Time in the markets

Izak Odendaal, Old Mutual Wealth Investment Strategist

F. Scott Fitzgerald wrote that the test of “first-rate” intelligence is being able to hold “two opposing ideas in the mind at the same time and still retain the ability to function". There are two opposing ideas investors are grappling with now. Since the start of the second Trump presidency, the world seems more uncertain than at any moment in the last 35 years. At the same time, the bulls are stampeding in global equity markets.

A pessimistic reading of this dichotomy is that this has nothing to do with intelligence and everything with complacency. We are simply experiencing the calm before the storm, in other words. The more optimistic view is that markets have considered President Trump’s wild policy changes and concluded that things will ultimately be OK. The global economy faces headwinds and will slow, but it will not fall over the edge. The record gold price also argues against mass complacency, since many investors are clearly in search of a safe haven.

Let’s examine this glass-half-full perspective. US import tariffs are at levels last seen when Fitzgerald was still alive, but business leaders have strong incentives to adapt to the environment, even if it constantly shits. The effective tariff burden is also not quite as high as the headline numbers suggest due to a variety of carve-outs, concessions and circumventing measures. So far, American businesses have absorbed tariff costs in their margins, with only limited passthrough to consumers in the form of higher inflation. For some firms, this is very problematic, but we haven’t seen overall profit levels under significant pressure. Healthy profit levels are key to the broader economic outlook in the US and elsewhere. The recession-inducing behaviours of companies of laying off workers, cancelling orders and shelving expansion plans usually occur when profits are falling and companies slash costs to maintain margins.

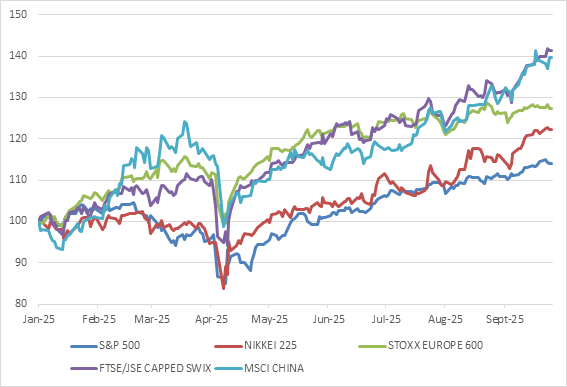

Chart 1: Global equities in 2025 in dollars

Source: LSEG Datastream

Importantly, recent years have not witnessed a major build-up of household and company debt and therefore an increase in economic fragility. This means the private sector in the US and other major economies was relatively well placed to deal with Trump’s policy shocks.

The weak link is the US labour market, however, with jobs growth having slowed down notably. This worries the Federal Reserve, and it has resumed an interest rate-cutting cycle, joining other central banks.

Easy financial conditions

Falling interest rates contribute to easy global financial conditions. Similarly, a weaker dollar is a big boost to countries outside the US. Fiscal policy is also loose. That will create problems at some future point, but for now expanding government debt levels in the US, China and Europe boosts markets and economic activity. In simple terms, it is hard to imagine a recession when both fiscal and monetary policy is so stimulative. As the old saying goes, economic expansions rarely die of old age but are usually bludgeoned to death by policy shocks. Trade policy has not yet delivered a big enough shock while fiscal and monetary policy are keeping the party going.

The hundreds of billions of dollars being spent on artificial intelligence (AI) is also a notable offset to the tariff headwinds. A back-of-the-envelope calculation is that tariffs amount to a tax increase on US businesses of around $300 billion a year, but AI-related capex spending by the mega tech companies is running almost double that. Whether the spending will be sustained is another matter. One day, these companies might realise that they’ve overbuilt datacentres and the like and that generating a decent return on all this capex won’t be possible. However, there is no sign of us being there yet.

So, while complacency is always a danger and there are plenty of risks, the above does not suggest doom and gloom. It is a complicated environment with many cross currents, but then if we look back throughout history, there were always things people worried about. Think about Fitzgerald’s most famous novel, The Great Gatsby, which turned 100 this year. It was set in the freewheeling decadence of the Roaring Twenties, but also darkly foreshadows the 1929 crash and Great Depression. This period, which he called the Jazz Age, was noted for the mass adoption of cars, radios and other consumer electronics and consumerism in general. In 1920, there were only nine million vehicles on the road in the US. By 1929, the number had tripled. It was also an age of industrial advancement. Electrification of factories and businesses became widespread (Eskom was established in 1923).

At one point, it was fashionable to say that the 2020s would be a rerun of the Roaring 1920s, despite the inauspicious start to the decade due to Covid. In fact, the pandemic probably shook the global economy out of the post-financial crisis stupor and low-interest rate environment of the 2010s. Other commentators are worried that decade will end the same way the Jazz Age did, with an economic calamity and ultimately, a war between the global superpowers.

The reality is that we don’t know. If the first half of the 2020s has taught us anything, it is to expect the unexpected. But it also showed that, under the right conditions, and with the appropriate positioning, the unexpected need not derail your portfolio. So, what to do? The advice in 2025 is not so different to what it would have been in 1925: diversify, invest for the long term, keep an eye on valuations and stick to the plan

Eggs and baskets

Diversification is about risk and return. For South African investors, for instance, diversifying offshore is a hedge against domestic political and economic uncertainties and currency that depreciates over time. But it is also being able to tap into a much larger opportunity set. There are thousands of listed companies internationally, compared to a hundred or so shares of a decent size locally. In important sectors like AI, biotech, robotics and defence, there are virtually no options on the JSE.

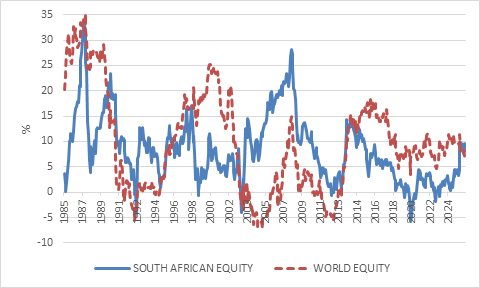

But it also runs the other way. The past few years have seen many investors join a headlong rush abroad, driven not so much by diversification as chasing the most recent winner. International equities outperformed the local market over most of the past 15 years due to a weak rand, low commodity prices, sluggish domestic growth and the US tech boom. However, as chart 2 below shows, returns are cyclical, and it appears that the cycle has turned. Ultimately, the best argument for diversification is simply that the future is always and has always been uncertain and unpredictable. It’s not just about not putting all your eggs in one basket, but also that we never quite know which basket will be the best one.

Chart 2: Rolling five-year real annualised returns in rand

Source: LSEG Datastream

The other point chart 2 illustrates is the ability for equities to deliver inflation-beating returns. South African equities beat inflation 95% of the 483 five-year periods shown. Over the whole period since 1980, the average annual real return was almost 8%. There were ups and downs, but a long-term investor was handsomely rewarded. And this wasn’t a period without drama. The 1980s saw the Rubicon Speech, the debt standstill, sanctions, unrest and the messy transition to democracy. The Asian Financial Crisis hit in 1998, and the Global Financial Crisis a decade later.

Price is what you pay, value is what you get

It is always difficult to know whether the years ahead will be fat or lean, but a good starting point is to look at standard valuation measures like price: earnings ratios or dividend yields. These never tell the whole story and can’t predict what happens in the short term (the next 18 months or so). However, it can give investors a good indication of the returns they can expect over the longer term (five to 10 years). History suggests that expensive investments deliver disappointing long-term returns, or to put it slightly differently, investors might have to wait a long time for an expensive investment to deliver a decent return, even if it is a very good asset.

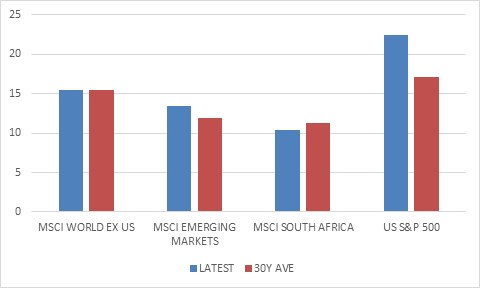

Chart 3: Global equity forward price: earnings ratios

Source: LSEG Datastream

Chart 3 shows that US valuations are well above the 30-year average (a period that includes the dotcom bubble), suggesting below-average long-term returns ahead for US equities. The US has many economic advantages over other countries, but this is seemingly more than priced in. Markets outside the US are in line with their historic average, pointing to reasonable future returns. South African equities trade at somewhat below average valuations, despite a very good year on the local market. Strong earnings growth, partly due to elevated precious metals prices means share prices have not run ahead of underlying profits.

Interestingly, Gatsby was a commercial disappointment in Fitzgerald’s lifetime. Only after his death did it become very popular, particularly when the Army distributed it as a paperback to soldiers during World War II. Meanwhile, the best-selling book in 1925, Soundings by Hamilton Gibbs, has largely been forgotten. Intrinsic value isn’t always recognised in real time and something similar happens in investment markets where an asset class can be ignored or unloved for a long time, while other asset classes can keep rising well above their fundamental values.

Too much information

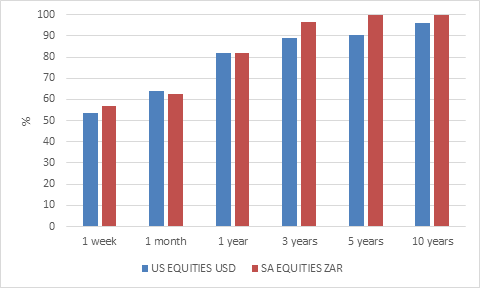

Nick Carraway, the narrator in Gatsby, was a bond trader. In his day, and indeed well into the 1980s, access to data gave investors an advantage. No longer. For both professional and retail investors information is no longer scarce, attention is. Today you can track your portfolio in real time on your phone. This has arguably not made us better investors, since the more we see the ups and downs of the market, the greater the urge to do something. For instance, as chart 4 shows, investors who look at the stock market daily or week will think it is extremely risky since it is basically a coin toss whether it will be positive. However, look at the market once a year, and the probability of a positive return increases to 80%. For longer periods, the probability rises further.

Chart 4: Probability of a positive return based on holding periods

Source: LSEG Datastream. Based on data since 1975.

It comes back to that old adage that it’s time in the markets and not timing the markets. With the dramatic global changes of the past few years – Covid, Ukraine, Gaza, AI, Trump 2.0 (and at home, the 2021 riots, the 2024 election) – the temptation to switch investments or get out of the market until the uncertainty fades have been tremendous. Those investors who’ve waited for the proverbial dust to settle are probably still waiting. They have missed out on a period of strong returns.

So yes, the world is very uncertain. But it is also true that markets can do well even in messy environments. Ultimately, as investors we cannot control what happens in the world out there, we can only control how we react. A disciplined, balanced, patient and valuation-sensitive response has stood the test of time.