The empire strikes back

Legacy software giants regain ground in the cloud wars

By Paddy Flood, Portfolio Manager and Global Sector at Schroders

When disruptors dominate the narrative, incumbent comebacks can create opportunities for active global investors.

Technology is a dynamic industry and one that, relative to other sectors, tends to exhibit greater obsolescence risk. Innovation in technology is relentless, and the ongoing push to advance the frontier of what’s possible often leads to the displacement of incumbent products, platforms, and companies. In many ways, the sector is defined by a continuous cycle of challenge and reinvention - where even the most established technologies can quickly lose relevance.

There are countless examples. Vinyl gave way to CDs, which were replaced by MP3s, only to be overtaken by streaming, thanks, in part, to better storage and connectivity. Landlines lost out to mobile phones, which were later subsumed by the smartphone. It’s a world where the dominant platform of one era can swiftly be overtaken by the next - a reminder that, as in certain long-running film franchises, the fall of an empire is never out of the question.

This dynamic has played out clearly in the enterprise software space. Over the last 15 years, the rise of cloud-native and Software as a Service (SaaS) companies transformed how business software is consumed and delivered. These firms - including Salesforce and Workday - rapidly gained share, taking advantage of a model where software could be accessed over the internet, paid for via subscription, and supported by infrastructure managed by third parties.

The benefits were clear: lower upfront costs, scalability, outsourced complexity, and faster deployment cycles. The contrast with legacy models - where customers had to operate their own data centres and purchase costly, perpetual licenses - was stark. As a result, newer players grew faster, were awarded premium valuations, and were widely viewed as the future of enterprise IT.

During this period, traditional software vendors like Oracle and SAP appeared increasingly out of step. Their models were seen as dated, their product portfolios as inflexible. The market narrative that emerged was one of maturity and, in some cases, structural decline - a belief that these legacy players would struggle to remain competitive as the market shifted decisively to the cloud.

This narrative created - and in some instances still creates - significant opportunity for discerning, forward-thinking investors willing to challenge consensus and identify where market expectations may be misaligned. This is exactly what the Global and International Equity team’s philosophy is designed to do: identify mispriced growth through the lens of the “growth gap” where we compare our expectations of future growth to those implied by the market. And importantly, we look for these opportunities globally - not just in the US - because structural change and innovation are not confined to any single geography.

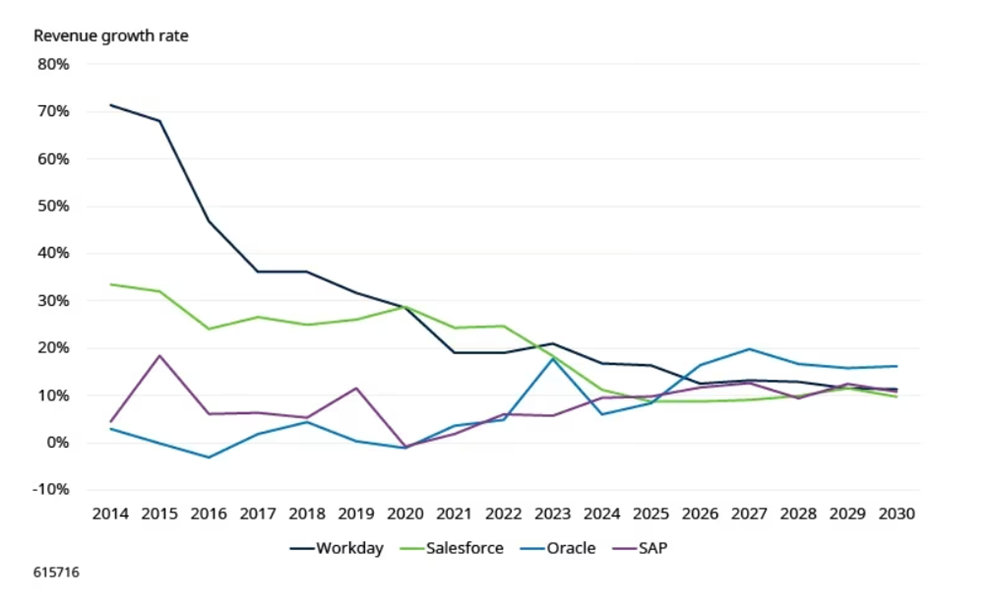

A clear example of this is challenging the assumption that US-based Oracle and German-based SAP were in structural decline - a view that underestimated both the resilience of these companies and their capacity to adapt. While cloud-native firms received much of the attention, Oracle and SAP began reshaping their businesses. SAP transitioned its flagship ERP suite to a cloud-first model, while expanding its SaaS portfolio and acquiring complementary assets. Oracle rebuilt its database and application stack for the cloud and made significant infrastructure investments.

Today, the gap between the disruptors and the incumbents has narrowed. In fact, as a result of these changes, both Oracle and SAP are now growing as fast - in some cases faster - than the SaaS companies that once threatened to leave them behind. Their cloud businesses are scaling, and the market is beginning to acknowledge the durability of their customer relationships and the strength of their execution.

Legacy leaders regain momentum: SAP and Oracle close the gap

Source: Bloomberg, Schroders, July 2025.

This shift offers a valuable reminder for investors. In periods of disruption, the market often gravitates toward the narrative of the upstart. That instinct is sometimes justified - certain transitions are permanent and one-directional, with incumbent companies continuing to disappoint. But not all legacy firms are destined to be left behind. In areas like enterprise software, where products benefit from high barriers to entry and switching costs, and where incumbents demonstrate a willingness to adapt, it is entirely possible for established players to not only survive but emerge stronger.

In the case of enterprise software, it’s clear that the incumbents are no longer on the defensive. The market has underestimated their staying power - a dynamic that has, and likely will continue to, create opportunities for active global investors willing to challenge the status quo across geographies. The empires, so to speak, are striking back - and in doing so, may offer overlooked opportunities for long-term investors.

Any reference to regions/ countries/ sectors/ stocks/ securities is for illustrative purposes only and is not a recommendation to buy or sell any financial instruments or adopt a specific investment strategy.