A year of Trump 2.0

Izak Odendaal, Old Mutual Wealth Investment Strategist

A year ago, Donald Trump secured a second term as US president. Due to the oddities of America’s political system, he was only sworn in almost three months later on 21 January, but investors immediately began considering what lay ahead. Indeed, since the victory was not unexpected, a second Trump term was already being discussed and discounted earlier on in 2024. It was widely expected that Trump 2.0 policies would centre on tariffs, tax cuts and immigration crackdowns. That’s what we got, but there have still been several shocks and surprises. Where do we stand after a year, and what insights can we gain for the three years left of his final term?

Tariffs and tacos

On tariffs, the announcements started soon after Trump took office, initially targeting Canada and Mexico, the largest trading partners of the US. “Liberation Day” on 2 April and subsequent announcements were surprisingly harsh, causing an unusual sell-off across US equities, bonds and the dollar. Normally, the latter two rally at times of risk aversion.

Faced with this market backlash, Trump put most tariffs on pause and started negotiating high-level trade agreements. Perhaps this was the plan after all, but it certainly supported the idea that “Trump always chickens out” (TACO), i.e. that when push comes to shove, he will back down and seek a deal that he can sell as a victory. His recent agreement with Chinese leader Xi Jinping came after China imposed export controls on critical rare earth minerals without which many US industries will grind to a halt.

Moreover, the Supreme Court heard arguments last week about the legality of some of the tariffs imposed under the International Emergency Economic Powers Act. While a decision is not expected soon, the justices expressed scepticism over the White House’s case during the hearing. It appears likely that the court will impose some limitations on the White House’s ability to impose import duties.

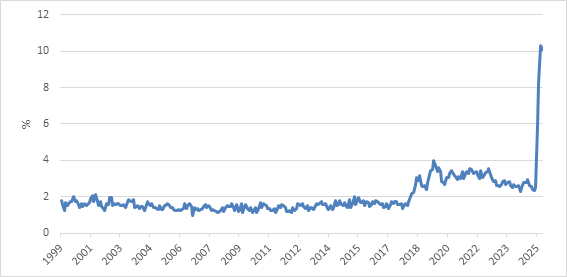

The net result, as we look ahead to the remaining three years of Trump’s term, is that the effective tariff rate, currently at 10%, will probably settle at levels that are more manageable, but still higher than at the start of the year.

Trump won a year ago mainly because he campaigned on achieving a stronger economy and lower prices. On the former, the track record is mixed, but when it comes to prices, the picture is straightforward. Tariffs raise the cost of living, even if we haven’t seen the full extent yet. Last week saw a few notable elections going the Democrats’ way, but the real test will be a year from now, when every seat in the House of Representatives and a third of the Senate are up for re-election. Ahead of next-year’s midterm vote, probably the best thing Trump can do for the Republicans would be to ease up on the tariffs, with or without the Supreme Court’s intervention. The state of the economy and cost of living will remain key for voters.

Chart 1: US effective tariff rate, %

Source: LSEG Datastream

Taxes

This is especially true since Trump’s main legislative victory, the passage of the One Big Beautiful Bill Act (OBBBA), extended tax cuts for companies and wealthy individuals, while cutting some benefits for lower income households. It is a regressive budget in an already unequal society, where the affluent have benefited from higher asset prices.

Despite higher revenues from tariffs, the net result of the OBBBA will be to add trillions to US government debt over the next decade. In the short term, OBBBA adds some positive impetus to the US economy, especially if its allowance for accelerated depreciation of investment spending boosts capex. Longer-term, the increase in government debt is a concern.

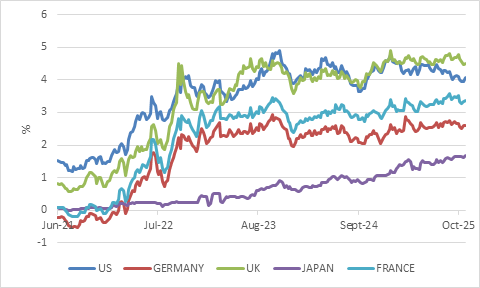

This is not purely a US story, however. One of Trump’s biggest achievements has been in convincing (or forcing) European countries to take more responsibility for their own defence. Germany, most notably, has abandoned the “black zero” commitment to a balanced budget and will increase borrowing to upgrade its military and infrastructure capabilities.

Bond yields across Europe are higher over the past year, despite central bank interest rate cuts, but interestingly not in the US. The 10-year Treasury yield initially rose after last year’s election to 4.8%, reflecting the view of stronger growth, more fiscal spending and potentially higher inflation. Since then, yields have drifted lower, apart from the “Liberation Day” spike. The Fed has cut short-term interest rates by 125 basis points since mid-2024, but longer-dated US bond yields have basically moved in a broad trading range since late 2022.

Chart 2: 10-year government bond yields

Source: LSEG Datastream

Much to Trump’s chagrin, however, the Fed was on pause for most of this year. His persistent and open calls for lower interest rates have been unprecedented and his influence over Fed decision-making could grow next year when he will be able to appoint a new chairman.

The Fed has moved cautiously this year, worried about inflation risks from tariffs (and other sources), though recently its concerns have shifted towards the employment side of its dual mandate. Hiring growth has slowed, perhaps because of the uncertainty surrounding the outlook for the US economy. Whatever the reason, firms are adding fewer new staff members, but exactly how much fewer is a bit of a mystery. The US government shutdown, now the longest on record, means that statistical agencies are not releasing official data at the moment. An agreement in the Senate over the weekend means the shutdown might end soon, just as it was starting to disrupt air travel across the country.

Despite the lower pace in hiring, the unemployment rate has not increased noticeably. This is because labour supply is sharply lower due to immigration crackdowns. Immigration is a political hot potato across the world, especially when migrants look, speak and pray differently to locals. Foreigners also make for easy scapegoats for crime or unemployment, whether in South Carolina or South Africa. However, countries whose native-born workforce is shrinking need migrants more than others. This is increasingly true of the US, where low-skilled migrant workers are particularly needed on farms and construction sites. At the other end of the skills spectrum, the ability to attract the best and brightest from across the world to American universities and corporate campuses has long been a unique strength of the US economy, but it seems in question now.

Closer to the present, the Fed will continue to look at the state of the labour market to guide its decisions. It recently warned investors not to take future rate cuts for granted. If the US economy holds up, fewer rate cuts will be needed. A repricing of the interest rate outlook has contributed to wobbly markets over the past few days and gave the dollar a boost.

The dollar has been one of the big surprises this year. When Trump was elected, it was a consensus view that his America-first policies would be dollar-positive. Instead, the first half of the year has seen a rush from large global investors to hedge against the risk of a weaker dollar. This hedging activity can create a self-fulfilling prophecy, and the trade weighted dollar is 10% weaker year-to-date. It has recently stabilised, however, and the next big move up or down will largely depend on what the Fed does next.

Luck

Luck plays a role in politics. The first year of Trump 2.0 has coincided with an epic boom in spending on artificial intelligence (AI) infrastructure. The numbers are staggering, estimated to be between $300 and $400 billion this year. A back-of-the-napkin calculation shows that this amount roughly equals tax revenue from the higher US tariffs. In other words, AI spending is putting back into the economy what tariffs are taking out. Of course, the winners and losers are different, but the overall impact is in the same ballpark. This is one of the reasons why Trump’s tariffs have not caused the economic declines one might’ve expected otherwise.

There is no sign of this AI spending slowing down, and indeed the companies involved keep raising their guidance on future capex. However, investors have questioned the valuations of some of the listed companies over the past week, leading to a wobble in stock prices. This kind of correction is healthy after a strong run.

Chart 3: US equities and the dollar

Source: LSEG Datastream

The longer-term questions around AI remain unanswered. How much will consumers be prepared to pay for AI services? Which companies will be big winners? Will all this datacentre capacity be profitable? Which sectors are disrupted the most? Will we see mass layoffs? Will the productivity gains be widespread or concentrated in certain sectors?

Another question is where all the electricity will come from to power these data centres. Trump’s assault on renewable energy puts the brakes on electricity production though the US still has abundant gas reserves. Still, many commentators are warning that it is a steadily growing electricity supply that could ultimately give China the AI edge.

The one thing we can say is that AI excitement has pushed up valuations on US equity markets. These tell us nothing about what happens over the next year (or three) but suggest longer-term return expectations are muted. This specifically applies to the S&P 500 Index of large, mostly multinational firms. S&P’s indices of smaller and mid-cap firms are trading at muted multiples. These companies tend to be more US-focused, though it should be noted that an American small cap can be considered a giant in many other countries.

The valuation of the S&P 400 and S&P 600 indices shows that investors are not pricing in substantial optimism over the broader US economy. In other words, this does not exactly look like a thumbs up for Trumponomics. In contrast, small and midcaps traded at a premium to large caps in the wake of Trump’s first election victory in 2016, when the market priced in a stronger domestic US economic outlook under a Trump presidency.

Chart 4: Forward price: earnings ratios

Source: LSEG Datastream

In conclusion, it has been an eventful year, even by Trump’s standards. Though there have been positives from this period for the US economy, Trump’s policies have also led to short-term headwinds and long-term uncertainties. The good news is that some of the extreme tariff scenarios that seemed possible earlier this year are now unlikely. The main area of current concern is the state of the labour market, and how the Fed reacts. No one likes uncertainty, but it is not necessarily a bad thing when markets climb a wall of worry - when investors are constantly fretting about what can go wrong.

Ultimately, as we brace for the remainder of Trump’s term, the first year offered a reminder of the difficulty of market timing, and how investors shouldn’t let politics cloud their decision-making. Trump opponents who predicted a crashing market and economy have been wrong so far and probably missed out on returns. Similarly, Trump supporters who thought that everything would be terrific are probably disappointed. It is better to approach things calmly, ensuring proper diversification and keeping an eye on valuations.