Bonds behaving badly

Izak Odendaal, Old Mutual Wealth Investment Strategist

As the three-month mark of the Gulf War approaches, a barrel of oil is still close to triple digits and the pressure on the global economy continues to build. Business profit margins are squeezed, and household real incomes are slipping. Reported inflation is already higher due to the direct weight of fuel prices in consumer price indices. Companies will pass on some of their cost increases to consumers, making a broadening of inflation pressures likely in the months ahead. However, that will largely depend on how long energy prices remain high.

Equity markets have largely ignored these concerns, focusing instead on strong earnings growth and enthusiasm around the artificial intelligence (AI) capex boom and anticipated blockbuster listings of SpaceX, Anthropic and OpenAI.

Downbeat bonds

Bond markets, in contrast, have been much more worried. In one sense, this is to be expected. Bond investors are always a bit nervous. Their preoccupation tends to be to preserve money, whether in nominal or real (after-inflation) terms. Equity investors have more of a blue-sky view of the world, focusing on potential upside. Stereotypically, they fear missing out more than almost anything else. And the AI rally seems to be FOMO on steroids.

The prices of government bonds have slumped since the start of the war, pushing up yields. The proximate cause is the inflationary impact of higher oil prices. In many developed countries, inflation had only just returned to target after the 2021/22 surge. In the case of the US, inflation was still in the process of hitting the Federal Reserve’s 2% target. The last time the Fed’s preferred inflation measure was close to target was March 2021, and it is once again moving in the wrong direction.

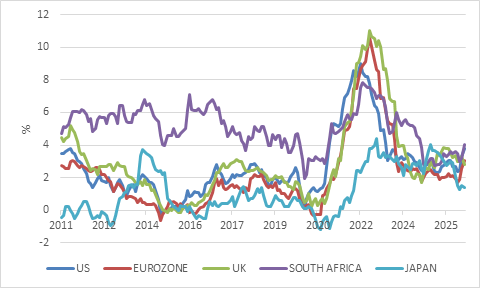

Chart 1: Headline consumer inflation rates in selected countries

Source: LSEG Datastream

Bond valuations are particularly allergic to unexpected inflation, since it erodes the fixed income bonds provide. The unexpected bit is key, because markets adjust quickly to what is expected and the war upended the narrative of gentle global disinflation in force at the start of the year. There is a category of bonds whose values are protected against inflation, but these inflation-linked bonds are a small slice of the overall pie. Most bonds issued by governments leave investors at the mercy of shifts in the inflation outlook. That wasn’t always a problem, since inflation across the developed world tended to be well behaved over the past few decades. Not anymore, it seems, with the post-Covid global surge in inflation potentially signalling a regime shift.

Inflation’s negative impact on bond valuations is compounded if central banks hike interest rates. Higher short-term interest rates offer competition to longer-term bond yields and money can flow from bond markets into cash.

It is at times like these when central bank credibility is important. If investors sense that central banks are willing to tolerate higher inflation than in the past, they will want higher bond yields to compensate for this risk. It is notable, for instance, that in the emerging markets where central banks have adopted inflation targeting and shown a willingness to tackle inflation, bond markets have been more stable. In the past, a similar risk-off event would have seen an indiscriminate sell-off of bonds and currencies of emerging markets, including South Africa (more on that below).

Nonetheless, central banks have different sensitivities to the oil price. Expectations for European Central Bank rate hikes jumped as soon as the bombs started falling. However, until very recently, the US Federal Reserve, the world’s most important central bank, was still expected to cut rates. No longer.

Minutes from its April policy meeting, released with the customary three-week lag, showed officials growing more concerned about inflation. A “majority” indicated they could support “some policy firming” if inflation remains above the 2% target, though “most” participants continued to see downside risks to the labour market. While Fed rate hikes are still unlikely, so are rate cuts. Incoming Chairman Kevin Warsh is widely believed to be dovish (i.e. in favour of lower rates and less concerned with inflation) but he will have a hard time convincing his colleagues that rate cuts are appropriate when inflation is rising, even temporarily, and the latest labour market date points to some stabilisation.

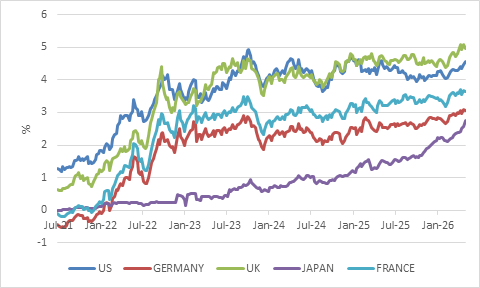

Chart 2: Developed market 10-year government bond yields

Source: LSEG Datastream

Borrowing bonanza

In the background, beyond Hormuz, is the high level of government debt (accumulated past borrowing) and large budget deficits (ongoing current borrowing). Rising government debt can weigh on bond valuations in two broad ways. Firstly, mechanically, more government borrowing means more issuance of bonds. Supply increases relative to demand. All else equal, this should lower prices and push up yields. Markets are always forward-looking, so it is not just about today’s supply and demand picture, but also a view of what it will look like in the future. The second reason is the feedback loop. As governments borrow more, they must pay more in interest every year. This squeezes out other areas of spending, inviting political pushback. As the interest burden rises, so does the political risk - however small - that bondholders won’t be paid back in full. Or that politicians will just take the easy route of borrowing more to ensure that spending on salaries and so on is unaffected. This perceived deterioration in creditworthiness can also reduce prices and raise yields. This is where the vicious cycle starts: any new borrowing or rolling over of maturing bonds is done at these higher yields, further raising the interest burden and lowering creditworthiness.

Too soon

Nonetheless, it is too soon to talk about a worldwide sovereign debt crisis. Governments have many ways to kick the proverbial can down the road, starting with forcing banks and pension funds to buy more of their bonds. Central banks can also be pressed into action to buy government debt, but as noted above, it will erode their credibility. The interplay between central bank independence and future debt sustainability will likely become increasingly complicated in the years ahead.

Another reason not to panic is that in many countries, nominal economic growth rates are still above government borrowing costs, as illustrated in table 1. This is only a rule of thumb, but it does indicate that the largest economies can still “grow out of debt” if they wanted to. However, the likes of France and the UK cannot be complacent, while South Africa still has a long road ahead, though it is at least trying to stabilise its debt level and its efforts are being recognised. Moody’s changed the outlook on the South African government’s debt from “neutral” to “positive” on Friday evening. This is the first step towards a potential ratings upgrade from Ba2 to Ba1.

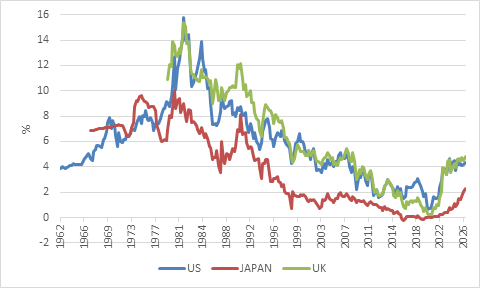

Chart 3 places current bond yields in a longer historical perspective, showing that they are by no means extreme. After falling to historically low levels around 2020 – with European and Japanese yields turning negative – the big reset happened in 2021 and 2022. The more recent moves have been small and orderly by comparison, which should provide some comfort.

Chart 3: 10-year government bond yield history

Source: LSEG Datastream

Close call

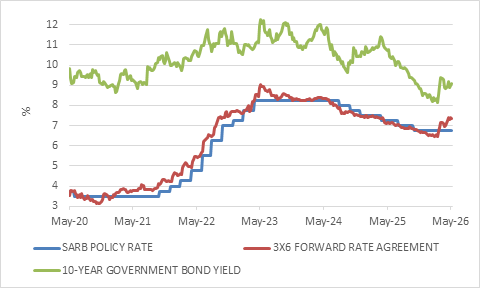

South African interest rate expectations have also shifted. Government bond yields are higher, though the move has been relatively small compared with past episodes as noted above. Yields also remain well below the peaks reached in 2023, as Treasury’s fiscal consolidation efforts continue and supply-side reforms are implemented. However, the Reserve Bank’s credibility as an inflation fighter is also crucial, and much of the decline over the past year can be attributed to the shift to the 3% inflation target.

Chart 4: South African interest rates, %

Source: LSEG Datastream

This week’s Monetary Policy Committee meeting will be a close call. Reported inflation rose to 4.0% in April, largely as expected, due to the jump in fuel prices, and will rise further in the months ahead, pushing away from the target. With more fuel inflation set to rise in the coming months, overall CPI inflation will probably peak at around 5%, up from 3% at the start of the year. Apart from fuel prices, global fertilizer shortages and an expected strong El Nino suggest there is upside risk to food prices over the next 12 months. One can also make a good argument for staying on hold, however. The policy rate was already elevated at the start of the year, and the rand has been relatively stable throughout. Either way, the market is already pricing in at least two 25-basis points increases in the South African Reserve Bank’s policy rate over the next six months as chart 4 shows.

Rate hikes will contribute to somewhat weaker economic growth than projected before the war. The silver lining is that increases are likely to be modest. The aim will be more about communicating the SARB’s commitment to its 3% target than cooling an overheated economy or trying to catch up with sharply rising inflation as in 2021 and 2022. This also implies that the rate cycle should turn quickly, with the first cuts coming next year. More importantly, getting inflation down and keeping it down will have significant long-term benefits for the South African economy and its financial markets.

Barrel half full

Since the war was the trigger for the bond sell-off and rising interest rates, a material de-escalation that allows the barrels to start moving through the Strait of Hormuz Gulf again will calm things down considerably. Central banks will be able to take a more sanguine view on whether inflation will be transitory. Bond yields can decline, although the long-term fiscal picture across developed markets will not be getting better, perhaps not until there is a big enough crisis to force a change in direction. Therefore, the news on the weekend that the US and Iran appear to be moving closer to a peace deal is encouraging, though nothing has been finalised yet and uncertainty remains high. As usual, markets will price in a more positive scenario long before an agreement is concluded. This means trying to time the market is largely a futile exercise, and a diversified investment approach therefore remains as important as ever.