Maximising new tax benefits to boost long-term investment outcomes

Shaun Duddy, head of Product Development at Allan Gray

You may have seen the good news in the 2026 Budget that you can now contribute more each year to tax-free investments (TFIs) and retirement funds. But the real benefit isn’t only the higher limits; it is how investing earlier, along with tax relief over time, can meaningfully improve long-term outcomes, according to Shaun Duddy, head of Product Development at Allan Gray.

“Contributions made earlier allow capital to benefit from tax-efficient compounding for longer,” he explains.

National Treasury announced that investors can contribute up to R46 000 per year to a TFI, up from R36 000 previously, while the lifetime contribution limit remains R500 000. Investors can also enjoy an additional tax break on retirement fund contributions, with the annual cap increasing from R350 000 to R430 000.

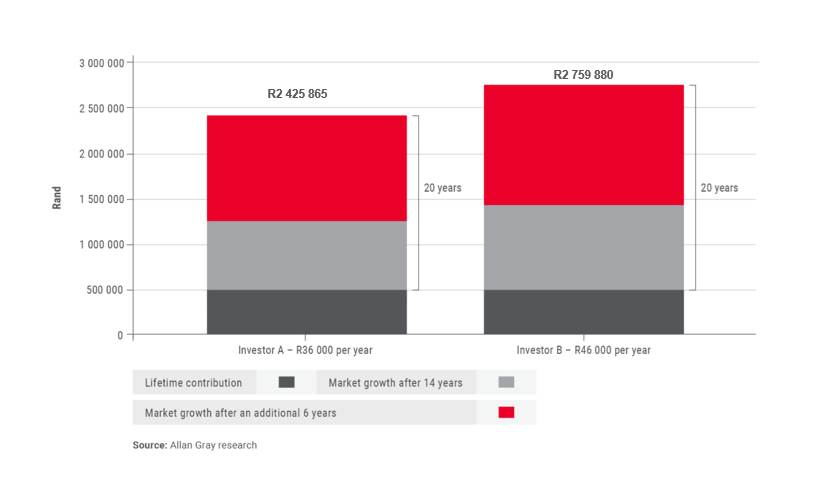

Getting the most out of a TFI

Duddy says the increase in the annual contribution limit for TFIs from R36 000 to R46 000 is the first adjustment since 2021.

“As the lifetime limit has not been adjusted, the increased annual TFI contribution limit means that you are able to invest more every year and reach your lifetime limit around three years earlier, giving your contributions more time to compound over the long term.”

Consider two investors who invest up to the R500 000 lifetime limit and earn the same annual return of 11.6%. Investor A invests R36 000 per year and reaches the limit after just under 14 years, while Investor B invests R46 000 and reaches the limit after just under 11 years.

Although both invest the same total amount, Investor B ends up with more because they invest more money earlier. After 14 years, their portfolio is about 13.8% larger. Over 20 years, the absolute gap grows even more, simply because of the benefits of earlier compounding,” says Duddy. “The difference arises not from how much is invested, but from when it is invested.”

Graph 1: The benefit of investing tax-free earlier

Taking advantage of tax relief with retirement fund contributions

Contributions to pension, provident and retirement annuity (RA) funds are tax-deductible. “This makes them a compelling proposition for long-term investors, and the new contribution caps are especially appealing for high-income earners,” says Duddy.

For individuals earning above R1.27m per year, who maximise their contributions, or for those who previously contributed above the threshold, the increase in the annual monetary cap on tax-deductible retirement fund contributions from R350 000 to R430 000 is particularly relevant.

However, Duddy notes that, as with TFIs, timing is an important consideration. For example, consider an investor contributing R430 000 per year to a retirement fund. Under the old limit, only R350 000 of this amount would be tax-deductible in the same tax year, with the remaining R80 000 treated as an excess contribution. Under the new limit, the full R430 000 is deductible in the same tax year.

“While deferred tax relief is not lost, its real value will likely erode over time due to inflation. Assuming an annual inflation rate of 5%, an excess contribution of R80 000 used only after 10 years would be worth just R49 113 in today’s terms. Accessing tax relief sooner preserves its real value,” he says.

How tax and time impact long-term investors

Duddy explains that tax on investment returns can eat away at the amount available for reinvestment over time, leading to very different outcomes over long investment horizons.

By way of example, according to Allan Gray research, an investment of R10 000 in the Allan Gray Balanced Fund at the end of 2005 would have grown to R89 587 (11.6% annual return) by the end of 2025 before tax. For an investor in the lowest marginal tax bracket (18%), the investment would have grown at approximately 10.7% per year to around R76 490 after applicable taxes. For an investor in the highest marginal tax bracket (45%), the same investment would have grown to only R65 487 over the same period (9.8% annual return) – a reduction of 26.9% overall or 1.7% per year.

“Tax-efficient investment structures, such as TFIs and retirement funds, are designed to reduce or eliminate this drag, allowing a greater proportion of returns to remain invested and compound over time,” he adds.

Duddy says it is best to speak to a financial adviser on how best to take advantage of the tax-efficient structures when investing.

“This is because factors such as liquidity needs, investment horizon, asset allocation and costs remain equally important in determining long-term outcomes,” concludes Duddy.