Current oil crisis is a symptom of much larger supply and demand imbalance across energy sector

Mark Lacey, Head of Thematic Equities and Portfolio Manager, Global Resource Equities and Alex Monk, Global Energy Resource Equities Portfolio Manager at Schroders

Investing in energy equities in today’s geopolitically charged world

Energy has once again become a key driver of both global and domestic outcomes. For South Africa, energy is not an abstract global theme. It quickly feeds into our inflation, our household budgets, business confidence, and ultimately our economic growth.

Heightened geopolitical tensions in the Middle East, especially around the Strait of Hormuz, have underscored the fragility of global energy supply chains. In a country that is highly sensitive to imported energy costs, global energy dynamics matter far beyond the energy sector itself and are a critical macro variable that affects all asset classes, particularly in emerging markets like our own.

Ceasefires and peace talks a distraction from a deep structural issue

Even in the event of a successful agreement between the US and Iran, which leads to a full opening and transit through the Strait of Hormuz, Mark Lacey, Head of Thematic Equities and Portfolio Manager, Global Resource Equities at Schroders said in a recent Schroders webinar, that there is a 400 million barrel shortfall of oil supply, assuming the Strait returns to normal running by the end of this month. “And there is every risk that the standoff will be longer,” says Lacey.

“Even when the tankers start moving again, oil fields and oil refineries are still shut. Currently, around 2.2mb/day, ~2%, of global refinery output is damaged and offline. Currently, around 3 to 4mb/day of production capacity is shut in, with both Kuwait and Iraq stating that it will take 3 to 4 months to resume production once the region is stable,” he says.

The global gas market has an even greater structural problem according to Lacey who says that around 17% of Qatar’s Liquid natural Gas (LNG) output is damaged – which will take 3 to 4 years to bring back online.

But, Lacey cautions, the real risk goes deeper than just the outcome of current geopolitical tensions – there is a structural supply/demand imbalance across all sectors of the energy market.

“Firstly, the oil market was going into a deficit anyway in 2027, even under normal circumstances. By 2027, US shale production will go into decline. In previous crises where we've needed an urgent supply response, shale oil production has come to the rescue, as it can come to market in three to six months.

“Any oil now that needs to match this supply deficit in 2027 will need long lead development, which is 3 to 4 years. So, there is no instant supply fix,” says Lacey.

Energy demand on the rise

According to Alex Monk, Global Energy Resource Equities Portfolio Manager at Schroders, it isn’t just that there was a supply-demand mismatch on the oil side. “There is a broadening supply-demand mismatch across the energy landscape as a whole,” says Monk.

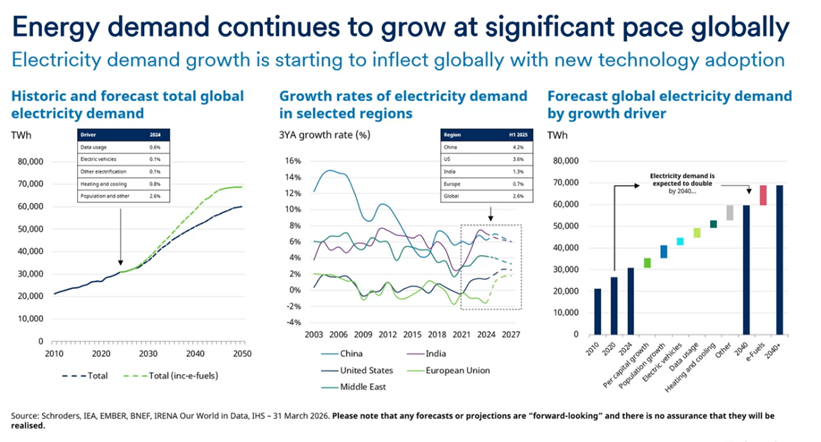

Lacey explains that energy demand is not only about oil – which he says is essentially a transportation fuel. “The biggest energy constraints are in the form of power. Global electricity markets have grown by 10,000 terawatt hours in the last 15 years. And in the next 15 years, they're forecast to grow by 30,000 terawatt hours, three times the growth rate,” says Lacey.

According to Monk, there are several factors driving growth in energy demand. “Data centres are a huge driver, but it is also population growth, growth in heating and cooling needs, and other forms of growth drivers as well,” says Monk.

Interestingly, government attempts globally to soften the impacts of the current energy crisis and energy inflation on consumers have actually had the reverse effect. “Releasing strategic reserves, removing fuel taxes, subsidising energy, and putting price caps on what can be charged at the pump have actually supported demand, not destroyed it through long-term switching. The only areas we have seen rationing or demand destruction policies have been on speed limits, public transport promotion, specific rationing of LPG in Asia, and some reduced lighting of cities – but this is not enough to solve the level of demand destruction that would be required to balance the lost oil and oil products’ supply over the remainder of the year,” says Lacey.

Outside of these actions that support consumer demand, the biggest collective action has been the International Energy Association’s coordinated release of 400 million barrels of emergency oil stocks, agreed on 11 March 2026. The US then launched the first tranche via a strategic petroleum reserve (SPR) exchange of up to 86 million barrels, part of a 172 million barrel US share. These inventories are expected to be replenished over the next 2 years.

Meeting the demand means we’re entering a long-term energy investment cycle

According to Lacey, we are entering a long-term energy investment cycle for several reasons. “Firstly, reserves are very low. The reserve life of listed oil and gas companies has contracted 25% since 2013 (proved FAS69 reserves). We estimate that companies need around $80/bl to $85/bl in order to incentivise an increase in capital expenditure (in order to make a sufficient return-on-capital-employed and in order to maintain the steady growth in shareholder distributions). We believe around $65/bl oil - not $80/bl- is being discounted in energy equities today,” says Lacey.

Secondly, Lacey says that extremely low investment rates are the reason why global oil and gas spare capacity is limited. “Despite global oil demand increasing over 25% since 2006, overall upstream investment has been at similar levels for the last three years. The oil and gas industry’s capital expenditure has been very low since the collapse in 2015 and in order to stimulate an increase in investment going forward, we would expect oil prices to stay above $80/bl over the next few years.

Lastly, US shale oil production has peaked and other non-OPEC supply additions are limited from 2027 onwards. “Assuming oil demand continues to grow at a steady 1mb/day going forward, non-OPEC supply is not sufficient to meet this demand growth going forward. We would expect oil prices to stay above $80/bl over the next few years to stimulate investment and have a meaningful impact on supply from 2029 onwards. Current oil demand estimates remain around 107mb/day in 2027, and under this scenario the oil market was heading towards a small deficit. Despite a ceasefire, the resulting restocking and production outages mean that the market will now likely be in a bigger deficit in 2027,” says Lacey.

What the investment cycle means for investors

According to Lacey, the investment cycle is very important for energy equities. “Energy equities typically outperform broader markets during a net investment cycle, and they underperform during a net divestment cycle. The conflict in the Middle East does nothing but support this cycle going forward.”

And even before the war started, Lacey says that energy equities were steadily outperforming broader markets, not only because of the long investment cycle in oil and gas, but also because most investors are underweight energy equities.

Monk says this presents a very interesting buying opportunity for investors.

“The world is short of energy. When you look at the energy system as a whole, and different parts of the world will be slightly different in terms of what the mix is, you need all these technologies to ultimately solve the global imbalance between supply and demand. In certain parts of the world, renewables will work better, while in other parts of the world, gas or potentially even oil will work better, and there will be certain applications, like data centres, where gas and nuclear become more effective. This means that all the parts of the energy complex should see earnings growth as we try to solve the demand-supply imbalance.”

Coupled with this, Monk says valuations across both the conventional and alternative energy sectors are attractive.

According to Lacey, this is where active management becomes valuable. “We're constantly moving around the different parts of the value chain to look where that earnings growth is strongest and also where the valuations and shareholder returns are most attractive to create an optimal risk-reward picture for delivering returns to clients.”