Far from it - are we approaching the end of the global rate-cutting cycle?

US Federal Reserve Chair, Jerome Powell throws cold water on rate cut expectations as slowing US job growth clashes with stronger economic growth.

By Sebastian Mullins, Head of Multi-Asset and Fixed Income, Schroders Australia

Despite all the drama of the US/China trade talks, perhaps the most interesting development recently was US Federal Reserve (Fed) Chair, Jerome Powell’s press conference after the Federal Open Market Committee (FOMC) delivered another 25 basis point rate cut. Powell hinted at ‘strongly differing views’ and that the December rate cut is ‘not a foregone conclusion, far from it.’

This quickly shifted market pricing for a December cut from 100% priced to 65%. The market is still pricing a terminal rate of around 3% for the US, which implies another 100 basis points of cuts to come, which we believe to be excessive. The apparent debate within the Federal Reserve (Fed) is healthy, as it shows the tension between weaker job growth, but the potential for strong economic growth and sticky inflation.

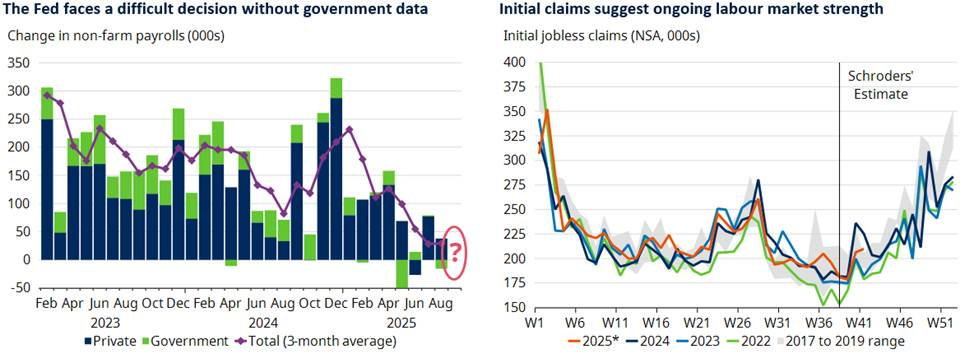

The required replacement rate of new jobs in the US economy has shifted to a structurally lower level. Previously, monthly new farm payrolls above 100k were required to keep the unemployment rate unchanged. However, Lorie Logan, President of the Federal Reserve Bank of Dallas, estimates that breakeven payroll growth has probably fallen to 30k per month, reflecting lower immigration and a declining participation rate as the population ages.

While the government remains shut down, it is hard for the Fed or for market participants to understand if jobs growth is recovering. However, any print above 50k will likely see the unemployment rate fall. Another way to look at employment is to track initial jobless claims against their seasonal averages. Based on this, jobless claims are well within recent historical averages and show no sign of a deteriorating jobs market. That leads us to believe that the job market is not as weak as some members of the Fed believe and therefore the Fed may be cutting into a recovering economy.

Chart 1: Is the labour market truly weakening?

Source: Macrobond, Schroders Economics Group, 20 October 2025.

Global economy and earnings remain strong

We continue to be more optimistic than consensus about the global economy, and expect growth across both developed and developing economies to be higher in 2026 than this year.

We also expect marginally higher inflation as wages growth reflects tighter labour markets. If so, it is likely that central banks are close to the end of their easing cycle and interest rates are at their cycle lows. With the US government shutdown, hard data on the US economy is scarce, but consumers are still spending and the AI capex boom continues, creating a floor for economic growth.

With the US economy growing at 3.8% last quarter, supported by strong consumption of 2.9%, we do not see signs the economy is at risk of a recession. We believe consumption and capital expenditure will keep a growth floor of 2% for the US. This puts us far away from a recession call, with our recession dashboard only 25% triggered. US inflation data for September was marginally lower than expectations, mostly due to the housing components and rent in particular, which remains the main weak spot in the economy.

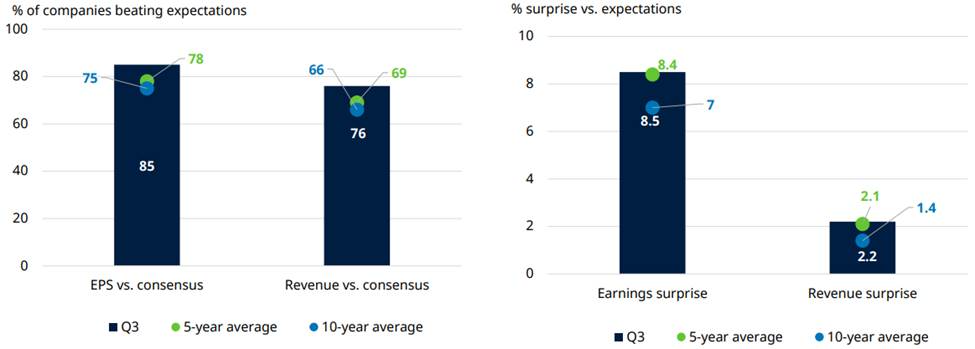

With over 65% of US companies reporting, earnings per share and revenues remain strong. 85% of companies have beaten revenue expectations, compared to the 10-year average of 75%. Earnings per share and revenue beat by 8.5% and 2.2%, against a 10-year average of 7% and 1.4%, respectively. Earnings revisions are also ticking up for non-tech companies, with the S&P 500 ex-technology and Magnificent Seven seeing revisions jump from just above -2% before October to 3.5%. With rate cuts delivered, Trump’s big beautiful bill being passed and our belief for a stronger economy, nominal earnings should continue to do well over the coming year.

Chart 2: The percent of S&P 500 companies surprising on EPS and revenue above historical norms

Source: LSEG, Factset, Schroders Economics Group. 31 October 2025.