Between Hype and Fear

Izak Odendaal, Old Mutual Wealth Investment Strategist

Many European football fans visiting the US for the FIFA World Cup have been astounded by the size and sophistication of American stadiums. This includes the most expensive stadium ever built, the 70,000-seater SoFi Stadium in California. Named after its sponsor, a financial company, it could easily have been called the Sci-fi Stadium as it resembles a giant spaceship. The cost was also out of this world, coming in at $5.5 billion.

However, this pales in comparison to the cost of a typical artificial intelligence (AI) datacentre, which can be between $10 to $40 billion depending on the size. Although there are only a dozen or so stadiums in the US with a price tag of more than $1 billion, hundreds of datacentres are under construction with more than a thousand in the planning stage. McKinsey estimates that global spending on datacentres could reach a cumulative $7 trillion by 2030. Just as the FIFA World Cup draws fans from around the world, these datacentres rely on imported components, spreading the economic gains to many countries. Indeed, semiconductors account for 50% of a datacentre’s cost and are mainly sourced from Taiwan and Korea. Unlike the World Cup, this build-out is not ending any time soon.

The International Monetary Fund’s latest outlook is titled “Global Economy in Crosscurrents of War and Technology.” It doesn’t exactly roll off the tongue but still summarises the situation. On the one hand, there is the extraordinary, fixed investment boom as companies compete to get ahead in the AI race. On the other hand, the world economy faces not only the impact of the Gulf War, but in fact a series of geopolitical shocks, including the still-raging war in Ukraine and the 2025 US tariff shock.

A turn for the worse

In terms of the war, things took a turn for the worse last week. Iran fired on ships trying to cross through the Strait of Hormuz. The US retaliated by launching missile strikes on several sites in Iran. President Trump said that the ceasefire was “over” as far he was concerned, and the oil price predictably jumped about 5%.

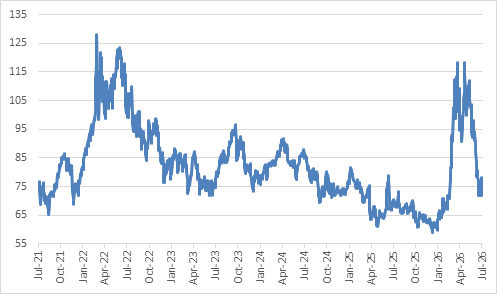

Chart 1: Brent crude oil price, $ per barrel

Source: LSEG Datastream

Since there is no trust between Iran and the US, the peace process was always going to be bumpy. However, both sides have a strong incentive to put the conflict behind them. America holds midterm elections in November, and this war and associated fuel price increases are unpopular with voters. As for Iran, it achieved a strategic victory against a much more powerful opponent simply by holding out. However, its fragile economy means it doesn’t have infinite capacity to absorb a US military and financial assault. At $76 per barrel, Friday’s closing price, it is clear that market believes that the peace process will continue.

At its worst, the oil price spiked to $120 per barrel, but never came close to the doomsday-scenario of $200 per barrel. While most people fixated on the loss of supply, there was enough demand flexibility to avoid things spiralling out of control, while there were also ample stockpiles to draw from, notably in China. If the conflict escalates further, investors will keep a nervous eye on those inventory levels.

Nonetheless, there was a negative economic impact. An oil price spike transfers income from buyers to producers, but the latter does not spend as much as the former. Therefore, total global spending on non-oil goods and services declined. Inflation rates also increased, though not nearly as much as was the case after the Russian invasion of Ukraine, since that episode was associated with a surge of pent-up demand as the world exited Covid lockdowns

In response to higher inflation, and particularly the concern that consumers and businesses will start believing that inflation will be permanently higher, several central banks raised interest rates. This includes the South African Reserve Bank. Long-term market-based rates (bond yields) also increased in countries such as the US and UK where central banks have so far remained on hold.

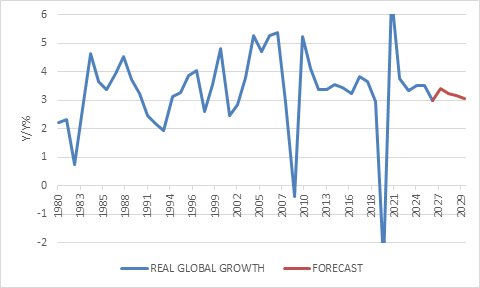

Chart 2: Global economic growth

Source: International Monetary Fund

All in all, the International Monetary Fund therefore expects that global growth will fall to 3% this year, which is slightly below the long-term average, before recovering next year to 3.4%. In its forecast, the headwinds from higher energy prices will be largely offset by the AI capex boom.

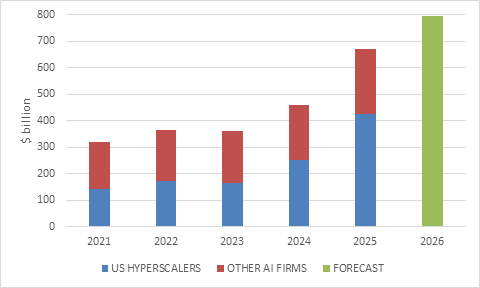

Chart 3: The AI capex boom

Source: Bank for International Settlements

With this boom comes the risk of overinvestment. Demand for AI is high as more businesses integrate it into their processes, and consumers use it daily. The providers of these services (the ones building the datacentres) are reporting strong revenue growth. However, there is still substantial uncertainty over how much individuals and firms will ultimately be prepared to pay for these services, who will capture that spending and whether there will be enough profit tomorrow to justify today’s capex.

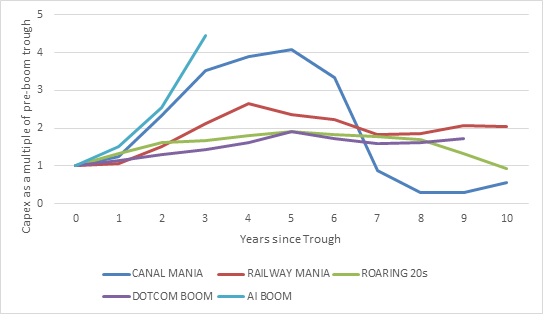

If history is any guide, at least some players will get overexcited, and build for demand that never materialises. This always happens when an exciting new technology comes along. Chart 4 from the recent annual report of the Bank for International Settlements (BIS) shows that the AI capex cycle is already running ahead of historical analogies. The BIS argues that the 1830s UK canal boom, followed by the railway mania, mass electrification (the “Roaring 20s”), and the internet boom of the late 1990s shared a common trait: “a genuine technological breakthrough that attracted capital in excess of what commercial returns could ultimately justify. These episodes ended with an eventual reversal in investment, inducing economy-wide recessions.”

Chart 4: Historic capex booms

Source: Bank for International Settlements

In other words, if AI fails to meet increasingly inflated expectations, there could be large financial losses, with spillovers to the real economy. However, there is also a scenario where AI fully lives up to its promise and leads to massive job losses with extreme political, social and economic consequences. This is a topic for the future.

For now, the main thing to watch is debt. Leverage is what turns financial corrections into economic recessions. Companies and households can absorb declining values in assets they own outright (where they have equity) but if that asset was financed with borrowed money, there is a problem. They are still on the hook for interest payments. Moreover, since one entity’s debt is another’s asset, these problems can cascade through the economy. As we saw in 2008, the impact is even worse if the debt is sliced and diced and spread throughout the financial system, making it difficult to determine who owns (and owes) what.

Current debt levels are still manageable, but they are rising. Even the so-called hyperscalers, the likes of Meta, Microsoft, Amazon and Alphabet, can no longer fund datacentre capex from their own cashflows. They are starting to issue shares to raise capital, after a decade of buybacks, but also turning to borrowing.

The Bank of England’s latest financial stability report, released last week, noted that “AI-related companies’ use of credit markets has accelerated rapidly, including in public markets, private credit, leveraged and structured finance, and is set to increase further as financing continues to expand.” It notes that the hyperscalers borrowed more in the first half of the year than the whole of last year, around $170 billion. This number is still small compared to the size of total global corporate borrowing. Overall corporate bond issuance reached $13.7 trillion in 2025 according to the OECD. AI-related borrowing has been easily absorbed so far in public and private credit markets. It is the projected increase that raises eyebrows, however, as well as frequent use of opaque off-balance funding arrangements. There doesn’t appear to be immediate danger, but the vulnerabilities are likely to keep building the longer the boom continues.

Profitability and productivity

The IMF argues that this boom can go in one of two directions. On the one hand, it could lead to broad-based AI adoption and efficiency gains. This will lift medium-term global growth rates, though as chart 2 shows, it is not incorporated in the IMF’s central forecast. On the other hand, if profitability and productivity gains disappoint, investment spending could “retrench abruptly”, while “frothy” equity valuations would decline.

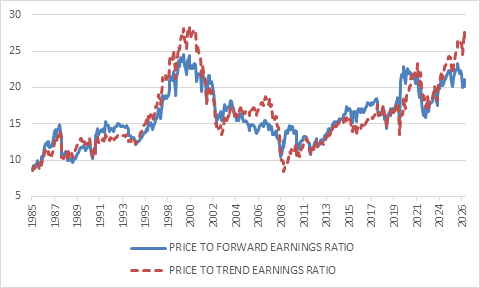

How frothy? As chart 3 shows, the S&P 500 trades on a lofty 20 price: earnings ratio (solid line). This is in the 81st percentile of monthly values since 1985, meaning it has only been more expensive 19% of the time. The picture is even worse when adjusting for the fact that earnings growth has been unusually strong due to all the AI-related capex. The price to trend earnings ratio (dotted line) is in the 97th percentile. Valuations at these levels have historically led to disappointing longer-term returns since so much good news is priced in.

Chart 5: S&P 500 price: earnings ratios

Source: LSEG Datastream

This is not an argument to cut and run. Peter Lynch was right when he famously said, “More money has been lost by investors preparing for corrections, or trying to anticipate corrections, than has been lost in corrections themselves.” It is nearly impossible to time market peaks, and since we’re only in the early stages of the AI revolution, there is a risk to missing out. However, exposure needs to be appropriately scaled within the context of a diversified portfolio. Alongside Lynch’s quote, we should acknowledge the equally famous comment from Warren Buffet who said the best time to be greedy (increase equity allocations) is when others are fearful, while we should be fearful (cautious in equity allocations) when others appear to be greedy, and caught up in the hype.

In other words, geopolitical shocks have been frequent and will likely reoccur as we move from a unipolar (US-dominated) world order to a more multipolar one, while domestic politics increasingly tilts towards populism. The Iran war is a symptom of this, but one with a direct economic impact from the higher oil price. While the conflict is by no means over, and the oil price increase has caused many problems, it has not been catastrophic. The oil price is bound to remain volatile, but if it hovers between $75 and $90 per barrel, the world as well as the South African economy can cope.

When bombs are flying, it is natural for investors to become anxious, but things aren’t always as bad as they seem (mainly because we are far away from the death, destruction and real suffering). Geopolitical events like these often offer buying opportunities when others sell in panic. But while the dangers of war are obvious to everyone, it is the hidden risks in the financial system that typically cause the most damage for investors. Global markets are becoming increasingly concentrated, with AI the common underlying theme. This makes diversification harder but not impossible. For example, the Bank of England report notes that AI-related companies now make up 50% of market capitalisation of US markets, but only low single digits for the UK market. The same is true for the JSE. Both these markets also trade on reasonable valuations, while local fixed income also offers attractive real yields. When geopolitical uncertainty causes angst and technology leads to hype, keeping a cool head is more important than ever