Global Market Outlook: All eyes on US jobs and rate cut expectations

Sebastian Mullins, Head of Multi-Asset and Fixed Income at Schroders Australia

August started with a shock non-farm payrolls report, which saw monthly jobs come in over 30k less than expected, but even more concerning was the negative revision of 258k total over the prior two months, bringing revised job growth to sub 20k in both May and June. This saw markets quickly price in a slowing economy and brought expectations forward for a rate cut in this month and two rate cuts by the end of the year.

With inflation coming in line with expectations for August, tariff concerns took a backseat. Powell’s Jackson Hole speech leaned more dovish, including comments that monetary policy can only impact cyclical changes to the economy, not structural changes such as trade policy, coupled with a strong emphasis on defending employment over fighting inflation. The market further interpreted a more dovish future Federal Open Market committee (FOMC) board after Kugler’s resignation allowed Trump to appoint the Chairman of the Council of Economic Advisers, Stephen Miran, to replace her.

More recently, Trump’s attempt to fire Cook from the board has further cemented the market’s interpretation that the Federal Reserve (Fed) will lean dovish into 2026. While the erosion of central bank independence will have negative consequences for long-dated US treasuries, the market so far appears relatively sanguine, despite modest yield curve steepening.

However, almost all of the economic data released throughout August provided little evidence that the economy is slowing or that rate cuts are needed. Gross domestic product came in strong at 3.3%, with personal consumption recovering to 1.6%. Retail spending was robust over the period and producer prices rose 3.3% over the year, the highest increase since 2022, led by services as opposed to tariff-related goods. Composite Purchasing Manager Indices (PMIs) continue to improve, financial conditions continue to ease and earnings revisions are turning more positive. So far, this has yet to curtail expectations of rate cuts, with the market hoping for a goldilocks scenario where the Fed cuts rates due to subdued inflation and political pressure, even though the economy appears to be on stronger footing than originally anticipated.

While the non-farm payroll revisions are concerning, the initial positive results were a surprise when they were released given the backdrop. It makes sense that corporates would pull back from hiring during May and June given the unprecedented shock of April’s Liberation Day tariffs. It is too early to see if this is a trend, based on continued business uncertainty or margin compression from tariffs, or a short-term reaction, which could see jobs rebound throughout the year as uncertainty fades. While job growth is slowing, labour supply is also falling due to Trump’s immigration policy, keeping unemployment low.

Inflation slow to appear in the data

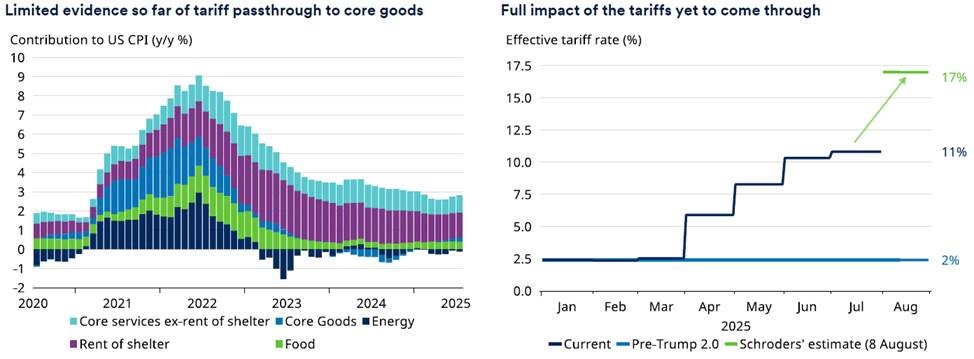

Concerns remain over how tariffs will impact inflation in the US, and how that will impact corporate margins, employment, real wage growth and ultimately consumption. But it is too early to see the full brunt impact of tariffs on the official consumer price index (CPI). The current US effective tariff rate is heading towards 17% based on current deals, but the actual realised tariff is only around 11% as of this month, meaning it has further room to increase. At the same time, analysis from Goldman Sachs indicates that 64% of the tariffs have so far been absorbed by corporates. It will take time for corporates to pass these costs onto consumers, meaning the impact of tariffs on inflation will likely take longer than anticipated to show up in the data.

Chart 1: Still too soon to see any impact of tariffs on inflation

Source: Schroders Economic Group, Macrobond, 15 August 2025.

Given this backdrop, we believe it is too early to turn bearish. For now, our recession model remains switched off, with more indicators likely turning off if the Fed follows through with rate cuts. We previously stated that the US will either be heading towards stagflation, where inflation stays elevated but growth slows, or reflation, where both growth and inflation re-accelerate. Today it looks more like the latter, but we need to keep a watch on employment and corporate margins to see if and when tariffs start to bite.