Rocks, hard places and everything in between

Izak odendaal, Old Mutual Wealth Investment Strategist

China’s leader Xi Jinping hailed his country’s advanced military capabilities last week as he presided over a massive military parade in Beijing. The occasion was the commemoration of the 80th anniversary of Japan’s surrender and the end of World War II. No leaders from the West were in attendance of the event, which one commentator described as aimed at showing that China was “a great power rooted in the developing world”.

This is a difficult moment for developing countries, squeezed between the world’s two superpowers, America and China, but also facing disruption from artificial intelligence and climate change. They’re witnessing China becoming more assertive on the global stage, while the US becomes more unpredictable and less friendly, as seen in the devastating cuts in foreign aid that hit the poorest countries hardest and the sharp increase in import tariffs.

Before going further, it should be remembered that we are talking about a very diverse group. Some will happily align with one of the superpowers, while others will try to steer a middle ground. They also have different economic dynamics and usually only have one thing in common: they are not rich. However, even that oversimplifies things slightly. South Korea, for instance, counts as an emerging market according to index providers like MSCI even though its economic sophistication and high living standards put it on par with many developed countries. This is because MSCI considers how easy it is for global investors to enter and exit a market, and Korea scores poorly on that count. The other thing to note is that not all developing countries are on investors’ radar screens. MSCI classifies developed economies as part of the World Index (23 countries), while developing economies fall into the Emerging Markets Index (24 countries) or the second tier Frontier Markets Index (28). This still leaves out more than 100 countries whose capital markets are too small or restricted to warrant index inclusion.

The diversity between emerging countries therefore means that grouping them together should only be done with a pinch of salt, while any thorough discussion of the topic will necessarily be long. There is only space here to make five quick points.

Weak dollar benefit

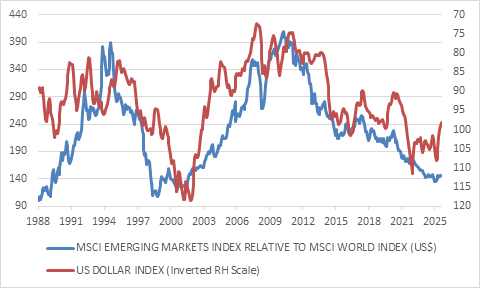

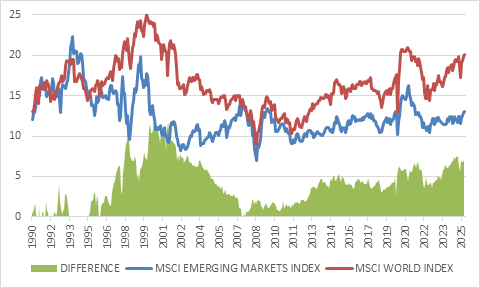

The first is that there is another commonality between emerging markets: they tend to benefit from a weaker US dollar since so many of them trade and borrow in dollars. As their currencies appreciate, there is also room to cut interest rates, stimulating domestic economies and financial markets. A weaker dollar also encourages capital inflows, since investors have greater certainty of earning a return in dollars. One of the biggest challenges in these countries is that the returns on offer might be compelling, but not so much when translated back into hard currency. . Simply put, periods of superior emerging market return in bonds and equities have usually coincided with a weaker US dollar as chart 1 shows.

Chart 1: Emerging versus developed market equities and the dollar

Source: LSEG Datastream

Countries that run current account deficits are particularly exposed to the dollar cycle and shifts in global risk appetite. They rely on portfolio inflows and continuously face the risk of a “sudden stop” in these inflows or destabilising rapid outflows, and must often maintain relatively high interest rates to keep the money coming in. An episode of risk aversion, even if it is related to something that happens in the US or Europe and not in emerging markets, can cause havoc as investors pull their money out.

Cutting cycle

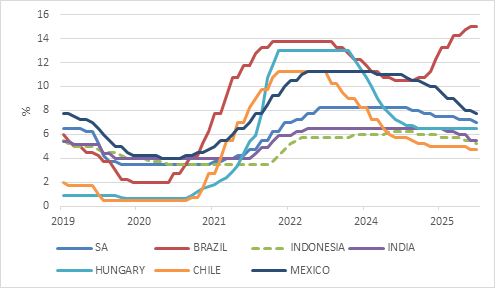

Secondly, and related to the above, most emerging markets have been able to cut interest rates despite the uncertain global climate. This offers support to their economies and markets. It is also notable that they came through a sharp post-Covid hiking cycle relatively unscathed without plunging into recession. Even Brazil, who experienced one of the biggest increases in interest rates, and who has been an outlier in not cutting recently, might’ve been expected to see its economy in the doldrums. In fact, it seems fine.

Chart 2: Policy interest rates in selected emerging markets

Source: LSEG Datastream

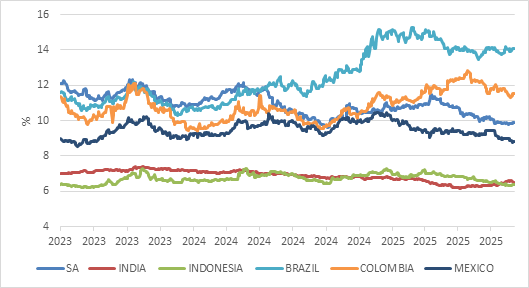

Also notable is that the recent increase in long-bond yields in many developed countries has not spilled over to the large emerging countries. Markets are seemingly able to discern between countries, such that France’s debt problems are not India’s or Chile’s. Having said that, the bond sell-offs in France and elsewhere have been orderly and mild.

In years gone by, we might have seen weakness in one country spilling over to others as in the 1998 emerging markets crisis. That it hasn’t happened is largely due to better macroeconomic policies in these countries, such as floating exchange rates, forex reserve buffers, inflation targeting and the fact that there was no borrowing binge in recent years. Some of the larger emerging markets have deliberately tried to develop local currency bond markets, thereby avoiding the “original sin” problem of having to borrow abroad and facing the challenge of having to earn enough hard currency to service the debt while being exposed to exchange rate risk. South Africa doesn’t is not guilty of this original sin, since it has always mostly borrowed in rands in the local bond market.

Chart 3: 10-year government bond yields, selected emerging economies

Source: LSEG Datastream

Thirdly, the traditional attraction of emerging markets in global financial centres like New York and London was growth. These countries should theoretically have higher rates of economic growth as populations urbanise and productive capacity catches up with the West, supporting company earnings.

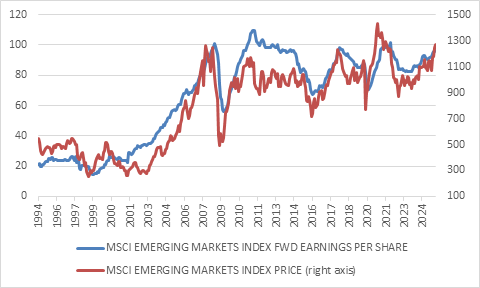

However, GDP growth does not always translate into profit growth. The MSCI Emerging Markets Index has shown virtually no growth in earnings per share over the past 15 years, though a close look at chart 4 shows an upswing since mid-2023. Part of this 15-year drought is a stronger dollar, partly due to foreign companies competing with less profitable domestic companies. But it also points to the fact that in any country, the fruits of economic value-add are shared between the government, businesses and households, and the ratio of that allocation differs.

Chart 4: Emerging market equities price and earnings

Source: LSEG Datastream

It should be noted again that this is the aggregate picture with important differences. South Africa is a country where companies are profitable despite lacklustre economic growth. India has maintained high rates of real economic growth and rising profits.

China sits at the other extreme. Chinese living standards have increased dramatically and it is rapidly becoming not just the world’s factory but more specifically a top producer of cutting-edge technological products, including more recently electric vehicles. At the same time, however, over-competition and weak demand mean it is experiencing deflation, an environment in which companies struggle to make profits. Only in the last 12 months has the government started campaigning against “involution,” the cutthroat competition, overcapacity and price-cutting behaviour. For instance, there are still more than 100 electric vehicle brands, though only a handful are likely to survive. One outlet for this excess production is exports but with the US market increasingly closed, a larger share of these goods must end up in other emerging markets, potentially undermining industrial development in those countries. This goes well beyond cars, but vehicles are emblematic of the problem because we can all see how popular Chinese brands have become in South Africa due to quality and affordability. This threatens local auto manufacturing.

No golden age

This leads us to the fourth point: the contrast with what was perhaps the golden age of emerging markets, the early 2000s, when China’s rapid industrialisation and urbanisation was a rising tide that lifted boats across the developing world due to its voracious demand for commodities and other inputs.

This continued for a while after the 2008 financial crisis when interest rates collapsed to zero and capital flooded into emerging markets in search of yield. It is hard to believe now, but in 2010 Brazil’s finance minister famously complained of “currency wars”. In other words that his currency was too strong! Be careful what you wish for. By around 2013, the dollar cycle had turned, China’s growth was slowing, and commodity prices were plunging. Brazil experienced a very deep recession in 2014 and 2015. The lost decade of emerging markets underperforming developed market equities (mainly the US) was well underway.

China’s demographic profile is a big reason why its growth rates should continue slowing, and therefore not contribute as much to the growth of other emerging markets in future. Of course, ageing creates fantastic opportunities in China’s “grey” economy, but these will largely be for the benefit domestic services companies.

Developing countries in general have better demographic profiles than developed countries, but there are a few with surprises. Brazil’s median age is 35 and Chile’s is 36, not far off from Australia and New Zealand at 37. Thailand’s median age is at 41, similar to Norway. Hungary and Bulgaria are at 44, the same as Switzerland. Several emerging markets are at risk of growing old before they grow rich.

The countries with the lowest median ages and highest fertility rates are overwhelmingly in Africa as indeed are most the world’s fastest growing economies. Business opportunities therefore abound, but small and underdeveloped capital markets mean they are not on the radar screens of global investors, except those who specialise in “frontier” markets.

What this implies is that another wave of synchronised rapid economic growth across the developed world seems less likely than in the past. A few countries like India seem to have the ingredients for sustained economic growth at a high rate, but the dream of catching up with rich countries is out of reach for most. In fact, only a small handful of countries have ever managed to transition from poor to rich.

Chart 5: Forward price: earnings ratios

Source: LSEG Datastream

However, and this is the final point, emerging markets are due for a cyclical rebound after a tough period. With equities still trading at a big discount to developed markets, bond yields attractively high and currencies largely on the cheap side versus the US dollar, there is room to run. After a long period of underperformance, emerging markets can have their moment in the sun again, this time without the weight of expectations. This is very much the case for South Africa too.