The elephants in the room

Izak Odendaal, Old Mutual Wealth Investment Strategist

There is an old African proverb that says when two elephants fight, the grass suffers. US President Donald Trump and Federal Reserve Chair Jerome Powell are arguably the two most powerful men on earth, although for different reasons. Their fight this year has, fortunately, not trampled markets underfoot. However, it offers a useful way to look at the US economy and what it means for investors.

According to Trump, the US economy is experiencing a boom. “Under President Donald J. Trump’s bold pro-growth policies, American businesses are thriving like never before”, a recent White House press statement read. Even allowing for some poetic license, this is surely an exaggeration at a time when businesses in the US and abroad face extreme uncertainty. Having said that, economic activity remains surprisingly resilient compared to expectations that the wild policy swings this year would cause business activity to decline sharply. The indices in Chart 1 fall below zero when economic data disappoint relative to economists’ forecasts. The last few weeks the US and Eurozone indices have held up, though July data from China has pulled its index into negative territory.

Chart 1: Citigroup economic surprise indices

Source: LSEG Datastream

It helps that the US economy was in good shape heading into the year. Growth in consumer spending has slowed, but from a high level. However, it appears to increasingly be held up by wealthier households, who benefit from a rising stock market, among other things. Considering data points like credit card defaults, lower income household are feeling strain. It also helps that fiscal policy is very loose – i.e. the government is borrowing and spending freely, while tax cuts will also take effect next year. Some businesses also benefit from deregulation, but the US economy was not overregulated to begin with.

Under pressure

If the economy was in such great shape, why has Trump and his team argued so forcefully for lower interest rates? Trump has badgered Powell to urgently cut the fed funds rate. As he can’t legally fire the Fed chair, he has resorted to other forms of pressure. The latest is calls that a member of its board of governors should resign for allegedly cheating on a mortgage application.

At this point, it is probably not only about interest rates, but also about control and dominance. Nonetheless, Trump has said he wants lower borrowing costs to reduce the government’s interest burden. Despite the additional hundreds of billions that Trump’s import taxes will bring in, the federal government’s deficit looks set to keep rising. The problem of course is that the government doesn’t borrow at the fed funds rate, which is an overnight rate in the interbank market. The government borrows in bond markets, typically at longer maturities, and the market is still allowed to make up its own mind. The risks of high future inflation from a loss of Fed independence can put upward pressure on long-term bond yields, even if short-term interest rates are cut. Rising government debt levels are probably also leading to higher long-bond yields, even as the market prices in rate cuts.

Chart 2: US interest rates

Source: LSEG Datastream

An ancient Indian parable talks of a group of blind people encountering an elephant for the first time. Each only feels one body part, the tail, the tusk, the trunk, a leg, and an ear. Based on their individual experiences, they describe what they are feeling as a rope, a spear, a snake, a pillar, or a fan. They argue, convinced that they are right, but no-one sees the full picture. In contrast to Trump’s rosy view of the US economy, the full picture is more complicated, with at least four cross-currents.

Firstly, there are the tariffs, a big tax increase that falls mostly on American businesses. So far, it appears that they’ve been unwilling or unable to pass the cost on to consumers in the form of higher selling prices. There is also little evidence of exporters in other countries slashing prices to accommodate customers in America. Since the tariffs only came fully into force in August and firms were able to stock up earlier in the year, the impact will take time to be felt. The CEO of Walmart, America’s largest retailer confirmed this last week noting that as “as we replenish inventory at post-tariff price levels, we’ve continued to see our costs increase each week”. He also noted that the company was trying to avoid raising prices for consumers. It is not clear whether it can hold it off indefinitely, however.

Back-of-the-envelope calculations suggest that tariffs will raise about $300 billion a year for the government. The mammoth $29 trillion economy can absorb this tax increase, but it still amounts to more than $2000 per household. Of course, the burden is not equally distributed, and smaller businesses and lower income households who spend a larger portion of income on goods will be hardest hit.

Will there be inflation from the tariffs? A one-off rise in tariffs will cause a 12-month bump in inflation numbers. The question is whether businesses, including those not directly affected, will use it to raise prices, and whether workers will be able to negotiate compensating wage increases. If the answer to the latter two questions is “yes”, there might be sustained inflationary pressure. But in a cooling labour market, it shouldn’t be the case.

The second cross current is that labour demand and supply dynamics have shifted. Companies seem to be hiring fewer workers, partly due to the uncertainties mentioned above. But with immigration clampdowns and expulsions, labour force growth is down to a trickle. It turns out the red-hot jobs market between 2022 and 2024 was fed by a surge in immigration that is now behind us. Apart from the longer-term demographic implications, it means there might be shortages of workers in some sectors, notably agriculture and construction even if the economy slows. It also means that the unemployment rate, currently at only 4.2%, will not necessarily rise if there are layoffs, since a decline in labour supply could match the decline in demand. For now, however, there are few signs of rapidly rising retrenchments. In an economy as large as the US, people are always losing their jobs. However, new claims for unemployment insurance have hovered around 200,000 per week for the last few years, though with a strong seasonal pattern.

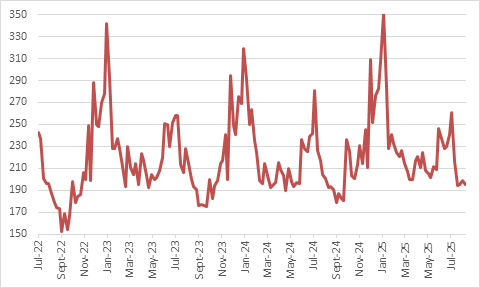

Chart 3: US initial jobless claims (not seasonally-adjusted)

Source: LSEG Datastream

Thirdly, the housing market has been characterised as “frozen” for some time, but things have been getting worse recently in what remains a key cyclical sector. Many homeowners locked in very low pandemic-era mortgage rates that they don’t want to lose by moving house now. The current mortgage rate is around 6.6%, twice what it was in 2021. Prices remain elevated, however, meaning that it is tough for new buyers too. Since mortgage rates are linked to bond yields, not the central bank’s policy rate as in South Africa, rate cuts will not help unfreeze the market if the yield curve steepens.

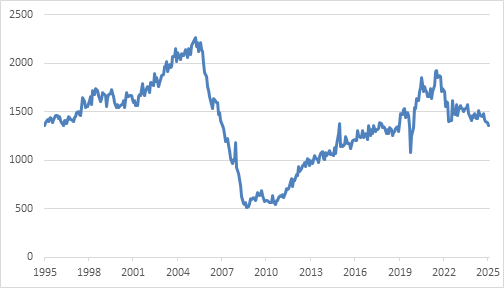

For homebuilders, higher tariffs on imported Canadian timber or Korean steel squeeze profits, while getting workers is also a challenge. This discourages new building activity and contributes to the sharp declined in building permits passed, a key leading indicator of housing market activity.

Chart 4: US approved building permits

Source: LSEG Datastream

Finally, there is artificial intelligence (AI). The massive AI-related capital expenditure, including building new data centres, is estimated to be around 1% of US GDP, not dissimilar from internet-related spending late in the dotcom bubble. This is a notable injection into the US economy and seems no sign of slowing while other sectors face headwinds from tariffs and interest rates.

However, with AI there are more questions than answers. We don’t know if it is the productivity miracle some say it is. If so, it might solve some of the labour shortages though it is unlikely to play much of a role in harvesting strawberries or putting up rooftiles, for instance.

Since AI is extremely energy-hungry, it is not clear whether the US energy grid will cope without raising prices for other consumers. But the biggest question is probably whether all this frantic spending will generate a return. Even if AI turns out fantastically useful for the broader business community, much of the investment in physical infrastructure might not be very profitable. At worst, they might be white elephants. If that realisation dawns, capex plans could be scaled back very quickly. Even OpenAI founder Sam Altman noted recently that investors were getting “overexcited” but insists his firm will continue spending, nonetheless. This is also a question for the equity investors who are buying AI-shares at eye-wateringly high valuations in public and private markets. These companies could go on to do great things, but if they are already priced for perfection, where is the long-term upside? On the contrary, the slightest disappointment could lead to significant downside.

On the tusks of a dilemma

Where does this leave Jerome Powell? His dilemma is that tariffs threaten to pull the Fed’s mandate in different directions. He has so far stood firm in resisting political pressure to cut rates, insisting that any moves will be based on a sober assessment of the economic outlook. This assessment is now pointing towards easing. In his highly anticipated address to the annual central banking conference in Jackson Hole, Wyoming, on Friday, he noted that the economic picture was much more complicated than this time last year. While acknowledging the potential inflationary risks from tariffs, he also argued that there are risks to employment, despite the “curious” balance of both lower demand and lower supply.

He sees interest rates in restrictive territory, which should take care of inflationary risks. To forestall a worsening of the employment situation, however, rates could fall somewhat. He noted that “the shifting balance of risks may warrant adjusting our policy stance,” leaving the door open to a rate cut at the September policy meeting without committing to anything. While Powell did not address the political pressure on him and his colleagues, a cut could defuse the tensions somewhat without hurting the Fed’s credibility. Both elephants could get what they want. It is what happens in the subsequent months that will matter. Powell’s term as Chair ends in May and Trump will almost certainly appoint someone seen as more pliable.

For the time being, markets like what they’re seeing, notably looming interest rates cuts, a relatively resilient global economy despite tariff headwinds, and ongoing AI spending. The glass appears to be half full across US equity and credit markets. Not all of this will play out as expected, and with valuations stretched, there is room for disappointment. But it is worth remembering the following: while we all experience this uncertain global environment, the responsibility to respond weighs heavier on some. Someone like Powell is forced to act by the nature of his roles, while others can sit back and try to ignore the noise. If you are a long-term investor nervously trying to make sense of all this, bear in mind that you don’t need to do anything if you have a sensibly diversified portfolio. But you will need patience. Like another old proverb has it, the only way to eat an elephant is one bite at a time.