People, pensions and policy choices

Izak odendaal, Old Mutual Wealth Investment Strategist

Last week’s 90th anniversary of US President Franklin Roosevelt signing the Social Security Act into law went by largely unnoticed. However, it was a landmark reform, providing a minimum level of state support for people in old age for the first time, part of a package of interventions to combat extreme poverty in the Great Depression. This was not the first state-backed pension system in the world but would grow to be the biggest and most well-known. Some 52 million retirees receive a monthly cheque from Social Security, and for two thirds of them, it forms at least half their retirement income. For 16 million Americans, it is their only source of income in old age.

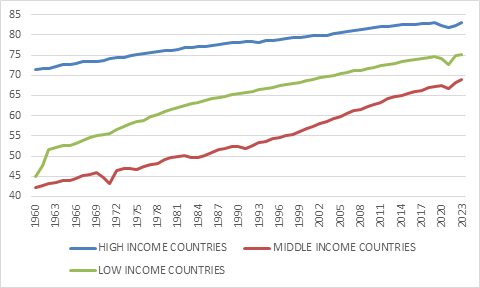

A lot has changed over the past 90 years, especially in the quality and extent of human lives. If we stay with the US for a minute, in 1930 about 85 babies out of every 1 000 born would not live to see their first birthday. Today it is only 5.6 out 1 000.This dramatic reduction in early child deaths contributed to a sharp increase in average life average expectancy, rising for women from around 62 years in 1930 to 77 today. The more recent gains in life expectancy are largely due to lower mortality rates among the middle and old-age cohorts thanks to better treatment and healthier lifestyles. Even in poor countries, lifespans have increased dramatically in recent decades though they still lag richer nations.

Chart 1: Female life expectancy at birth

Source: World Bank

The other notable demographic trend is that the average woman is having fewer babies all over the world. In 1930, the US fertility rate (births per woman) was around 3. Today it is 1.6. The global fertility rate fell from 5 to 2.2 over the same period. The fact that women can choose to have fewer children today is widely celebrated, but it also means that in most rich countries the average woman is not having enough children to replace herself and her partner. The fertility rate in Japan is 1.02 and in Spain it is 1.2. The lowest fertility rate in the world is in South Korea. At only 0.7, it means that the average woman is not even replacing herself. Attempts to raise birth rates in low fertility countries have largely failed. Only large-scale immigration can turn this around, but as we’ve seen across the world, immigration is a political hot potato, even in countries with a long history of being open to migrants, such as the US.

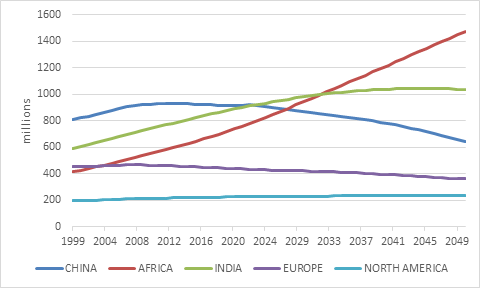

The combination of rising life expectancy and falling birth rates results in rapidly ageing populations, mainly in rich countries but also in some emerging economies, where China stands out due to the implementation of the one-child policy between 1979 and 2015. It is remarkable that the great fear of the 1970s - and not just in China - was overpopulation and the Malthusian dread of running out of resources. Today, it veers to the other extreme, with more commentators warning of an economic calamity due to declining populations. As in the 1970s, this fear might also be somewhat overblown. The UN projects that the overall global population will keep rising until around 2080, largely thanks to India and Africa, though populations in many individual countries will fall over the next few years. Interestingly, the International Monetary Fund recently noted another silver lining: in a study of 41 developed and developing countries, it found that 70-year-olds today have the same average cognitive abilities as 53-year-olds in 2000. If this remarkable finding is true, it means people can remain productive workers late in life, thereby partially offsetting the impact of shrinking workforces. Technologies such as robotics and artificial intelligence will also stand in for some workers though probably not all.

Chart 2: Working age population projections

Source: United Nations

Slower growth

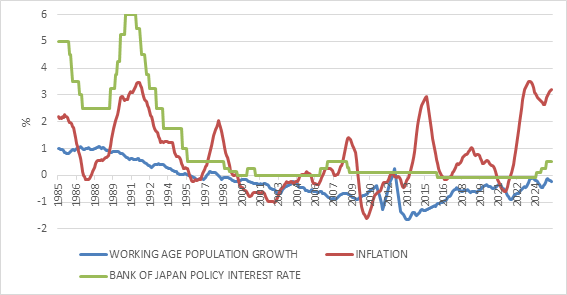

It is therefore still likely that shifting demographics will result in slower global economic growth in the decades ahead as shrinking workforces drag on output and consumption. There are two schools of thought on how this will impact interest rates and inflation. The mainstream view is that slower economic growth will pull interest rates and inflation lower. Japan is in many ways the leading indicator in terms of ageing among rich countries with a median age of 48. Last year fewer babies were born than at any time since record-keeping began in 1899. Its interest rates and inflation hovered around zero for much of the past three decades.

Chart 3: Japan’s demographic decline

Source: LSEG Datastream

The other view, associated with economists Charles Goodhart and Manoj Pradhan, is that a shortage of workers will push up wages and inflation and interest rates will rise as retirees run down their savings, leading to an imbalance of savings versus investment. Time will tell.

What few disagree on is the challenge this poses for state-backed social security systems and fiscal health in general. Official retirement ages are not keeping pace with increases in life expectancy, meaning that people are spending more years in retirement, drawing a pension. But there are also fewer young people who are working and making pension contributions directly or via taxation. This is a problem for “pay as you go” systems where today’s workers are funding today’s pensioners. As the number of pensioners rise relative to the number of workers (the dependency ratio), these systems will be squeezed and require additional government support. America’s Social Security is one example, and many European countries also operate on pay-as-you-go (PAYG) pension programmes.

Healthcare requirements also rise steadily in old age, adding to the burden on the state. Governments will eventually face tough trade-offs between paying out pension benefits as promised and maintaining appropriate levels of spending elsewhere. The get-out-of-jail-free card of simply borrowing more will increasingly not be an option, especially if interest rates trend higher.

Therefore, many countries are reforming their pension systems by raising retirement ages, adjusting benefits, changing tax treatments and shifting more of the burden and risks of retirement provision to individuals. The fear of collapsing pensions can therefore also be taken too far, though none of these reforms are easy. Australia’s superannuation system, introduced in 1992, is often held up as a success story. Workers and their employers make mandatory contributions into pension funds called “supers” and the state is largely off the hook. Most supers are defined contribution funds, following the international trend, away from defined benefit funds, both public and private. In the former, the member basically gets what they put in plus growth, meaning that they carry the risk of living too long, retiring too early and experiencing poor market returns (but they also get the upside). In the latter, members get a guaranteed retirement income based on years of service or final salary and these risks fall largely on the employer or the state.

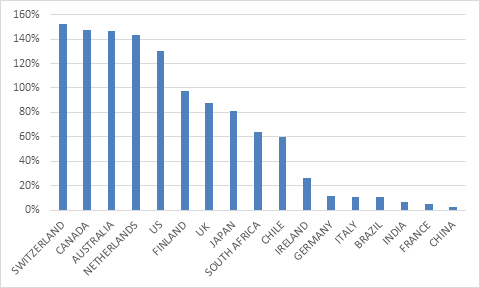

Today Australia is one of only a handful of countries with more than $2 trillion in pension fund assets, according to the Thinking Ahead Institute, the others being Japan, the UK, Canada and, by far and away the biggest at $32 trillion, the US. This puts Australia well ahead of larger economies like France and Germany where PAYG systems dominate.

Chart 4: Pension fund assets as % of GDP

Source: Thinking Ahead Institute

Sustainable pension funds are not merely a grudge purchase for societies. They are also an important source of capital, but the impact depends on where they choose to invest. In both Australia and the US, defined contribution funds predominate, and the average equity allocation is around 50%. US pension funds are also big investors in the venture capital funds that keep Silicon Valley’s conveyor belt of innovation turning. In countries where most assets are in defined benefit schemes, the average asset allocation skews towards bonds, since these can more closely match long-term liabilities actuarily. This is the case in the UK for instance, where proposed pension reforms are currently being debated, including how to get funds to increase investments in UK-listed equity and venture capital to support economic dynamism and productivity growth.

A related argument surfaces from time to time in South Africa too, namely that “prescribed assets” rules should be introduced to force retirement savings into infrastructure and other productive assets. This call is often misinterpreted as the intention of the government to confiscate pension savings to fund itself. Regardless, it is unnecessary. The challenge is not a shortage of funding but rather a lack of bankable projects. The government recognises this and work is underway to increase the pipeline of investable projects and prescribed asset regulations are not on the cards. However, the prudential asset class guidelines Regulation 28 of the Pension Fund Act already channel investment into the domestic economy, since they limit international exposure to 45%. Total equity exposure is capped at 75%, though this adequately leaves room for local pension funds to have significant equity exposure.

It is up to you

Most local funds have also made the transition to defined contribution funds and as such the burden of adequate retirement provision falls largely on individuals. An exception is the Government Employee Pension Fund (GEPF), the largest in the country, which is a defined benefit fund. In other words, if it ever runs out of money, taxpayers will have to bail it out. Fortunately, despite a few governance wobbles at the state-owned asset manager, the PIC, the GEPF is more than fully funded with R2.3 trillion in assets. It is the largest investor in the local bond and equity markets.

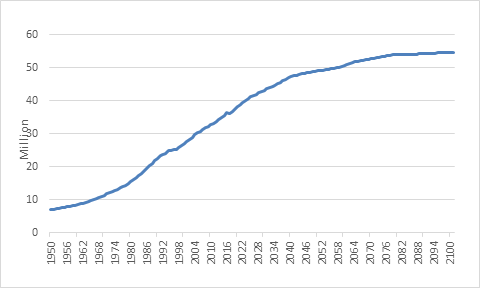

Given widespread poverty and unemployment, many South Africans are not members of occupational pension funds nor do they have private retirement savings arrangements. About three million people currently rely on the state old age pension of R2,200 per month. This is paid directly out of the fiscus. As the population ages, taxpayers will likely have to support more pensioners. Fortunately, South Africa still has a favourable demographic profile with a working age population that is projected to keep rising until around 2075, before levelling off. The challenge to create enough jobs is massive but South Africa is not at risk of running out of workers any time soon.

Chart 5: South Africa’s working age population projection

Source: United Nations

To put it slightly differently, South Africans should worry about whether they are individually saving enough for retirement, rather than whether the country’s overall pension system is sustainable or poses a fiscal risk. The country has a large, sophisticated and well-regulated financial system that is a key strength, though its reach is unevenly distributed. Most people don’t have enough retirement savings since they never earn enough, but many who do earn decent salaries don’t put enough aside.

A big problem in the past was a lack of preserving retirement savings when people switched jobs. The two-pot system addresses this, as two-thirds of retirement savings must now be preserved, with one-third available to be withdrawn for emergency use (and it cannot be stressed enough that it should only be for emergencies). While most of the focus has been on the withdrawals, the compulsory preservation aspect of two-pot is a significant reform that should ultimately improve retirement outcomes for individuals while also increasing the pool of capital available for investing in the local economy. The next step, though unlikely in the short term, is mandatory participation, where every full-time worker must contribute to a retirement fund.

Even so, it is unlikely that membership of an occupational pension fund will be enough to provide sufficient income in retirement for most people, and therefore other savings vehicles will remain important. If you are reading this, you probably knew that already, but if you are unsure, speak to a financial adviser. The best time to start saving is yesterday, and the right amount to save is “more than you think”.