Paper & Pulp Fundamentals

Daniel Malan, CFA , Founder, Managing Director & Chief Investment Officer, Perspective Investment Management

An aspect of every investment analysis we undertake is to develop an accurate list of comparable global companies. This seems so simple but it is far harder than it appears, especially so in the global paper & pulp sector where companies operate across totally different parts of the underlying industries.

Sappi is predominantly a manufacturer of dissolving wood pulp and coated graphic paper products. Mondi is predominantly a manufacturer of flexible and corrugated packaging paper products, while International Paper is predominantly a manufacturer of corrugated packaging paper products. These five industries each have unique supply and demand dynamics and drivers of volumes, pricing, and profitability.

However, when it comes to long-term investing in the global stock markets it all boils down to an inescapable truth: Regardless of what sectors, industries, continents, or countries it operates in, every listed company is first and foremost a business. We also know from countless case studies that long-term investment outcomes for shareholders matches the long-term underlying business fundamentals of listed companies.

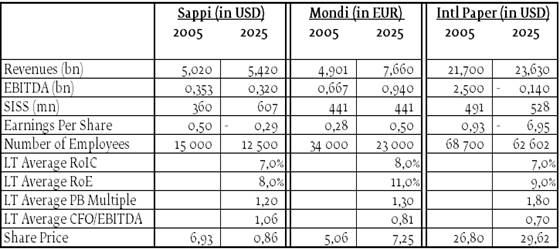

Take a look at some of the long-term business fundamentals of these three listed companies in the global pulp & paper sector.

Table 1: Selected metrics comparing Sappi, Mondi & International Paper

The past 20 years was a period of relative stability and economic growth globally. However, these numbers in the table above suggest the fundamentals and shareholder returns were vastly different between these three companies in the same sector.

A few more insights drawn from the table are:

- Mondi was the only one that grew its revenues, profits, and earnings per share over this period.

- Mondi also delivered the best positive shareholder returns of these three companies over this period.

- Sappi delivered negative shareholder returns over this period, while its issued shares had also increased by a substantial 68%.

- None of these three companies managed to deliver long-term average returns on invested and shareholder equity capital well above their cost of capital. Despite this, the stock market consistently priced them over this period at premiums to book value.

Even a quick glance at the long-term chart of International Paper clearly shows how its share price has essentially travelled sideways since 1987. Bear in mind, this is in nominal terms [unadjusted for inflation].

Chart 1: Share Price of International Paper

Our work continues…