The Stock Market is not the Economy

By: Izak Odendaal, Old Mutual Wealth Investment Strategist

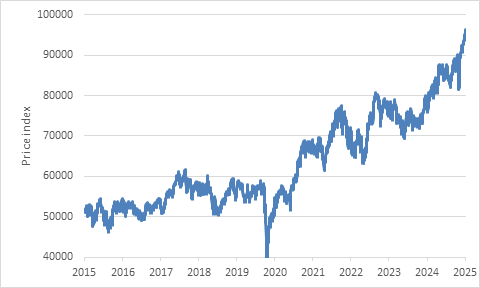

This might be a puzzle to many. How can the JSE All Share Index cross 96,000 points for the first time in the same week when the latest data indicated the South African economy only grew 0.1% in the first quarter? We can expand the question globally. Why are equity benchmarks in countries like Canada and Germany – both big exporters to the US – hitting record highs while global economic growth forecasts are being downgraded because of US trade policies?

Chart 1: FTSE/ JSE All Share Index

Source: LSEG Datastream

Let’s start with the global picture. Of course there is never just a single answer, but rather a confluence of factors. And even after we’ve explained these, there is always that touch of mystery. After all, we are dealing with the decisions of millions of people here.

The global growth outlook has certainly deteriorated since US President Donald Trump launched his trade wars. Tariff barriers will lead to downward pressure on the real incomes of American businesses and consumers and weight on the export earnings of other countries.

The OECD, a large think tank representing a club of advanced economies, released its updated global forecast last week. It showed that the global economy will only grow by 2.9% this year, down from the 3.1% it expected previously, and falling from 2024’s growth rate of 3.3%. That seems like a small difference, but on a $110 trillion global economy it amounts to hundreds of billions of lost potential income and output. The OECD expects growth of 2.9% in 2026. So overall, not a pretty picture. But the details matter.

The US faces the biggest expected downshift in expected growth of all the large economies, from a healthy 2.8% in 2024 to only 1.6% this year and 1.5% in 2026. For some other countries, however, the trajectory is upwards. Germany’s growth rate is projected to rise from -0.2% in 2024 to 0.4% this year and 1.2% in 2026. Not big numbers in absolute terms, but an improvement. Japan’s growth rate is expected to rise from 0.2% last year to 0.7% this year. The UK is also expected to show a somewhat better growth rate this year compared to last year.

In other words, equity markets are looking ahead, not backwards. The OECD expects South African growth to rise to 1.3% this year from 0.6% last year.

Policy support

Another factor is that central banks are cutting interest rates outside the US and Japan. Lower interest rates do not only cushion the economy, especially in Europe and other countries where variable rate loans predominate but also make equities more attractive. Other forms of policy support also matter, notably Germany’s rearmament programme and China’s fiscal support.

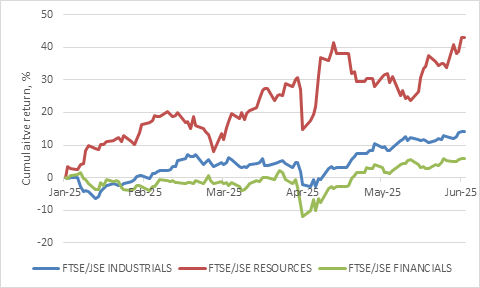

Chart 2: Selected equity benchmarks in US dollars

Source: LSEG Datastream

Thirdly, there is simply the fact that the shine has come off the “American exceptionalism” notion. Trump’s erratic policymaking style, particularly on trade, is causing a big rethink among global investors, as is the concern over a massive rise in US government debt. Suggestions that foreign portfolio investments could face taxes doesn’t help.

It doesn’t mean that the US will be abandoned altogether. It will always be too big to ignore and will continue to be the home of the world’s leading companies. However, global investors are waking up to the fact that they are potentially overexposed to the US and are looking for alternatives. This has supported markets outside the US. Importantly, the US stock market came into 2025 priced for perfection. Markets elsewhere were fair to cheap. This means that the risk-return payoff profile for US equities has deteriorated relative to other markets.

The US dollar’s 15-year bull market also supported US equities outperforming the rest of the world. As the dollar rallied against the euro, for instance, investors in Europe got an additional boost to the returns of their US equity and bond portfolios. This encouraged them to increase allocations to American assets. However, if the dollar continues declining, which seems a reasonable assumption although it will not happen in a straight line, it will detract from the US investments of global investors. Again, this forces hedge funds, pension funds and insurers in Europe, Asia and elsewhere to rethink US exposure and look for alternatives.

A weaker dollar would also be good for growth in emerging markets, creating another reason for investors to look more broadly than the US tech shares that drove the S&P 500’s massive outperformance over the past decade.

Through the windshield

The same pattern happened in South Africa too. Returns from offshore investments were boosted by a weaker rand over the last 15 years. This in turn encouraged local investors to take money abroad, while South African companies made acquisitions abroad with decidedly mixed results. It discouraged foreigners from investing here, since while they can hedge out exchange rate movements, it is relatively expensive given high local interest rates. Offshore investing makes a lot of sense for South Africans, given the diversification benefits and larger opportunity set. Many South African investors remain overexposed to their home market. However, many locals were investing through the rearview mirror, chasing the performance of the winning asset class of the day. This always poses risks, and investors should rather be looking ahead through the windshield.

Chart 3: South Africa’s real economic growth forecasts

Source: OECD, SARB, Treasury, Reuters

The economic picture in South Africa remains mixed. As noted, real first quarter gross domestic product (GDP) growth was only 0.1% on a quarter-on-quarter basis. Compared to the first quarter of 2024, real GDP was 0.8% larger. Add back inflation, and nominal growth was 4.4% year-on-year. This is hardly exciting.

The first quarter saw a 4% quarter-on-quarter decline in mining output, despite firm precious metals prices, and also weakness in the manufacturing sector. The end of persistent loadshedding has not helped these two electricity-intensive sectors much, partly due to ongoing logistical challenges. On both fronts, there should be an improvement over time. For instance, the Department of Transport announced last week that it received 162 formal responses to a request for information on private sector participation (PSP) in the country’s rail and ports system, mostly on the mining corridors. It is still early in the process, but PSP will lead to increased investment and improved operational performance in logistics.

Consumer spending, on the other hand, has firmed up, benefitting from lower interest rates and lower inflation. It was 3% higher than a year ago in real terms in the first quarter. More recent data from industry body Naamsa showed that new car sales rose 21% year-on-year in May, an indicator of improving consumer health.

Local is looking lekker again

How then do we explain the strong performance of local equities? It largely reflects the global factors listed above, but it should be noted that the JSE has outperformed the broader emerging markets index in dollar terms, so some local factors are at play.

The most notable such factor is the strong performance of mining shares. The local mining sector has shrunk in terms of output and employment over the past decade, weighed down by infrastructure bottlenecks, regulatory uncertainty and security issues. This is negative for the economy, the fiscus and job creation. The infrastructure issues are being addressed, but regulatory matters remain a bone of contention, while organised crime continues to be a scourge. Nonetheless, when commodity prices jump, so does the profitability of miners even if there is no increase in production. The dollar gold price has increased 28% this year, while platinum and palladium have increased 22% and 11% respectively.

This means the consensus earnings per share growth for the JSE’s resources sector of 2025 is 50%, and for 2026 it’s 25%.

Chart 4: JSE sectors in 2025

Source: LSEG Datastream

Some commodities are weaker, notably oil. This helps the profitability of most sectors apart from oil and fuel producers like Sasol. The iron ore price is also slightly weaker this year, while coal has fallen some 15%.

The financial sector on the JSE has benefited from lower inflation and declining short-term interest rates. Optimism that the country’s inflation target could be lowered has pulled long-term interest rates (bond yields) lower. Consensus earnings growth for the financial sector is around 9% per year in 2025 and 2026.

Among industrials, the winners this year have been Richemont, ABInbev and BAT, three large globally focused consumer companies and Naspers and Prosus, also effectively global companies. Local retail shares have been under pressure this year, despite rising consumer spending. However, this follows a strong rally last year. Consensus earnings growth for industrials is around 19% per year in 2025 and 2026.

The overall earnings growth outlook for JSE-listed companies is therefore healthy at around 20% this year and 15% next year, depending on the benchmark. The All Share Index is no longer widely used by fund managers, who generally prefer the Capped SWIX, but is still better known among the general public. It is clearly much faster than expected nominal economic growth, but this is always the case. The stock market is not the economy. Earnings growth has a bigger amplitude than economic growth on the upside and the downside. Moreover, stock market sectors do not align neatly with GDP sectors, with the government a third of the latter, while the former has a large exposure to overseas revenues. Finally, it is worth remembering that in a sluggish economic environment, the best companies can become more profitable, since their competitors fall away.

Chart 5: FTSE/ JSE All Share Index analyst consensus metrics

Source: FactSet, SBG Securities

In summary, the strong performance of several equity markets, including the JSE, might seem odd at first glance given the economic outlook, but is driven by explainable factors: the decline in the US exceptionalism idea, policy support and the earnings picture. This doesn’t mean that markets will keep going up in a straight line. That never happens. After a strong run, we are bound to see a pull-back at some point. However, valuations still support a positive long-term outlook for South African equity returns, and from selected global markets. Any equity investment should always be made with a long-term goal in mind, since anything can happen in the short term. This year has already demonstrated the latter point several times.