All That Glitters

Izak Odendaal, Old Mutual Wealth Investment Strategist

It started with stars and a bang. The elements that form the building blocks of life on earth were created in nuclear explosions inside stars billions of years ago and ultimately scattered throughout the universe. This includes element number 79, gold. As our planet was forming, gold particles formed part of the earth’s core. It is theorised that a period of intense asteroid activity about four billion years ago forced some of this into the mantle. Other theories suggest hot fluids and magma dissolved the gold particles and moved it closer to the surface where it eventually cooled in fissures and cracks in the crust. Tectonic shifts, erosion, weathering and other geological processes over millions of years then exposed these gold deposits to a point where humans could eventually access them.

In the case of South Africa’s gold riches, a meteor strike two billion years ago concentrated these deposits in reefs that formed an arc from Witwatersrand to Klerksdorp and Welkom around the impact site near Vredefort.

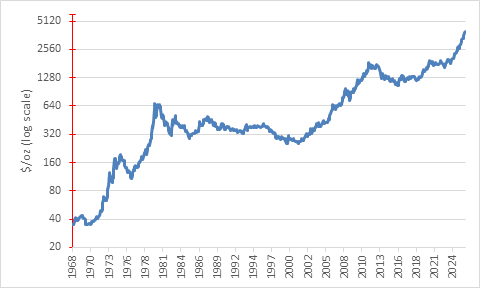

In other words, immense astrophysical forces created gold atoms, while ancient geological forces created the gold reefs and deposits that could eventually be mined. Arguably, humanity’s millennia-old fascination with gold as an object of value reflects some deep psychological force. Today, it is largely political forces that are responsible for gold’s glittering run, pushing the price towards $4000 per ounce for the first time.

Chart 1 Gold bullion price, $/oz

Source: LSEG Datastream

Fiscal follies

While the current upcycle in gold began in 2022, the most recent source of momentum is the two-week old US government shutdown. Democrats and Republicans cannot agree on passing a new budget, meaning that parts of the federal government have no funding for the fiscal year and workers must go on furlough until Congress can appropriate the money. This has happened before from time to time, with the longest shutdown in late 2018 lasting five weeks. Since government workers receive backpay, the economic impact was limited. Therefore, the big worry is not so much the shutdown as what it represents: deepening political divisions that will make tackling the US government’s long-term debt problem difficult.

The US is far from alone. France’s new prime minister resigned after scarcely a month in the role as he too has failed to get parliamentary support for tackling the country’s large budget deficit. It is not that any of these rich countries’ debt levels are unmanageable from a technocratic point of view. It is the political will that is missing and that is what markets are starting to worry about.

It points to an ongoing increase in government debt which means more bonds being issued but also increasingly a shortage of safe assets. US Treasury bonds have long been the world’s risk-free asset and will continue to be so in many contexts, but in other ways it is losing that role. This is firstly because of the political dysfunction described above that led to the US losing its triple-A credit rating, and secondly because many countries no longer see US bonds and the dollar as purely financial, politically neutral, instruments. Reserve managers like central banks and sovereign wealth funds had been gradually diversifying away from dollar assets, but this process sped up after a big chunk of Russia’s central bank reserves were frozen in the wake of the full-scale invasion of Ukraine in 2022. Most countries are (hopefully) not planning to invade their neighbours, but even peaceful nations wonder if there isn’t a small risk of falling foul of the US government.

But where to go? There is a shortage of triple A-rated government bonds to invest in. S&P Global only rates 11 countries as AAA. These include small countries like Switzerland, Singapore, Luxembourg and the Netherlands, whose markets are not liquid enough to absorb a large shift away from US assets. The largest AAA-rated sovereign is Germany, which until recently has been trying to reduce borrowing, i.e. shrinking its bond market. This is starting to turn around under the Merz government, but the reality remains that large investors have limited options if they want the ideal combination of safety, convertibility (which China doesn’t offer) and liquidity.

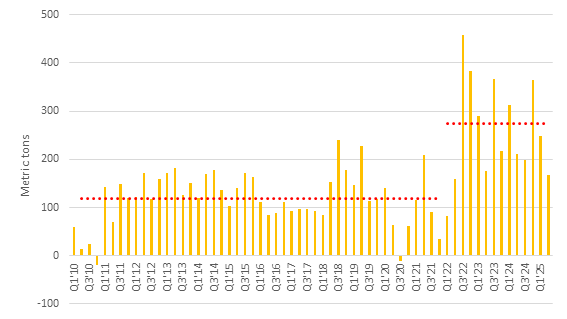

This is where gold comes in. Central bank purchases of gold have doubled since 2022 to an average of around 270 tonnes per quarter compared to 118 tonnes per quarter between 2010 and 2021 according to the World Gold Council. Central bank purchases are a small part of the overall gold market and still only half as big as the demand for gold for jewellery fabrication. However, since the overall gold market is not that big and supply is largely fixed, this increase in demand had a notable impact on the price. The daily turnover of between $100 billion and $200 billion in the global gold market is but a slice of the $900 billion daily turnover in the US Treasury market. This also means that gold can never be a perfect substitute for US bonds, since it too lacks liquidity.

Chart 2: Central bank purchases of gold

Source: World Gold Council

But as more investors and reserve managers allocate to gold on the margin, it has boosted the price. This has attracted speculators. Where there is price momentum, FOMO (fear of missing out) is sure to follow.

While it is often said that gold is an inflation hedge, it is clearly not the driver this time. US inflation has ticked up, but longer-term market-based indicators of inflation expectations remain stable. At any rate, there have been plenty of periods where gold underperformed inflation, notably the 20% peak to through decline in 2022 while the world was grappling with an inflation surge. Even worse was the slump in gold prices that started in 1980 when the US Federal Reserve hiked interest rates aggressively. It would take another 30 years for gold to deliver a real return in dollars.

Another traditional explanation for gold price movements, the inverse relationship with real interest rates, is also not applicable today. Since gold pays no interest, the opportunity cost of holding it falls with interest rates. If rates rise, it becomes relatively expensive to hold bullion. Though real interest rates have declined somewhat this year, the decline is nowhere near enough to justify a 50% jump in the gold price, especially since real rates are still elevated compared to the past 15 years.

Therefore, it is hard to escape the conclusion that the gold price has been driven by a search for alternatives to US dollar assets in a world where safe havens are in short supply. And, of course, with plenty of momentum buyers.

September 2025 Edition

Getting gold

Is it too late to get on the bandwagon? That is an impossible question to answer, but there are a few considerations.

One is to clarify what purpose it will serve in your portfolio. If the idea is to diversify away from other asset classes, then a small allocation will always make sense. If diversification is the goal, the direction of price movements matters less than the correlation with other asset classes. If, however, the aim is to maximise gains, investors should be wary since the price has already run up so much already. The forces described above could continue pushing it higher, but who knows? As Isaac Newton quipped after losing money in the South Sea bubble, “I can calculate the movement of stars, but not the madness of men.” Newton would be able to explain the celestial origins of gold atoms but where the “madness” of political machinations takes us next would be lost on even him.

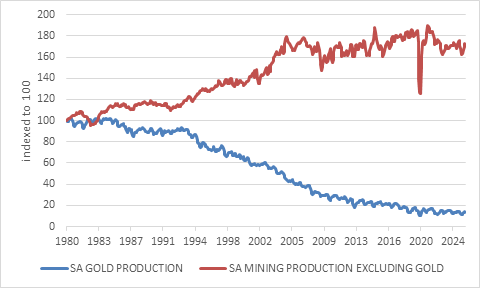

The second consideration is that South African investors already have indirect exposure to the gold price. The country is no longer the world’s top gold producer, since most of the gold has been mined out after 150 years and what remains is kilometres deep and costly to extract. Sadly, the mining climate in general has become very difficult due to regulatory red tape, sky-high electricity prices, poor transport infrastructure and increasingly, illegal mining. Even when excluding gold, mining output has flatlined over the past 20 years. And since exploration activity has declined, output will not increase any time soon.

Chart 3: South African mining output

Source: Stats SA

Nonetheless, while the South African economy, financial market and exchange rate are less influenced by the gold price and mining in general than in the 1980s, the impact is still important. The JSE has boomed this year, with the All Share Index topping 100,000 points for the first time on the way to a 34% year-to-date return. This is helped along by an echo-boom in platinum group metals prices. Platinum is not a replacement for gold but can be a substitute in some contexts, and the price is up 74% this year.

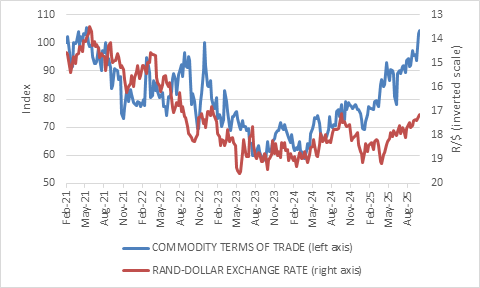

Suddenly, gold and PGM miners are very profitable. They don’t necessarily need metals prices to keep rising to remain profitable. If prices remain relatively stable at elevated levels, shareholders will be smiling. The taxman will also smile, and so indirectly the gold boom is good for bonds by reducing the South African government’s borrowing requirement somewhat. Bonds and other interest rate-sensitive assets benefit from a stronger currency. As shown in chart 4, the rand has appreciated as the country’s terms-of-trade - export prices relative to import prices – and improved with higher precious metals prices and cheaper oil (note the rand is on an inverted scale).

Chart 4: Commodity prices and the rand

Source: LSEG Datastream

In summary, the gold price is a windfall for investors with broad South African market exposure, even if they don’t specifically own Krugerrands or a gold ETF. It is worth reiterating that the geopolitical conditions that gave rise to the rally in gold look set to remain in place, but that doesn’t mean that the blistering pace of price gains will be sustained or can’t be reversed. As with any market, investors should approach this coolly and rationally and try to look through the hype. It started with a bang, but how it will finish is anyone's guess.