate, but was instantly downgraded by the markets, and started trading at a discount to its peer countries. Chart 1 compares the borrowing costs of the South African government with a handful of emerging market peers across four continents. A very distinct gap opened after Nenegate that persisted for the subsequent decade. Covid hit South Africa particularly hard and the gap widened again in 2022 even as reforms were underway. The consequence of earlier mismanagement – notably loadshedding, a logistics crisis and elevated government debt levels – proved to be persistent.

Chart 1: 10-year local currency government bond yields

Source: LSEG Datastream

Today, however, things are looking up again. These reforms are bearing fruit. The country has not experienced severe loadshedding since early 2024 and painful fiscal consolidation has eased anxieties over government debt levels. A few weeks ago, S&P Global upgraded South Africa’s credit rating. Moody’s did not follow suit at its scheduled review on Friday but will likely come round eventually. Though there is much work to be done in improving governance and fighting corruption, the removal from the FATF grey list is another marker of improvement. The gap between South African and peer country borrowing costs has now basically disappeared — a decade after it first opened.

We can tell a similar story about the rand. All emerging markets currencies weakened against the dollar over the past decade-plus, but the rand fell especially sharply for all the reasons outlined above. This is partly because the rand is a highly liquid currency, which means it tends to be hit hard by periods of global risk aversion, such as in 2020. However, it is also because South Africa simultaneously ran large current account and fiscal deficits, earning us a place in the “Fragile Five” club around 2014. This “twin deficit” which must partly be funded by capital inflows, has now stabilised, with South Africa running a surplus on the primary (non-interest) fiscal balance and the trade balance (meaning that exports exceed imports).

Derating

As for the equity market, it is a mixed story since many large JSE-listed companies have little exposure to the local economy. We’ve also seen the significant boost from gold and platinum miners over the past year, which is simply luck and not something any South African can claim credit for. Indeed, the local mining environment remains difficult from a regulatory and operational point of view. However, the modern economic history of South Africa has always featured such periods of commodity price windfalls and a positive economic outlook will always include positive international tailwinds, or at the very least, the absence of global headwinds. The contrary is also true. A broad commodity price crash, like the one experienced between 2013 and early 2016, caused immense damage and compounded all the other problems.

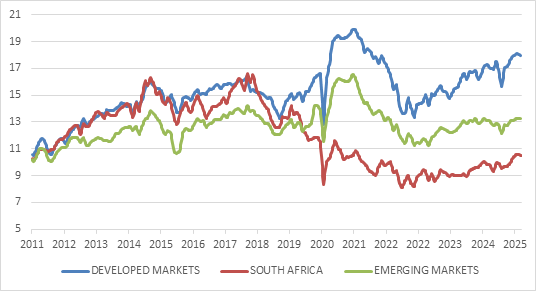

Chart 2: Forward price: earnings ratios

Source: LSEG Datastream

South African equities traded on a similar price: earnings multiple to developed and emerging markets prior to 2018 but suffered a severe derating thereafter. This was a substantial drag on returns. The derating was driven by sector-specific issues, but also broadly because global investors demanded a greater margin of safety for deploying capital here while locals were still desperate to get their money out. Many South African companies made acquisitions abroad over the past 10 or so years with limited success. Arguably the greatest local corporate scandal, the collapse of Steinhoff in 2017, was driven in part by this trend. Investors were prepared to overlook corporate governance concerns to piggyback on the company’s rapid international expansion. Reserve Bank numbers show a cumulative R480 billion net acquisitions of foreign assets by domestic firms between 2013 and 2019. This trend of offshore acquisitions at the cost of domestic investment, which seems to have turned, was both a consequence of and contributor to a period of economic stagnation.

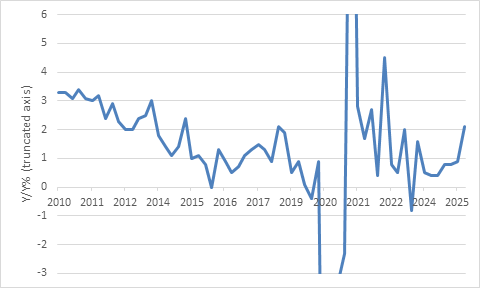

South Africa’s real economic growth rate averaged 2.8% between 2010 and 2013, but downshifted dramatically from 2014 onwards to average only 0.7% over the subsequent decade. This is lower than population growth of around 1.3% per year, meaning the country has been getting poorer on a per person basis.

Chart 3: SA real economic growth

Source: Stats SA

2025 is already looking better, despite headwinds from US tariffs. Third quarter real gross domestic product (GDP) was 0.5% higher than the second quarter. The third quarter of 2024 was particularly weak, flattering the year-on-year growth rate somewhat. Household spending has recovered strongly from a period of high inflation and high interest rates, hitting 3% year-on-year. Looking ahead, real growth in household spending is likely to ease slightly from its current high base to around 2%. For overall economic growth to continue rising, fixed investment spending must rise.

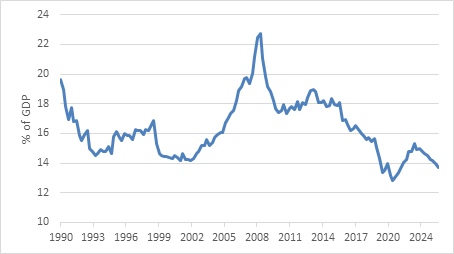

It has been depressed for several years as a lack of funding has limited public sector capex while low business confidence, policy uncertainty, infrastructure bottlenecks and the focus on international expansion as discussed above have weighed on private spending. Fixed investment averaged around 18% of GDP between 2010 and 2015, but in the wake of Nenegate it collapsed sharply to 14%, well below the 25% to 30% level needed to sustain rapid economic growth.

Chart 4: SA gross fixed capital formation (fixed investment)

Source: SA Reserve Bank

To turn this around, the Budget is gradually shifting the mix of spending from salaries to capital spending, while efforts are underway to unlock private investment in infrastructure. This is not straightforward but a priority for government. Experience in other countries shows that once the blueprint has been established for crowding private capital and expertise into infrastructure projects, it can be rolled out at speed and scale. Private companies should also increase investment in their own businesses when they become more confident about growth prospects. Lower borrowing costs will also help.

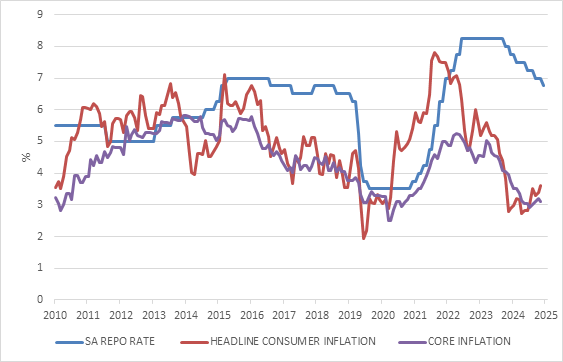

Tight money

Monetary policy has been tight over much of the past decade, apart from the emergency rate cuts when the pandemic hit. The Reserve Bank hiked the repo rate by 50 basis points at the first monetary policy committee meeting after Nenegate in January 2016 and arguably kept interest rates high even when inflation started declining. It was essentially forced to be the grown-up in the room and provide policy credibility where none was available from other branches of government. To put it simply, it kept rates elevated to prevent destabilising capital outflows and an even worse collapse in the rand.

Chart 5: Inflation and interest rates

Source: LSEG Datastream

However, two developments mean the outlook for interest rates is better. Firstly, with fiscal policy credibility improving and the twin deficit narrowing, the country risk premium is lower, allowing the Reserve Bank to focus on domestic inflation dynamics. Secondly, if the 3% inflation target can be achieved, interest rates will naturally decline. The repo rate has already fallen from 8.25% to 6.75% over the past year and is likely to continue declining gradually. This will further support economic growth and a rerating in South African assets.

Sense and sensibility

Clearly maintaining a positive economic and market outlook will depend on sensible politics and government policies. Coalitions are now a reality at the national level and will remain so for the foreseeable future. This makes extreme policies less likely. The current coalition, a self-styled government of national unity (GNU), has been welcomed by the market for its focus on the rule of law, improving governance and raising economic growth. While there is disagreement within the GNU about how to achieve its goals with likely missteps along the way, there is broad consensus that the country needs sustained faster economic growth and sustainable government finances. Whether the GNU will see out its full term remains to be seen. Local government elections late next year or early 2027 will be a key marker in how the political landscape is changing.

Either way, a crucial pivot that predates the GNU is the ANC’s realisation that it should encourage private investment, rather than clinging on to state monopolies. This mind shift was arguably brought on by the severity of the electricity crisis, but the success in ending loadshedding has given it credibility and it is now embedded in official ANC policy. The party will choose a successor to President Ramaphosa in late 2027 (and not at this week’s National General Council) and this is a source of unease for many investors. However, a drastic change in policy seems unlikely, especially if current policies show results. Moreover, whoever succeeds Ramaphosa will still have to operate in a coalition with other parties.

Politics in South Africa will remain noisy and the downside of coalitions is that they can be unstable and indecisive. Future coalitions might include populist parties, but no one will have the full say and all parties will have to compromise, meaning destructive policies are less likely. The likelihood of one person concentrating power in their hands again is slim. And even if they do, we have now seen how the courts, other democratic institutions and ultimately the markets present checks and balances.

Direction of travel

Serious challenges remain, particularly the dysfunction in many municipalities and parts of the criminal justice system, as highlighted by the Madlanga Commission hearings. Unemployment also remains much higher than in any comparable economy. However, there is a difference between how smart investors think and the way most other people do. The latter will look at a situation and ask if it’s good or bad, while investors will ask if it’s getting better or worse. They care about the direction of travel and what it is priced in. In the case of South Africa, the evidence keeps piling up that things are improving. Local bonds, listed property, and equities have delivered phenomenal returns of 22%, 29% and 36% respectively. Despite this, domestic asset classes can still benefit from better fundamentals and sentiment over the longer term. Sensible diversification will always remain important because the future is uncertain, and many things can still go wrong. Broadly speaking, South Africa’s lost decade is over, a milestone worth celebrating as we enter the festive season.