Diamonds in the rough: Finding gems in an uncertain earnings environment

A Q3 earnings review from BlackRock Fundamental Equities, November 2023

Helen Jewell – Chief Investment Officer, BlackRock Fundamental Equities, EMEA&Stefan Gries - Head of European Equity, BlackRock Fundamental Equities focusing on the key takeaways from the recent earnings season and exploring how investors can find opportunities in an uncertain earnings environment.

A brighter outlook for industrials?

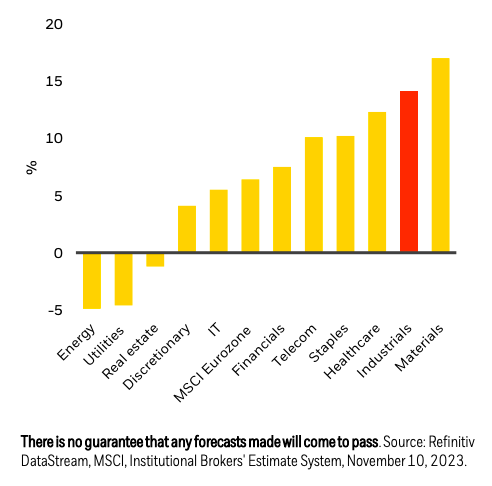

Earnings-per-share growth estimates for 2024

Valuation opportunities

Third quarter corporate earnings in Europe highlighted a sense of uncertainty among investors. Earnings were broadly in line with lower expectations, falling around 14% from one year ago.* But when companies missed analyst estimates – even slightly – their share prices were often heavily punished by the markets.

A notable feature of the Q3 earnings season was that companies whose share prices fell the most on earnings misses were those with the most stable earnings over the past five years, our analysis shows. Some of these companies have suffered earnings disruptions that warrant lower valuations. Yet many are seeing revenue return to more

normal levels after a few years of stellar sales. We believe the market has overcorrected in these cases, reflecting an uncertain macroeconomic environment and growing fears of recession. However, we do not see a deep recession around the corner, and some of these quality companies are now available at attractive valuations, in our view.

Bright spots remain across sectors

Despite disappointment at the overall index level, Q3 earnings also revealed dispersion – and opportunity to unearth companies with above-average earnings growth

prospects across sectors. Within financials, for example, we remain positive on European banks overall, but see large differentiation in earnings between some of the banks in Italy, Ireland and Spain, which are performing strongly, versus banks in other parts of Europe.

And among industrials, around half of companies missed earnings estimates as inventory levels rose and material and labour costs hurt margins. Yet despite this, many industrial companies – or some parts of industrial companies – proved resilient in the third quarter.

Earnings support for select industrials

We wrote in our recent Stock Market Monitor that decarbonization and deglobalization are two powerful, longterm forces that may boost the earnings of some industrials,

and that was evident in Q3 earnings. Some areas that supported sales: investment in power grids necessary for the energy transition, electrical infrastructure for data centers, the reshoring of manufacturing, the need for battery plants and the production of air compressors required for the hydrogen industry and carbon capture.

These services and business areas sometimes form only part of an overall conglomerate. So as stock pickers, we have to know the different strengths of companies within the sectors. But we also have to know the strengths and weaknesses of the businesses within companies. Can the areas with earnings momentum, powered by long-term megaforces mentioned above, continue to outweigh parts of industrial companies that are more closely tied to the economic cycle?

We believe they can. Earnings growth estimates for the industrials sector in Europe in 2024 are second only to materials companies, as the chart shows. Some of these industrials see strong growth potential as U.S. government spending on the energy transition, currently in early stages, is more fully deployed. And valuations are now more attractive amid concerns of an economic pullback that we don’t believe will hit all industrial companies with the same severity.

We believe current European equity valuations are attractive and – because stock markets tend to be forward looking – they could recover swiftly ahead of a major improvement in the economic outlook. So the medium-term for markets is bright, in our view, although selectivity will remain key as the cycle evolves and companies adjust to a new regime of higher rates.

* All earnings data in this report comes from our analysis via Refinitiv and MSCI, as ofNovember 10, 2023.