Wishing for White Flags

By: Izak Odendaal, Old Mutual Wealth Investment Strategist

On Thursday the world marks the 80th anniversary of the unconditional surrender of Nazi Germany and the end of World War II in Europe. Planning for the post-war world had started years before the fall of Berlin. This included arrangements for economic cooperation. It was understood that the Great Depression of the 1930s contributed to the rise of fascism, and that the sharp turn towards protectionism, notably the passing of the 1930 Smoot Hawley Tariff Act by the US Congress greatly worsened to the Depression. Mechanisms needed to be put in place to avoid a repeat. The post-war economic architecture (at least in the West) was agreed on at a conference in Bretton Woods, New Hampshire in 1944. This included the creation of the International Monetary Fund to help countries manage balance of payments difficulties, and the World Bank to fund reconstruction and economic development. A free trade agreement proved elusive, but by 1947 the General Agreement on Trade and Tariffs (GATT) came into existence and would oversee the gradual removal of trade barriers around the world. GATT was eventually replaced by the World Trade Organisation.

In all of this, the US played a key role. It was the undisputed economic and military superpower at the end of the war. Although it could have thrown its weight around, the US worked towards a world where even the vanquished Germany and Japan could flourish. It would continue to be a leader of this global system over the next eight decades, greatly benefiting from it, and allowing others to also benefit. For all the world’s many problems, it is more peaceful and prosperous than at any time in history, with people living longer and having access to more technology than ever before. Even a cheap smartphone today has significantly more computing power than the whole of Bletchley Park, the famed wartime British code-breaking centre. While the US itself had to cede ground to other countries in terms of its share of global economic activity, it was also richer and more productive at the start of 2025 than at any other time, and notably outperformed other advanced countries in recent years. Again, there are many problems and many unhappy Americans, but this is not a country that needed to be “Made Great Again” as was the case with devasted Germany and Japan in 1945, for instance.

In question

Needless to say, all of this is in question today. Under President Donald Trump’s America First banner, the US is seemingly turning its back on a free and open global economy (the original “America First” movement of the 1930s campaigned to keep the US out of global conflicts).

Although Trump suspended the “reciprocal” tariffs he imposed on 60 countries, he increased tariffs on Chinese imports to 145%. China is such an important supplier of manufactured goods to the US that, even with exceptions for smartphones and other electronics, as things stand, the effective tariff rate is around the level 20% set by the Smoot-Hawley Tariff Act. It was around 2.5% at the start of the year. This is a huge tax hike for American consumers. Meanwhile, China’s 125% tariffs on imports from the US mean profitable trade between the world’s largest economies looks impossible.

Many American businesses have warned that some products will become much more expensive or simply unavailable in the months ahead, while others fear much worse: bankruptcy and job losses. Small businesses with tight cashflow and constrained balance sheets are clearly more at risk. The good news is that the US economy came into this tempest in good shape, with healthy levels of consumer spending and business investment. This will give it some resilience, but not necessarily enough. It is also possible that the economy looks stronger than it is, since many businesses and consumers would have brought forward purchases in anticipation of tariffs.

Given all this, it might be surprising that the initial market shock from Trump’s April 2 “Liberation Day” tariff announcements has faded so quickly. Many equity benchmarks have already retraced their losses. This suggests that markets have sniffed out that Trump does not have the stomach for an extended trade war. After all, he has already made concessions. Investors believe that he will keep backing down and ultimately do deals with other countries, including China. There is a big debate whether the US or China has the upper hand in this conflict, but the bottom line is that both stand to lose from a protracted trade war.

In a democratic society, pressure for change can build quickly. Republican politicians have shown little appetite to rein in Trump, but they will face voters next year and still need the backing of big money donors from the corporate sector. And while Americans might be prepared to sacrifice their living standards for a higher purpose, that is certainly not what they signed up for. The biggest issue in the November election was lowering the cost of living, not raising it.

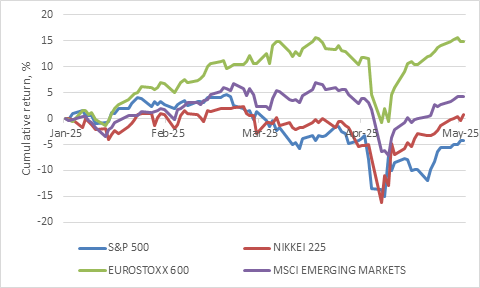

Chart 1: Global Equity indices in US dollars

Source: LSEG Datastream

Measured in dollars, global equities ended April in positive territory, despite large intramonth drawdowns and negative returns from the US. A weaker US dollar boosted returns from non-US markets such as Japan and Europe.

The S&P 500 Index lost only 0.7% in April and is still down 4% for the first four months of 2025, but was down 15% at the lowest point. Nonetheless, it is its worst start to the year relative to non-US equities since the early 1990s. The US market was considerably more expensive at the start of the year, with too much good news priced in. There was much more room for disappointment.

Local equities more than retraced their losses, and the FTSE/JSE All Share Index is at an all-time high of above 90,000 points. This is a 20%-plus return over the past year.

Chart 2: FTSE/JSE All Share Index in rand

Source: LSEG Datastream

While the equity market seems to be sounding the all-clear, the bond market is more circumspect. US bonds responded unexpectedly to the tariff shock. Instead of rallying, as is normally the case in a time of global market stress, government bonds (Treasuries) fell. This meant that the yield on the benchmark US 10-year Treasury rose from 4.2% to a peak of 4.5% intramonth, raising borrowing costs throughout the economy. However, yields have receded since, falling to around 4.2%. Despite the Federal Reserve being in a difficult position with its employment and inflation mandates potentially pulling it in different directions, the market now expects it to cut rates four times this year.

It should be noted, however, that while the volatility in the bond market has been elevated, yields remained within the broad trading range of recent years. This means that neither growth nor inflation fears have reached extreme levels. For instance, when Covid hit, the US 10-year yield fell a full percentage point in just three months. In 2022, the global inflation surge saw the yield rising two percentage points.

Chart 3: 10-year US Treasury yield, %

Source: LSEG Datastream

South African bonds were very volatile in the past month, responding both to global bond market volatility and concerns over the future of the government of national unity (GNU) amid deep disagreements on fiscal policy. These differences have seemingly been put aside, but investors will have to wait until 21 May for details on the third attempt at passing a budget. This time there will be no VAT increase and it will be based on a weaker growth outlook compared to Budget 1.0 tabled in mid-February.

Dollar doldrums

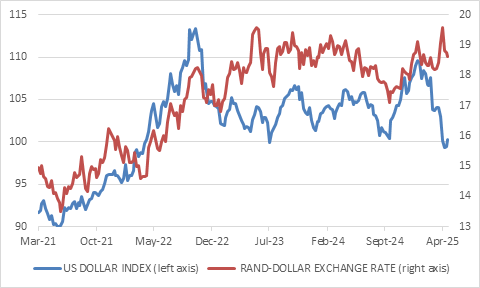

When it comes to foreign exchange, the standout feature is that the dollar, the traditional safe haven, sold off at a time of market stress. Instead of running towards the dollar, investors fled. As chart 4 shows, the trade-weighted dollar index fell to the lowest level in three years. It remains elevated relative to its longer-term history and potentially has further room to fall if the growth outlook sours and the Fed starts cutting rates. Moreover, given erratic US policymaking, international investors could continue to rebalance their portfolios away from the US after being massively overweight over the last decade. Note that this would be a cyclical move out of dollar assets. It is too soon to know whether the dollar’s structural role in global finance and commerce is under threat. For the time being, there is simply no credible alternative. But the fact that the question is being discussed is telling.

The rand, meanwhile, behaved exactly as one would expect during an episode of extreme global risk aversion. It fell from R18.32 at the start of April to R19.92, before regaining most of this lost ground. The rand typically sells off when global investors are jittery and then stabilises and strengthens. It just happened on a very compressed timescale, highlighting once again how difficult it is to time the currency.

Chart 4: US dollar index and rand-dollar exchange rate

Source: LSEG Datastream

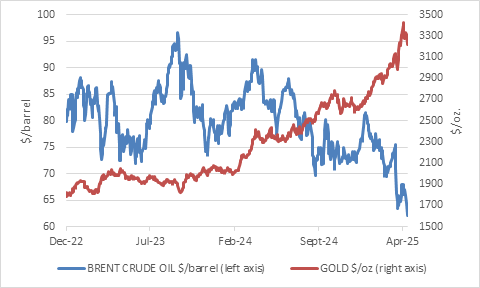

Finally, it is commodity markets that perhaps provides the clearest signal that all’s not well. Though the gold price is off its record highs, it is still 22% higher since the start of the year, while oil is 16% lower. The former points to elevated investor unease, while the latter suggests weaker economic growth ahead. However, it will also reduce inflationary pressures worldwide, and support the case for central bank rate cuts, including in South Africa, where inflation surprised to the downside yet again in March.

Chart 5: Gold and oil prices

Source: LSEG Datastream

Ceasefire

The big question is therefore whether additional Trump concessions will be forthcoming, and whether other countries, particularly China, can also come to the table and offer him something he can pass off as a win. Since trade agreements typically take years to finalise, and the White House must simultaneously negotiate with dozens of countries on a tight deadline, these deals will be best thought of as ceasefires, not peace treaties.

Importantly, these ceasefires must also come in time to avoid long-term damage. A firm that closes shop because it is unable to afford key inputs will not simply restart as soon as the cost of those inputs fall again. On the contrary, every business failure has knock-on effects that put other firms and their employees at risk.

Businesses are adaptable, but they need to know what they are adapting to. The longer they are left in limbo in terms of where tariffs are headed, the greater the odds of a recession in the US with negative implications for other economies and the equity market. It must be pointed out that, if it happens, this will be the first time in modern history that the US stumbles into a recession like this – essentially shot down by friendly fire. The Federal Reserve has caused policy-induced recessions before, notably in the early 1980s, but there was a clear goal in mind: to win the war on inflation. The contraction was deep, but once inflation was beaten, the economy came roaring back and markets enjoyed a long boom. The problem is that it seems very unlikely that Trump’s tariffs will be a similar case of short-term pain for long-term gain. Instead, he risks long-term damage with little upside.

Staying calm under fire

Meanwhile, investors in the trenches of global markets must maintain cool heads. As Barton Biggs wrote in his classic work, “Wealth, War and Wisdom” the low point in British stock markets during Word War II came soon after the debacle of the Dunkirk evacuation and the terror of the Blitz (the Luftwaffe bombing of British cities) in 1940. Hitler controlled most of the European continent, and D-Day and VE-Day were still far into the future, but markets didn’t need good news to stop falling, it just needed all the bad news to be priced in. From the middle of 1940 onwards, things could only get better for the Allies, and ditto for markets.

We don’t know what the next few months holds, and it is not clear that even Trump himself knows. There seems to be no game plan on his part; it is all tactics and no strategy. Investors are betting on ceasefire and might still be disappointed. But for now, let’s just remind ourselves that when markets get wild, riding out the volatility is usually a good strategy, as was the case over the last couple of weeks. Trying to time the highs and lows is for traders, not long-term investors.