The madness and the mundane

Izak Odedaal, Old Mutual Wealth Investment Strategist

The most overused word of the year, “uncertainty,” is being put to work again. The conflict between Israel and Iran has now drawn in the US. American bombers hit three sites in Iran on Sunday, with the stated aim of destroying Iran’s nuclear capabilities. While US President Trump claims that he has achieved his goals and that there won’t be further strikes, it largely depends on how Iran retaliates. This could be the end of the conflict or just the beginning. There are several American military bases in the region that Iran could target. As an act of desperation, it could block maritime traffic through the Strait of Hormuz, a narrow chokepoint through which about a fifth of global oil is transported. Trump, meanwhile, risks fighting a military war alongside a trade war, creating political risks for himself having promised to keep the US out of foreign entanglements, and economic risks for the rest of the world.

Black gold

Wars cause human misery, but investors mostly care about the Middle East because of oil. Those who study history know how the Arab Oil Embargo in 1973 and Iranian Revolution in 1979 sank markets and crippled the world economy. More recently, we saw a global inflation surge following Russia’s full-scale invasion of Ukraine.

Chart 1: Brent crude oil price

Source: LSEG Datastream

The oil price increased in recent days as traders fear supply disruptions. When markets opened on Monday morning, it briefly jumped above $80 a barrel, the highest level since January, but still within the broad trading range of the past two years. As Chart 2 shows, the oil price was in line with its long-term average in real terms at Friday’s close. War and geopolitics caused a cumulative sixfold increase in the 1970s, while 2008 saw another extreme move due to the fear that strong demand would outstrip dwindling supply (in reality, the world was nowhere near “Peak Oil” supply while the high price was undermining demand by the minute). Two other notable spikes were in 1990 when Iraq invaded Kuwait and in 2022 following Russia’s attack on Ukraine. In contrast, America’s 2003 invasion of Iraq barely registers.

Chart 2: Real oil prices

Source: LSEG Datastream

Higher oil prices will raise fuel prices across the world and put upward pressure on inflation. Those two things are not quite the same. Higher fuel prices could lead to ongoing inflation if firms pass the costs on to consumers, the so-called second round impact, or it can simply make everyone poorer (a similar logic applies to Trump’s tariffs). The oil price is essentially a global tax, and the higher it is, and the longer it remains elevated, the less money businesses and consumers have to spend on other things. Producers obviously benefit, but higher oil prices would be a net negative for global economic growth.

It should be noted that the world economy is much less dependent on oil than in the 1970s, so even an extreme move in the oil price would cause as much damage as it did back then. If the Strait of Hormuz is closed, for instance, the oil price could well revisit the $130 per barrel level it briefly hit after Russia’s 2022 invasion of Ukraine.

Russia very deliberately used energy prices as a weapon in 2022, especially when it throttled gas supplies to Europe. It inflicted economic damage since its western neighbours relied on piped gas that could not immediately be replaced by seaborne gas. Moreover, with Russia and Ukraine being major grain exporters, food prices also jumped in 2022, adding to an international inflation surge that was already underway as the world economy rebounded from Covid lockdowns. The rebound also meant firms could pass on cost increases to customers, maintaining or even expanding their margins. Some called this “greedflation” and others “profit-led inflation”. Either way, it relied on firms having pricing power, something that is not obviously the case today. Therefore, 2022 is also not a perfect analogy for the current situation.

One further reason is that global oil supplies were tight in 2022, but less so now. Indeed, on the eve of Israel’s strikes on Iran, Brent crude was trading around $65 per barrel. Further price moves do not only depend on Iran’s actions, but also on what other major oil producers do, notably the OPEC cartel. OPEC has spare production capacity, and the likes of Saudi Arabia and UAE are not particularly sympathetic to Iran. They don’t necessarily want a much higher oil price that might encourage US shale producers to increase output. Moreover, a global economy under pressure from US tariffs might not be able to handle sustained higher oil prices, leading ultimately to falling oil demand. That is not a desirable outcome from their point of view.

Hit by sanctions and years of underinvestment, Iran’s oil exports are around 2% of the global total. Unlike Russia in 2022, Iran has little to gain from weaponizing energy prices, other than some leverage in future negotiations and winning back lost pride. It has few allies, with China probably being the closest and biggest export market for Iran. China does not want higher oil prices. There is also the question of whether Iran will be able to sustain attacks on oil infrastructure in the region given the weakened state of its military, its stagnant economy and unhappy population.

Trade war and peace

While we shouldn’t be complacent, it therefore still appears that the fate of the world economy this year and into the next will rest more on traditional economic policies than on geopolitical shocks.

There has been some good news on the tariff front, but much remains unknown. The US and China have extended their trade truce following recent meetings. While details are sketchy, it still appears that extreme tariff outcomes will be avoided. The same is also likely to happen in discussions with other countries, but these are still underway with mixed success to date. The 90-day pause on the implementation of “reciprocal” tariffs expires in two weeks, and countries like South Africa await news on the level of tariffs they face. Again, the market consensus seems to be that US tariffs will be higher than at the start of the year, but not as high as threatened on 2 April.

This still implies that American consumers face higher prices down the line, while American businesses will see their profit margins squeezed. It also means that other countries will lose some export revenues. The evidence of this is limited so far, but the economic data is distorted by the fact that many businesses stockpiled goods earlier in the year, while consumers also brought forward some purchases to avoid higher prices. The announcement and subsequent suspension of tariffs on China will probably give rise to another wave of stockpiling. Another factor making it difficult to gauge the underlying health of the US economy is the immigration crackdown that is impacting labour supply. The full picture will emerge over the next few months.

This has also been the view of the US central bank, the Federal Reserve, whose policymakers met last week (before the attacks on Iran) to decide on interest rates. The Fed has a dual mandate, full employment and price stability. In practice this means it aims to maintain a low unemployment rate and inflation close to 2%. It gets to put a tick next to the first part of its mandate. As the post-meeting statement noted, the US economy remains solid, with unemployment still low. Inflation, on the other hand, is viewed as “somewhat” elevated.

Headwinds

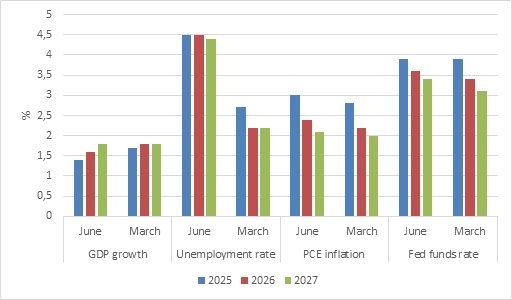

Looking ahead, however, the economy faces headwinds from tariffs and this is likely to lead to pressure on the labour market. At the same time, tariffs could derail the downward trend in inflation (the same is true of higher energy prices) This is reflected in the quarterly summary of economic forecasts of Fed officials, otherwise known as the dot plot, which shows a weaker growth outlook compared to March, but also higher inflation.

Chart 3: Fed Median Summary of Economic Projections

Source: Federal Reserve

The Fed’s dual mandate is therefore being pulled in different directions, and as a result, it kept interest rates unchanged. Fed Chair Jerome Powell noted in the press conference, “Ultimately the cost of the tariff has to be paid, and some of it will fall on the end consumer. We know that’s coming, and we just want to see a little bit of that before we make judgments prematurely.” However, some voices within the Fed are arguing for acting sooner, before the economy slows down. There is the possibility that the Fed waits too long looking for the impact of tariffs while the underlying health of the economy steadily deteriorates. This is ultimately a bigger risk for markets than what happens in the Middle East and requires close monitoring.

As for the South African Reserve Bank, Governor Kganyago will probably feel lucky that he scheduled the next Monetary Policy Committee for 30 July. This will give him and his colleagues time to assess where the oil price and rand-dollar exchange rate settles. On Friday, the rand oil price was still 7% lower than a year ago and not ringing alarm bells, but this could still change in the days ahead.

Chart 3: Oil in rands

Source: LSEG Datastream

It will also have sight of June’s inflation data. May’s inflation was probably the bottom of the cycle, but at 2.8% it was below the Reserve Bank 3% to 6% target range for the third month in a row, It should drift higher from here and remain close to the 4.5% target over the medium term, unless the global environment changes dramatically. There has been no formal announcement on moving the inflation target as yet.

Risks and opportunities

There are three final points to highlight regarding the uncertain situation in the Middle East. Firstly, the geopolitical landscape is shifting. If the US is attacking smaller countries – whether justified or not – without support of the international community through the United Nations for instance, what is to stop other large countries such as China from doing the same by invading Taiwan? As with Trump’s tariffs, it is another sign of the fraying of the world order that America itself constructed over the past 80 years.

Secondly, this brings risks and opportunities. Energy is an obvious example. The Middle East matters to rest of the world largely due to our ongoing addiction to oil. However, every time there is a worry about security of oil supplies, it encourages the rest of the world to turn to other forms of energy and sources of oil in quieter parts of the world. The upheaval of the 1970s led to more energy-efficient cars, a surge in nuclear power station construction, and also the development oil fields in the North Sea and elsewhere. Today, electric vehicles are ready to increase market share. Nuclear is in the early stages of making a comeback while solar and wind continue to expand, while a country like Namibia is a promising prospect for drillers. This has broader economic implications. Oil is globally traded and transported, but renewable energy tends to be local. In other words, it is not just about the energy source but the entire layer of economic activity that supports it. The world economy will always need energy. Artificial intelligence, for instance, is not something that happens in the ether somewhere, it is ‘manufactured’ in extremely energy-intensive datacentres.

Thirdly, while these geopolitical events hog the headlines and cause market volatility, long-term equity market returns are driven by something much more mundane, namely the profits generated by companies across the world, and a willingness to remain invested and benefit from the power of compounding. The mad events of the past two weeks do not change this.