On track

It is always good to have an example of how not to do something. After five frustrating weeks, the US government shutdown has finally ended. For now, it should be added. The agreement between Republican senators and a handful of Democrat defectors will only fund the Federal government until end January. The economic damage of the shutdown is limited, though it started causing widespread disruption to air travel, meaning things would have been different if it dragged on. Markets breathed a small sigh of relief on the news, though it will take some time before the regular publication of economic data resumes, hopefully providing more clarity on the state of the US economy.

Instead, the greater damage is to the credibility of US fiscal policymaking. No one should believe this is the last shutdown and there are likely to be future standoffs over raising the debt ceiling too. Political divisions now run so deep that future episodes could be even more intense. All this while US federal debt levels keep rising. The one thing both parties seem to implicitly agree on is that there is no urgency in stabilising these debt levels. It should be noted, however, that America has a vast reserve of credibility to squander. US government bonds are still considered the global ‘risk-free’ asset, and the dollar is still the reserve currency. In contrast, South Africa lost credibility on fiscal matters and has been fighting to regain it.

The good news is that there has been tangible progress but at some cost. “Fiscal consolidation”, as it is euphemistically called, is a painful process of constraining government spending and raising tax revenues, with taxpayers essentially paying more and getting less in return. However, it has been necessary since South Africa followed the alternative approach of funding spending with debt for too long. The government now spends a fifth of tax revenues on interest payments, diverting funds away from other important social objectives.

The 2025 Medium Term Budget Policy Statement (MTBPS) is not a turning point in fiscal policy, since it is the culmination of years of effort. But it represents a turning point of sorts in investor perceptions. One can easily get lost in the detail. After all, the MTBPS represents the government’s plan to raise R1.9 trillion in tax revenue in the current fiscal year, and spend R2.3 trillion, including R421 billion on debt service costs. So, let’s just focus on three key areas.

Growth outlook still better

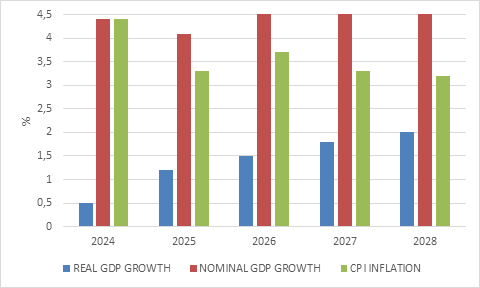

The first is the economic assumptions that underpin this budgeting process. Real (excluding inflation) and nominal (including inflation) economic growth rates were revised lower, given global headwinds and the failure of fixed investment spending to grow as expected. Instead, fixed investment spending will decline this year, before starting recovery next year. Real gross domestic product (GDP) growth of only 1.2% is expected in 2025, though this still represents double the rate achieved in 2024. It is projected to rise to 2% in 2028. These forecasts are broadly in line with the consensus of private sector economists. In other words, while 2025 is disappointing relative to earlier expectations, it already marks an improvement from previous years, and it should continue rising over the medium term.

Sustained higher economic growth rates are crucial to making the budget maths work over the long term. A bigger economy organically generates more tax revenues and increases the government’s capacity to service existing debt. The MTBPS therefore maintains a four-pronged approach to raising economic growth: Macroeconomic stability (including low inflation and debt stabilisation); structural economic reforms, including the work of Operation Vulindlela; increasing state capacity so that the government, particularly local government, can be an accelerant rather than a hinderance to economic activity; and ramping up public spending on infrastructure, and crowding in private investment.

Chart 1: South Africa’s macroeconomic forecasts

Source: National Treasury

Secondly, in terms of revenue and spending trends, it is notable that the current fiscal year will see SARS collecting R19 billion more than budgeted, despite softer-than-expected economic growth. This is also while still taking a conservative view on a potential tax windfall from precious metals miners. Rather, most of the overrun comes from VAT. The May Budget pencilled in an additional R20 billion in tax revenues from an unspecified tax hike next year but also noted that greater SARS efficiency could negate the need to do so. This might still happen, but clearly SARS is on a good wicket in terms of performance, while the gold and platinum boom could still surprise to the upside. Either way, though, there is no relief for taxpayers in the years ahead as the tax-to-GDP ratio is expected to rise from 25.7% this year to 26.4% in 2028/29.

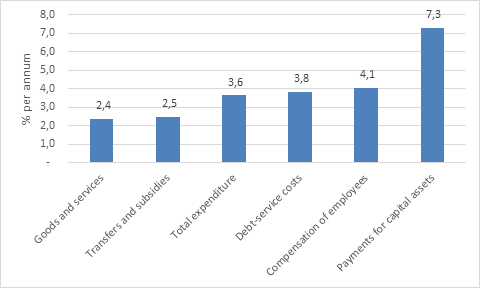

This year’s tax overrun will largely be directed toward increased spending on several one-off matters, but there are also initiatives to improve spending discipline. More than 8 000 suspected ghost workers have been identified, for instance, while work is ongoing to consolidate or close underperforming or low priority programmes, with some R6.7billion in savings identified already. Looking at the projected spending increases over the medium term, there is a notable change. Capex will be the fastest growing item at a projected rate of 7.3% (or 4% in real terms). Interest payments, long the fastest growing line item, have now been pushed down the rankings and are expected to grow by 3.8% over the forecast period. The wage bill is projected to grow by 4.1% on average between 2026 and 2028.

Chart 2: Projected growth in government expenditure components, 2026-2028

Source: National Treasury

Balancing spending and revenue

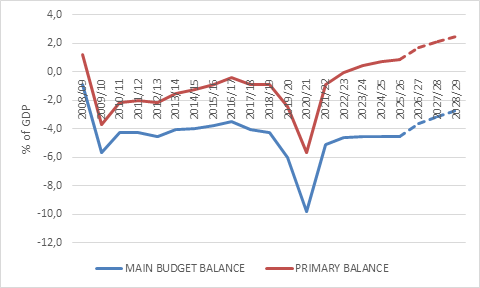

Thirdly, if we put spending and revenue side by side, the difference is the budget balance, which has been in deficit since 2008, meaning that spending consistently exceeded tax income. The gap was filled by borrowing, with the government’s outstanding debt rising to R5.5 trillion or 77% of GDP. This, in turn, drove the surge in annual interest payments noted above, which doubled from 2.5% of GDP a decade ago.

However, if interest payments are excluded, a much better picture emerges. This is the so-called primary balance, which has been in surplus for the past three fiscal years (including the current one) and is projected to increase further over the medium term. This essentially means that revenues now cover non-interest spending, with a bit left over to start paying down debt.

Chart 3: Primary and main budget balance

Source: National Treasury

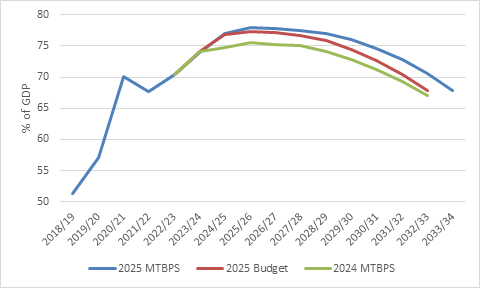

Together with an additional R31 billion top-up from the Reserve Bank’s gold and foreign exchange contingency reserve account (GFECRA), supported by elevated gold prices, debt levels will stabilise as a percent of nominal GDP. The debt-to-GDP ratio is projected to peak at 77.9% in the current fiscal year and gradually decline thereafter. It is not the first time that Treasury has promised to “flatten the curve” in the debt ratio, but previously this goal was always a few years away. Now it is happening as we speak, even though it will do so at a slightly higher level than the May Budget expected. This is significant and means the interest burden will also start stabilising as a share of revenue.

Chart 4: Debt-to-GDP ratio

Source: National Treasury

The decline in the debt ratio would have been faster, but slower growth in nominal GDP means the denominator will be smaller, pushing the ratio slightly higher. This helps explain why the Treasury was less eager than the Reserve Bank to lower the inflation target. What seems to have tilted the argument in the Reserve Bank’s favour was the sharp decline in government bond yields following its announcement of a shift to targeting the lower end of the 3% to 6% range. This decline in government borrowing costs partially offsets the impact of lower inflation on tax revenue assumptions.

Benefits

The benefits of achieving sustained inflation around 3% will be substantial. Households will experience a slower rise in the cost of living, while businesses will similarly not lose competitiveness against other countries as quickly. After just 10 years, a country with 4.5% annual inflation will have a price level 20% higher than one with 3% inflation. After 20 years, the gap is 60%. The theory of purchasing power parity (PPP) suggests that the exchange rate between these two countries will adjust to bring competitiveness back in line. This largely explains why the rand weakens so much over time against the currencies of relatively low-inflation economies such as the US dollar or euro. Wrestling inflation down to 3% on a sustained basis – something that won’t happen overnight – therefore points to a more stable rand over time.

It also implies lower interest rates. If we assume that the repo rate should be 2.5% above inflation through the cycle, we are talking about it declining from 7% currently to around 5.5% eventually. This will be a multi-year process, but the Reserve Bank is now likely to bring the next cut forward, perhaps even this week. Because the government now officially backs a 3% inflation target, the Reserve Bank will have more confidence that the target can be achieved over the medium term. A large part of how inflation targeting works is that people must believe that inflation will be 3% (or whatever the number is). With Treasury throwing its weight behind this target, it becomes easier to communicate to the population that they should anchor on 3%, as opposed to the slightly confusing message that the Reserve Bank aims for the lower end of the 3% to 6% range. The simpler the message, the more powerful it is. It can also reverberate more quickly through the broader public service, who, as we know, has been the biggest culprit in giving above-inflation salary increases and implementing above-inflation increases in administered prices.

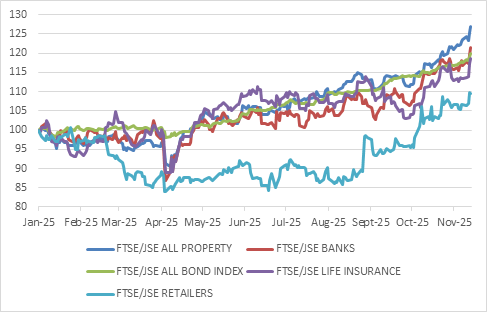

Chart 5: SA interest rate sensitives

Source: LSEG Datastream

It is no surprise then, that we’ve seen a strong rally in interest rate-sensitive assets this year including immediately after the MTBPS. This is the market giving the thumbs up for a lower inflation target and progress in fiscal consolidation. At least one of the major ratings agencies is also taking notice. On Friday evening, S&P Global upgraded the government’s local currency credit rating one notch to BB+ and the foreign currency rating to BB. This is still in sub-investment or “junk” territory, but S&P maintains a “positive” outlook, suggesting another upgrade is possible in the next 12 months if the economic growth accelerates and fiscal metrics improve further.

The introductory chapter of this year’s MTBPS is titled “On track: meeting fiscal targets and advancing reform”. It is a pithy summary of the document’s intent, but also — for once — a reasonably accurate reflection of what is actually achieved. The market is recognising it as such and ratings agencies will come round eventually. There is still a long road ahead and staying the course will depend on political will and stability. Nonetheless, the narrative that everything in South Africa is going backwards and that investors should take all their money offshore is losing credibility by the day. South African bond, equity and listed property benchmarks have outperformed their flagship global counterparts in dollar terms over the past five years. The better approach, humbler and more sensible, is to be appropriately diversified.