Living annuity drawdown rate average drops below 6% for the first time since 2011

Jaco van Tonder, deputy chair of the ASISA Marketing and Distribution Board Committee

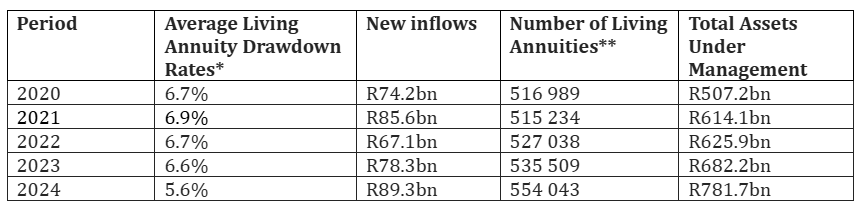

Living annuity policyholders withdrew, on average, 5.6% of their invested capital as income in 2024, the lowest average drawdown rate recorded since the Association for Savings and Investment South Africa (ASISA) started collating living annuity statistics.

In terms of the ASISA Standard on Living Annuities, which came into effect in 2010, member companies are encouraged to provide a living annuity status report to ASISA at the end of each year. Statistics were collected for the first time in 2012 for the 2011 reporting period. The ASISA living annuity statistics for 2024 show a one percentage point drop in the average drawdown rate from 6.6% in 2023 to 5.6% in 2024. A living annuity is a compulsory purchase annuity that does not guarantee a regular income. Instead, living annuity policyholders must select an income drawdown of between 2.5% and 17.5% of the value of their living annuity assets. This can be reviewed once a year on the policy's anniversary date.

Jaco van Tonder, deputy chair of the ASISA Marketing and Distribution Board Committee, says the strong investment performance recorded in 2024 resulted in a healthy growth of the living annuity asset pool. While this contributed to a drop in the average income drawdown levels, calculated by taking the total value of drawdowns against the total value of the living annuity book, the growth in assets also encouraged policyholders to adjust their income drawdown to lower levels.

The living annuity asset pool grew to R781.7 billion by the end of December 2024, compared to R682.2 billion at the end of 2023; an increase of 14.6%. The number of living annuities increased from 535 509 at the end of 2023 to 554 043 as of 31 December 2024.

Van Tonder says it would be prudent for living annuity investors to resist increasing their drawdown rates on the next policy anniversary date, thereby locking in some of the investment gains from last year and this year. The FTSE/JSE All Share Index (ALSI) delivered a return of 13.4% over the 12 months to 31 December 2024. Over the 12 months to the end of June 2025, the ALSI delivered a return of 25.2%.

Van Tonder explains that to prevent the erosion of invested capital over time, the percentage of income drawn should not exceed the real returns of the investment portfolio supporting the living annuity. Three key factors determine whether a living annuity will be able to produce a regular income for the life of an annuitant:

- The level of income selected;

- Performance of selected investments; and

- The lifespan of the annuitant.

According to Van Tonder, annual drawdown rates of 4% to 5% in the first decade of retirement and below 8% in the later retirement years are generally considered prudent, providing annuitants with a high probability of preserving their purchasing power for their lifetime.He says it is encouraging that 36.4% of assets (R284.4 billion) held in living annuities at the end of 2024 fell into the 2.5% to 5% income band, followed by 23.0% (R179.9 billion) in the 5% to 7.5% income band.

A 5-year overview of South Africa’s living annuity book

* The average income drawdown level is weighted by fund size (the total value of the drawdowns against the total value of the living annuity book).

** The number of living annuities does not imply the same number of policyholders. It is not uncommon for policyholders to have more than one living annuity.