Private equity and credit seen as key for investors to navigate market uncertainty

Private equity ranks among the top avenues for return opportunities in Schroders’ annual investor survey, while private debt and credit alternatives is the number one option for income generation.

Global investors are increasingly turning to private markets to access attractive return and income opportunities, and also potentially enhance portfolio resilience, in the face of persistent macroeconomic and geopolitical volatility.

That’s according to Schroders’ 2025 Global Investor Insights Survey, which canvassed nearly 1,000 institutional investors and wealth managers overseeing approximately $67 trillion in assets. Broadly, the results highlight that investor appetite for actively managed strategies is rising in an environment in which there is no longer a rising tide to lift all boats.

Read the full results of Schroders Global Investor Insights Survey 2025.

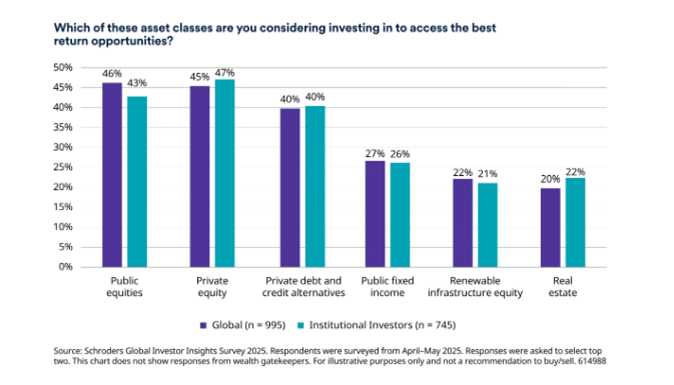

Specifically, private equity (45%) is one of the two most favoured asset classes for all investors seeking return opportunities in the current market, and it is the most favoured asset class for return opportunities among institutional investors (47%), alongside public equities (46% and 43% respectively). At the same time, investors also recognise the potential to source differentiated risk-return opportunities across the spectrum of private debt and credit alternatives (40%), which encompasses a broad range of strategies that provide access to diversified, defensive and opportunistic portfolio income.

Private equity: Accessing resilient return potential

Private equity is regarded as a key avenue to access innovation and sector specialism. For survey respondents who currently invest in private equity, they point to the potential for long-term returns (60%) and diversification (53%) as the primary reasons for private equity’s inclusion in their portfolios.

Schroders Capital research into private equity performance during the major market crises of the past 25 years highlights that the asset class offers protection against public market volatility – and can thrive even amid market uncertainty. Nevertheless, investors need to be discerning in selecting strategies and investments, and diversification is important.

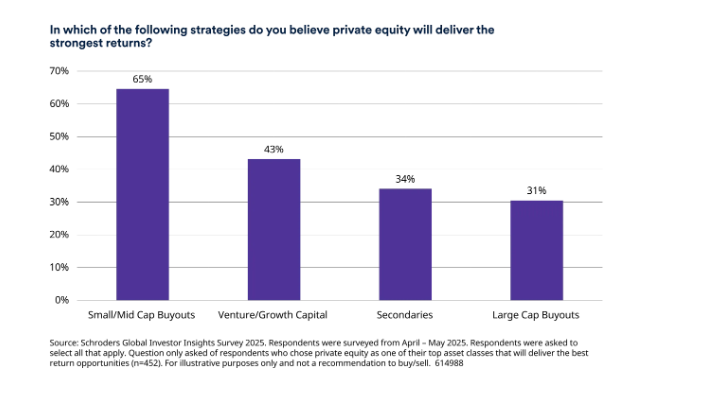

Small and mid-cap buyouts is the clear favourite among those seeking to allocate to private equity, with nearly two-thirds (65%) of investors targeting this segment. Additionally, 43% are targeting venture and growth capital strategies. This reflects a focus on smaller, innovation-rich and domestically focused companies that are inaccessible via public markets and that can be less exposed to global trade disruptions.

Nils Rode, Chief Investment Officer at Schroders Capital, commented: “Small and mid-market buyouts represent a particularly compelling long-term return opportunity in the current environment. These deals benefit from a favourable capital supply and dynamic to offer attractive entry points – and they offer access to a broad and deep universe of often domestically-focused companies that are less exposed to shifting global trade dynamics.”

Secondaries are gaining ground too, with 34% of investors prioritising this segment – outpacing even large-cap buyouts (31%). Last year marked a record year for secondary deals with $160 billion in transactions – and that momentum is expected to continue into 2025, as traditional exit routes remain constrained. In particular, continuation funds, otherwise known as general partner (GP)-led secondaries, are emerging as a mainstream liquidity solution.

Private debt and credit alternatives: Redefining income generation

As traditional fixed income faces new constraints and challenges in an era of high government debt and geopolitical shifts, the universe of strategies across private debt and credit alternatives (PDCA) has moved centre-stage in income strategies.

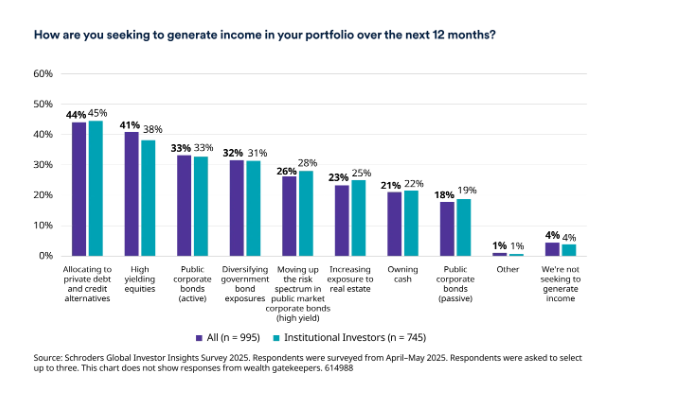

Allocating to PDCA is the top-ranked option for investors seeking to generate income over the next 12 months, chosen by 44% of all respondents and 45% of institutional investors specifically. This is ahead of high-yielding equities (41% of all respondents), active public corporate bonds (33%) and diversifying government bond exposures (32%), and signals a broad-based recognition that private credit is no longer merely an alternative – it can be considered a core building block for resilient portfolio income.

Direct lending remains the most popular strategy within this universe, with 69% of investors and 73% of institutional investors that are targeting investments across private credit identifying this as the top source of attractive, risk-adjusted yield. However, a notable trend is emerging: investors are diversifying beyond this core and potentially saturated exposure to explore new sources of scalable, thematic income.

In this regard infrastructure debt (63%) and securitised products (60%) are now viewed as powerful complements for those allocating to private debt and credit alternatives. Infrastructure debt offers long-duration, stable cashflows, while securitised products provide flexibility and the potential to capitalise on market inefficiencies. Notably, gatekeepers and wealth managers surveyed rank securitised credit (64%) and infrastructure debt (60%) as the top two strategies to generate income yield in private credit, above even direct lending (56%).

Michelle Russell-Dowe, Co-Head of Private Debt and Credit Alternatives at Schroders Capital, commented: “In an environment defined by uncertainty, inefficiency and volatile risk premiums, the ability to select well-collateralised debt, backed by strong borrowers and robust security packages, is a significant advantage of private debt and alternative credit markets.

She continued: “The ability to access diversifying and flexible income through the wide universe of securitised and asset-backed finance, defensive income through real asset debt, and uncorrelated income through insurance-linked securities, provides a valuable extension of the fixed income toolkit for investors.”

Real assets: Tapping into structural growth opportunities

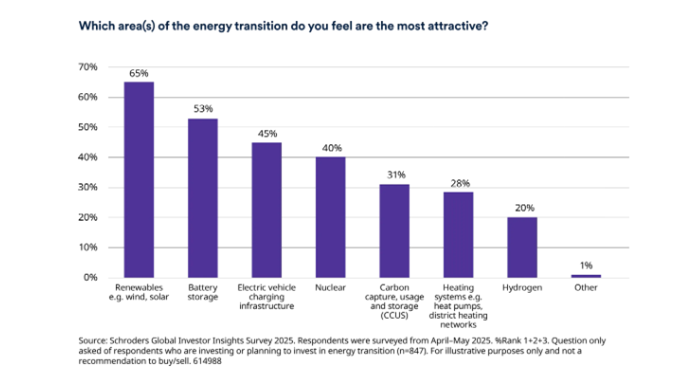

Investor interest in private infrastructure and real estate, especially those aligned with long-term secular themes, remains strong. The energy transition stands out as a particularly attractive area. According to the survey, 86% of investors are already investing in this theme – or plan to do so – over the next year, with 75% targeting fully private or blended market exposure.

Key areas of opportunity include renewables (65%), battery storage (53%), and electric vehicle charging infrastructure (45%). Europe is seen as the most promising region for energy transition investments, with 69% of investors expecting the strongest returns from this area, supported by continued government support for renewable energy build out.

Minal Patel, Global Head of Infrastructure at Schroders Capital, commented: “The opportunity across the global energy transition is vast, global and growing. The investment set has become increasingly broad, with the range of technologies and energy transition sub-sectors that have evolved into viable opportunities with solid infrastructure characteristics for diversified, differentiated portfolios expanding significantly.”

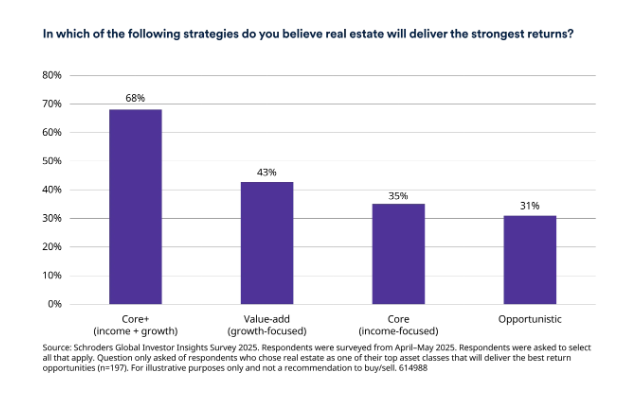

Meanwhile, within real estate investors are favouring regional and domestic strategies (49%) that can capitalise on uneven and substantial repricing across geographies and sub-sectors since 2022. Europe is the most favoured region (48%), with a pronounced tilt toward Core+ strategies (68%) that blend income and growth characteristics.

Read the full results of Schroders Global Investor Insights Survey 2025.