Monetary policy in the eye of a storm

Izak Odendaal, Old Mutual Wealth Investment Strategist

Being a central banker is not all pinstripe suits, leather chairs and mahogany boardroom tables. Cigars are definitely out of the question these days and whiskey is surely only poured out late at night. The stakes are still high, however, since monetary policy has a big impact on the economy and financial markets. It can change people’s lives in positive and negative ways. Sometimes, the decisions are difficult and the dilemmas acute.

The past two weeks saw several important central banks make interest rate decisions. Before getting to the two that are particularly important for South African investors, it is worth zooming out a bit. After a synchronised post-Covid hiking cycle, most central banks now have an easing bias, though the number of banks cutting rates every month is gradually declining. A weaker global growth outlook due to US tariffs will keep the cutting going, though there are obviously question marks in the US itself, as discussed later on.

The handful of countries still hiking rates each has unique circumstances, such as Russia and Ukraine’s war economies, for instance. Brazil has pushed interest rates higher to offset loose fiscal policy. This is a country with a history of hyperinflation after all and the central bank did not want to take chances, though its policy rate seems to have now peaked at 15%. The most notable of the hikers is Japan, where rates are gradually rising after being pinned near zero for more than two decades. The Bank of Japan left rates unchanged last week, but its forecast of persistent inflation implies that it will raise rates again later this year.

Chart 1: Global central bank interest rate decisions

Source: cbrates.com

The why and how

Most central banks these days aim to maintain a low and stable inflation rate around a specific target rate, 2% in the case of developed countries. Inflation targeting in turn is premised on anchoring the public’s expectations of future inflation, so that their price-setting behaviour matches the target (though there will always be cycles). This then rests on the central bank’s credibility, since people need to believe that it will act if required.

Changes in central bank policy interest rates directly impact commercial banks, either because it impacts central bank lending to banks, or the rate at which banks lend reserves to one another. These are very short-term rates, usually overnight, but they are important enough for interest rates to rise and fall in the broader economy with central bank policy rates, though not always one-for-one. The higher the interest rate, the more firms and households must cough up every month to repay their loans. Higher rates also discourage new borrowing. Both of these effects dampen demand in the economy, though savers will benefit. This also ripples through financial markets, since higher short-term interest rates offer competition to riskier bonds and even riskier equities. There is also the indirect impact, since a weaker economy will weigh on profitability of companies. When the central bank lowers its policy interest rate, the process operates in reverse.

There are market and economic conditions that can blunt the impact of the central bank’s decisions or amplify them. One of these is that borrowers sometimes have the benefit of fixing their loan rates for a period which means they are not affected by central bank decisions. We saw this in the US housing market in recent years, where homeowners could lock in low Covid-era mortgage rates and felt little pain from the post-pandemic surge. European homeowners, on the other hand, mostly have floating rate mortgages and were squeezed when rates went up but benefitted immediately when rates fell. The same is true in South Africa.

Fed pressure

All central banks are also not equal. In a dollar-denominated world, the US Federal Reserve (the Fed) is the most important. The Fed is also somewhat unique in having a dual mandate, given to it by Congress. Alongside price stability, which it expresses as a 2% inflation target, it must also aim for full employment.

It now faces two challenges. Firstly, President Trump’s tariffs threaten to pull the dual objectives in different directions, since there will be upward pressure on prices and downside pressure on employment. The price increase will probably be once off, but that is not guaranteed. Similarly, while unemployment remains very low, 4.2% in July, it might start rising as the tariffs and other headwinds are fully felt. (We’ll discuss the tariffs and their global impact in more detail next week). Faced with this dilemma, the Fed has not cut interest rates this year, including the Federal Open Markets Committee meeting last week. Notably, however, two FOMC members voted for a cut.

Fed Chair Jerome Powell explained that since inflation is further away from the target than unemployment - its preferred inflation measure was 2.8% in June - the focus of monetary policy must be on the inflation side of its dual mandate. Therefore, a somewhat restrictive stance is still warranted. Should unemployment start rising from current levels, the balance would tilt towards an easing bias. The weak hiring data out on Friday after the FOMC meeting suggests this is still likely to happen later in the year.

Since interest rates work with a lag, there are risks to waiting too long and cutting too early. This is an unusually difficult moment.

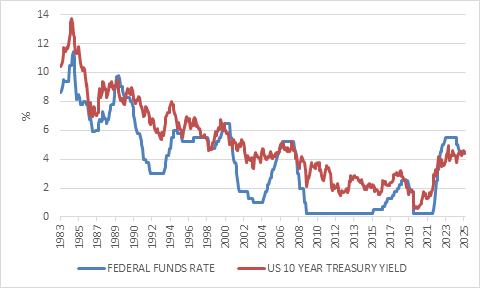

President Trump has different ideas, however, and he has piled pressure on the Fed to lower interest rates. He has not only given Powell unflattering nicknames, but also accused him of mismanaging renovations at the Fed’s headquarters. Powell, meanwhile, is trying to shield the Fed from political interference. Trump seemingly wants lower rates so that the government can save money on its substantial borrowings, but it could be counterproductive if longer-term interest rates rise, which would be the case if markets fear that the Fed will lose its independence and be soft on inflation. As chart 2 shows, longer-term government borrowing costs (the 10-year Treasury yield) are correlated to the short-term Fed policy rate, but they can and do diverge, depending on the market’s outlook for future inflation and interest rates.

Chart 2: US short-term and long-term interest rates %

Source: LSEG Datastream

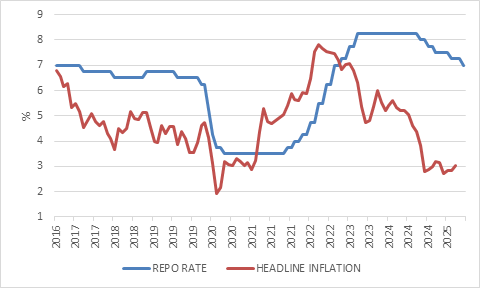

For a central bank like the South African Reserve Bank, the impact of US tariffs is more straightforward, and the Monetary Policy Committee (MPC) lowered the repo rate to 7% at its meeting last week. Tariffs are a demand shock that will lower export earnings without a significant impact on inflation as long as the exchange rate remains relatively stable. Though the rand wobbled after the latest round of tariff announcements, it is within its broad trading range of the past year or so.

Chart 3: SA repo rate and inflation

Source: LSEG Datastream

South Africa has not been able to secure a deal with the US, meaning that its non-commodity exports will be taxed at 30%. Trade negotiations will likely continue, but for now this level US tariffs pose a headwind to key agricultural and automotive export sectors. There are important offsetting tactors, however, and therefore higher US import duties are not a recession-inducing event. This is partly because only 8% of the country’s exports go to the US, but mainly because of the positive impact of lower inflation and interest rates which has lifted consumer spending. Structural reforms to raise investment levels and boost the economy’s productive capacity are also ongoing but will take time to bear fruit. Nonetheless, economic forecasters have cut 2025 projections from around 1.8% to 2% at the start of the year to 1% to 1.5%. Incorporating the tariff impact, the Reserve Bank cut its forecast to 0.9% in 2025, rising to 2% by 2027.

Taking aim

The MPC decision was widely expected. The more notable announcement is that the MPC will now aim for the bottom of the 3% to 6% target. National Treasury must approve a formal lowering of the inflation target and discussions in this regard are still ongoing. Indeed, the Finance Minister did not seem pleased with the “unilateral” announcement. However, strictly speaking the MPC is simply shifting its focus within the existing target range, as it has done before. When inflation targeting was introduced in 2000, the upper-end of the range was generally seen as the de facto goal for many years, before the MPC explicitly started aiming at the midpoint from around 2018.

There are short and long-term implications of moving to a lower inflation target, even if unofficially. In the near term, interest rates are unlikely to fall further as inflation is now in line with the new goal. Headline inflation rose slightly to 3.1% year-on-year in June, but core inflation, which excludes food and fuel prices, fell to 2.8%, the lowest since 2021. Inflation is likely to rise modestly in the next few months, partly as the favourable base effect rolls out.

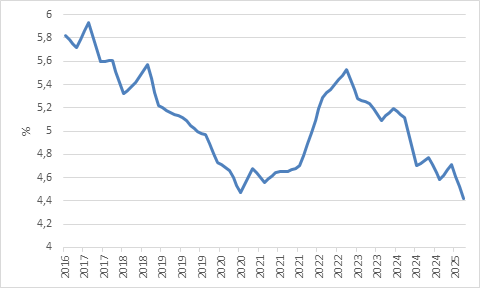

Over the long term, however, interest rates will trend lower if the Reserve Bank manages to anchor inflation and inflation expectations around 3%. Success is not guaranteed, in particular because most of the inflationary pressures are from the supply side, notably municipal and utility costs, and these are not responsive to interest rates or broader economic conditions. It is also important to remember that inflation will always move in cycles, even if the trend is structurally lower. Nonetheless, the progress in anchoring inflation expectations around 4.5% suggests that 3% will be doable over time.

Chart 4: Surveyed expected inflation over five years

Source: Bureau for Economic Research

This will have a positive long-term impact on South African bonds, equities and property, since lower interest rates will make these longer-duration assets more valuable. The depreciating trajectory of the rand against hard currencies will also bend lower, since the weakness of the rand is tied to the gradual loss of competitiveness that the theory of purchasing power parity implies.

At a time when there is considerable global uncertainty, especially around US trade policy, it is a reminder that we should not get too caught up in the short-term noise at the expense of ignoring important long-term trends. We are long-term investors after all. There are several structural reforms underway in South Africa to raise the country’s growth potential and now there is also a push by a credible institution, the Reserve Bank, to lower inflation. These efforts will take time to materialise and there will be ups and downs along the way, but they imply that investors should not be overly pessimistic about the country’s prospects, even if there are headwinds such as US tariffs. With local valuations still attractive, there is certainly room for upside surprises over time. As always though, being appropriately diversified will help when the surprises go the other way.