A dynamic environment requires a flexible approach

Marc Beckenstrater, Fund Manager at PSG Asset Management

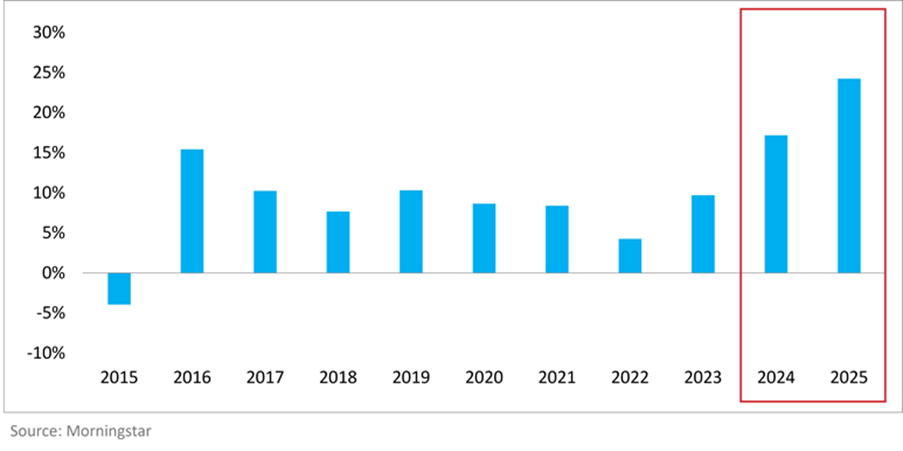

South African bond markets rewarded fixed income investors with exceptional calendar year returns in both 2024 and 2025 – the All Bond Index (ALBI) returned 17% and 24% respectively. These returns are far above the norm, and so we anticipated moderating performance in 2026, especially as the market had repriced strongly as risk perceptions around the local economy and political climate improved, the risk premium decreased and foreign investors started finding our bonds attractive again.

FTSE/JSE All Bond

Thus, we entered 2026 with the prospects for local nominal government bond returns looking respectable, if less attractive than over the previous two years.

It’s been a tough year for bonds so far

Global developments in 2026 so far have not been supportive of bonds. The conflict in Iran sent oil prices sharply higher, triggering inflation spikes.

Compounding the inflation picture, the United States (US) is confronting a structural fiscal challenge that markets are no longer willing to ignore. With the federal deficit running at levels historically associated with wartime or crisis, and the Treasury needing to roll over and issue new debt at scale, bond investors (the so-called bond vigilantes) have reasserted themselves as an effective constraint on fiscal and monetary excess. In the absence of a credible consolidation path, the market itself is doing the work that policymakers have deferred, demanding higher yields as the price of continued financing. Consequently, we have seen US long-term bond yields edge up, with US 30-year paper trading at yields in excess of 5%. In this sense, rising US long yields are not a temporary tantrum but a considered repricing of sovereign risk.

What is often underappreciated is that even a bond that ultimately repays in full can inflict meaningful mark-to-market losses in the interim, and in the current environment, where short-term inflation fears are flaring, investors are demanding additional compensation simply to bear that uncertainty. This inflation risk premium – compensation for bearing uncertainty about future inflation rather than inflation itself – has pushed up nominal yields while also representing a higher hurdle for real returns globally.

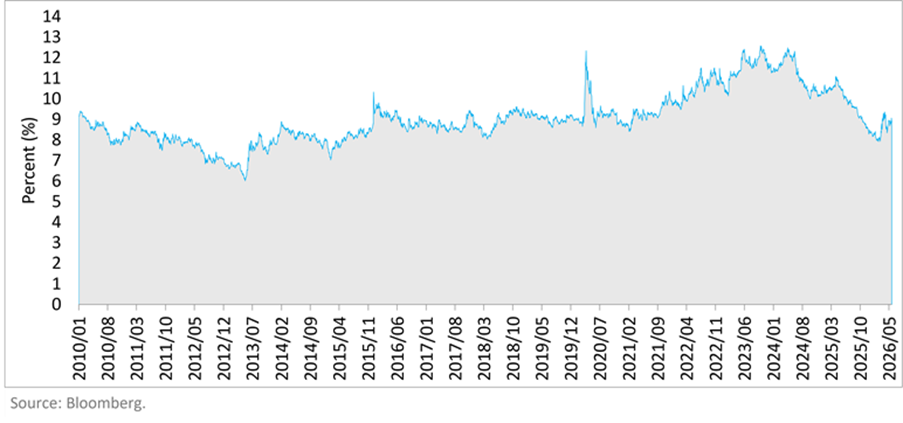

Against this backdrop, South African nominal government bonds have perhaps held up better than expected. Despite weakening appreciably since mid-April, current yields on the 10-year bond of around 8.6% (27 May 2026) are still appreciably lower than the levels of above 11% recorded at the height of uncertainty around Budget 3.0 and the Government of National Unity (GNU) in March/April 2025.

South Africa 10-year bond yield

Nonetheless, the recent experience again highlights that bonds are not risk free, and serves as a reminder that risk management in fixed income portfolios remains important.

What are fixed income investors to do against a changing global backdrop?

Inflation, the primary threat to real returns, can be an especially tricky opponent for investors with a lower risk tolerance. Retirees are a good example. They may have substantial investment timeframes ahead of them (often 30 years or more), but may be highly risk averse and unable to stomach any potential loss of capital. Nonetheless, preserving the purchasing power of their income is a key consideration, even as adding risk assets capable of outperforming inflation in the long run introduces more short-term volatility to portfolios.

As responsible stewards of our clients’ capital, we believe it is most important to be a safe pair of hands for our fixed income investors – not taking undue risk with their capital, while still providing as much yield as possible in a responsible and risk-conscious manner, suited to the objectives of the fund.

Twenty years of income excellence

To our minds, this approach is exemplified by the PSG Diversified Income Funds, which recently celebrated reaching its 20-year milestone. The fund mandate offers a broader investment toolkit, providing the fund manager with the flexibility to adjust fund positioning as market conditions change.

The fund invests in a mix of local and foreign assets across the full breadth of the fixed income spectrum. It looks to actively allocate to the areas of the fixed income market where there is a low likelihood of capital loss, and the market is providing attractive risk-adjusted returns to achieve the fund’s return objective of inflation +1% over rolling 2-year periods. The fund’s toolkit also encompasses limited investments in listed property, preference and ordinary shares, while tightly managing risk with the aim of preserving capital. This extra toolkit beyond narrow fixed income has allowed for enhanced portfolio construction. As price-sensitive investors, we not only aim to consistently invest at a margin of safety, but also to identify the opportunities where we believe the market has mispriced assets due to an undue focus on prevailing narratives or short-term factors.

How we have used a flexible toolkit to our clients’ advantage recently

Given the volatile investment environment, our focus has been on capital preservation, liquidity, and flexibility. We reduced interest rate risk early in the year by lowering portfolio duration, primarily through the sale of fixed-rate bonds. Following strong performance in medium-term inflation-linked bonds during January and February 2026, and a widening in breakeven inflation rates, we took profit in these instruments, recognising improved pricing and the potential for better re-entry opportunities. We increased exposure to floating-rate instruments, which are more resilient in an environment of rising or uncertain interest rates, and maintained a high level of portfolio liquidity. This positioning allows us to respond dynamically to evolving market conditions while limiting downside risk, and we believe it has offered an advantage to our investors as inflation risks have come to the fore, as highlighted by the graph and tables below.

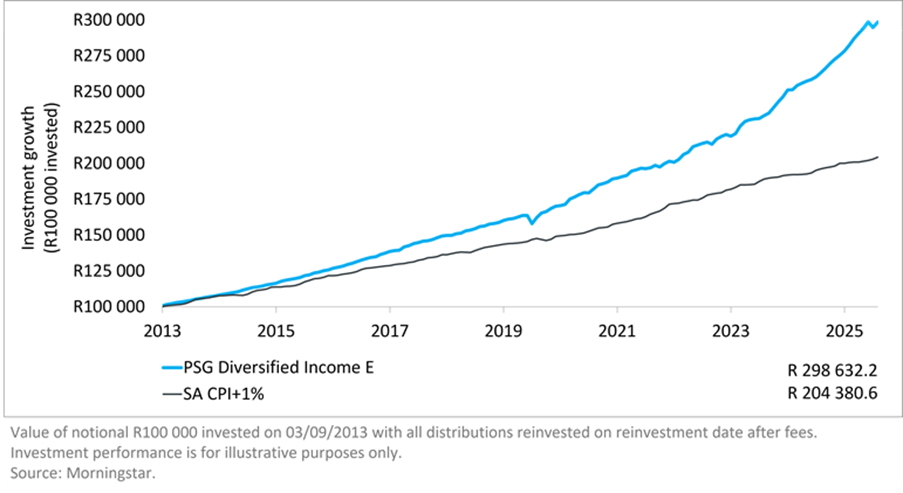

The A class was closed to new investments. The graph below highlights fund performance since the launch of the E class of the fund in 2013. This is the class of the fund that is currently open to new investments through platforms.

Cumulative long-term performance

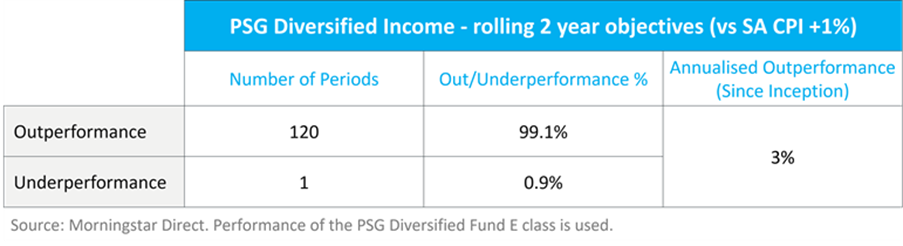

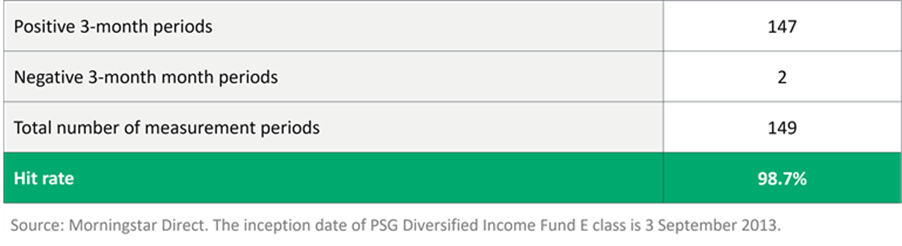

PSG Diversified Income Fund E: Number of positive 3-month rolling periods since inception

A fixed income process that considers both price and risk benefits our investors

Successfully navigating a changing fixed income environment not only requires being on the lookout for opportunities to responsibly enhance the yield on offer for investors, but – importantly – also avoiding a permanent loss of capital. We believe that to be truly successful in the long run, it is imperative that a fixed income process consider the price paid for an investment as well as carefully weighing the risks. A flexible mandate helps the PSG Diversified Income Fund adjust its approach as the market continues to evolve. We believe this flexibility offers important benefits to investors in a rapidly changing and unpredictable environment. Twenty years of navigating exactly these kinds of environments – from the Global Financial Crisis to the Covid-19 pandemic, to the current bout of fiscal and inflationary turbulence – gives us both the conviction in our process and the humility to know that preserving our clients’ capital requires constant vigilance, not complacency.