Bitcoin’s Black Friday

Izak Odendaal, Old Mutual Wealth Investment Strategist

It was expected to be a strong year for Bitcoin and the broader crypto world. Donald Trump’s second presidency is considered the most crypto-friendly in US administration history, with the Trump family heavily involved in crypto schemes. Bitcoin duly rallied from $68,000 on the eve of last year’s election to a record of $121,000 at the beginning of October. Since then, it has slumped, closing last week at $91,000.

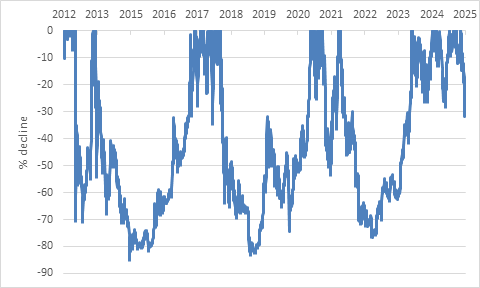

Will this have broader implications, and does it reveal anything meaningful about the overall state of markets? Not really. As chart 1 shows, Bitcoin has endured at least seven peak-to-through declines of more than 20% since 2012, and three proper crashes when it lost more than 70%. Bitcoin’s price could well rebound as it has done before — simply because enough people believe it has value. Or more precisely, enough people think other people will believe it is valuable. To be fair to them, the price is up an incredible 23,000% over ten years even after the 28% decline from its recent high. Each time it bounced back, rewarding those investors with patience and nerves of steel. However, unlike bonds or equities, there is no income stream, dividends or interest to reward investors while they wait for the price to recover.

Chart 1: Bitcoin maximum drawdown

Source: LSEG Datastream

Digital gold?

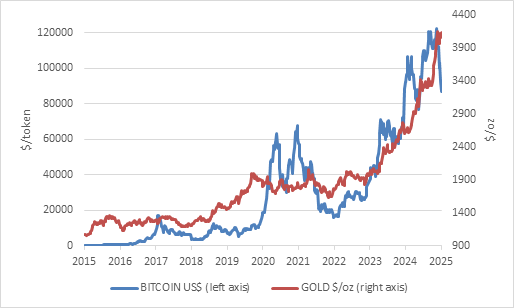

Gold also generates no income, and indeed many investors view Bitcoin as “digital gold” since its supply is fixed at 21 million, unlike currencies, bonds or equities. (However, there is no limit to how many competing coins can be created.) Many die-hard Bitcoin holders, similar to gold advocates, share the belief that currency debasement and runaway inflation are inevitable as government debt levels rise.

Chart 2: Gold and Bitcoin prices in dollars

Source: LSEG Datastream

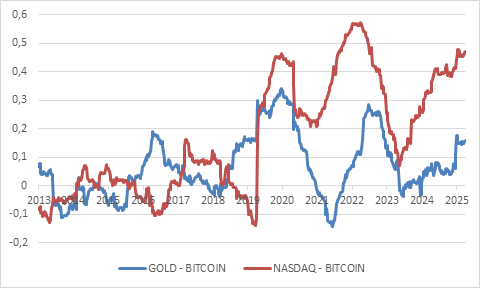

It is therefore notable that Bitcoin and gold diverged this year. However, correlations between Bitcoin and other investments show that it behaves as a “risk on” asset, rather than a safe haven. Bitcoin is more correlated with equities, particularly tech shares (as typified by the Nasdaq) than with gold, particularly after 2020.

The sharp decline in Bitcoin over the past month may therefore simply be an exaggerated move in response to the wobbles in tech shares, as investors start getting nervous about the massive spending on artificial intelligence. Or perhaps, given that a lot of the enthusiasm for Bitcoin at the start of the year was political, the declines mirror Trump’s falling approval rating. There is also the special case of “Bitcoin treasury companies” whose leveraged Bitcoin purchases helped boost it on the way up but similarly accelerated losses on the way down.

Chart 3: Rolling 12-month correlations of daily returns

Source: LSEG Datastream

Regardless of what drove the recent slide, the fact that Bitcoin’s wild swings have caused minimal problems to the broader financial system is indicative of its narrow adoption. If the dollar, rand, pound or yen fell almost 30% in a two-month period, there would be serious real-world implications. Despite the hype, Bitcoin is no closer to its original intention of being a currency that operates as a serious alternative to government-backed (fiat) currencies and a way of disintermediation of the traditional financial system. It is used extensively in black market activities, but not much beyond that for good reasons. Apart from the fact that transactions can be slow, using Bitcoin to make purchases will also count as a disposal event, potentially triggering capital gains tax in some jurisdictions. (South Africa is one of those, and SARS won’t let you get away with not declaring Bitcoin gains).

The main reason it cannot be a currency, however, is the volatility. You might have planned to use your Bitcoins for some Black Friday shopping, but you now have almost 30% less to spend compared to a few weeks ago. Rapid price increases also discourage use as a currency. Nobody wants to be Laszlo Hanyecz, who famously spent 10,000 Bitcoins on two large pizzas in 2010. At the time, that amounted to about $40, but today it would be almost one billion dollars. If people believed that the price of Bitcoin would go up over time, they would tend to postpone spending as much as possible. It would be deflationary for the economy.

To be useful as money, it must be relatively stable in value. While cash loses value over time due to inflation, the loss of purchasing power — around 4% to 5% per year in South Africa or 2% to 3% a year in Europe and America — is gradual enough that people don’t feel they must spend their money immediately (the annual loss of purchasing power compounds over time, therefore cash is not a good long-term investment.) It doesn’t make sense to buy Bitcoin expecting that it will rise in value because it will one day be widely used in everyday life. It is either one or the other.

In search of stability

Stablecoins are different. As the name suggests, stablecoins typically run on a blockchain ledger like Bitcoin, but maintain a fixed value relative to the dollar or another currency. They were designed to be the bridge between the crypto world and traditional finance and that remains their primary role today. It is widely assumed that they can go further and become prominent in day-to-day transactions, not just in countries with underdeveloped financial systems, but also in advanced countries.

The big benefit of stablecoins is immediate settlement, an instant transfer of economic value when a transaction takes place since everything happens on the same ledger. It is like paying with a banknote, where ownership instantly changes hands. In contrast, when you pay for something with your credit card, it feels instantaneous to the buyer but the process of clearing and settling the transaction in the background can take a day or two. Cross-border payments are even more laborious, with several middlemen.

Most stablecoins are pegged to the US dollar and therefore basically digital dollars. However, the are privately issued and lack the backing of the US government, and some stablecoins have broken their peg in the past. The Federal Reserve has an obligation to ensure that each dollar is worth the same as every other dollar (a property known as “singleness”), but stablecoins can be worth more or less than other dollars. This is in part because they are backed by holdings of securities whose market value can fluctuate. Some are even backed by holdings of other cryptocurrencies, the most famous example being TerraUSD, which crashed in 2022, wiping out $45 billion.

S&P Global Ratings last week downgraded the stability rating of Tether's USDT, the world’s largest stablecoin, to its lowest possible level. This is because USDT is backed by a mix of assets that include Bitcoin.

The US GENIUS Act is meant to fix this, and its adoption in July was greeting with great enthusiasm in the crypto community. It allows banks and other companies to issue stablecoins which must be backed one-to-one by safe reserves such as cash or short-term US Treasuries. This is a step in the right direction but still leaves the possibility that the peg could come under pressure since even short-term Treasuries can fluctuate in value. Stablecoin issuers always have an incentive to hold the highest yielding assets possible because they keep the interest. This means there might be volatility in the reserves that could ultimately undermine confidence in the coin itself. There is also a transition period until 2027 for stablecoins to comply if they want to operate in the US. This leaves open a window of vulnerability. Holders of coins outside the US could still end up with risks they don’t fully appreciate.

Oh, the irony

Ironically, stablecoins could ultimately help to prop up the US dollar and the value of US government bonds. The more dollar-based stablecoins grow in popularity, the more dollar assets they will purchase to hold as reserves. They are already significant holders of US government bonds. Indeed, this seems to be part of the motivation for the GENIUS Act and accompanying legislation that bans the Federal Reserve from issuing its own retail central bank digital currency (CBDC). A Fed CBDC would not need government bonds as backing, in the same way that Fed-issued dollars are not explicitly backed.

Outside the US, especially in Europe, this prospect has alarmed policymakers. Apart from the financial stability concerns, the more dollar-based stablecoins are adopted, the more it cements the dominance of the dollar at the expense of the euro and other currencies.

While stablecoins offer significant promise — particularly in terms of speeding up transactions, especially across borders, and broadening financial inclusion — the lessons learned over decades of banking runs and financial crises should not be forgotten in the rush to embrace this new shiny toy. Users should be comfortable with what sits behind the coins. There are also other ways of expanding access to finance and introducing real-time payments that do not rely on blockchains, such as Brazil’s PIX platform and India’s United Payments Interface. Both are very successful and have been closely studied by the South African Reserve Bank to eventually emulate.

In conclusion

Many crypto enthusiasts will point to stablecoin adoption or tokenisation (another area of promise which we don’t have space to discuss here) as proof that “crypto is going mainstream”. This really has little to do with Bitcoin.

For financial advisers, trustees, and investors in general, the combination of hype, novelty, security risks and volatility makes crypto a minefield to navigate. The fact that Regulation 28 of the Pension Fund Act prohibits crypto and “digital assets” in retirement vehicles simplifies the issue somewhat. Nonetheless, many people are still looking at their discretionary portfolios and asking whether they need crypto exposure, and how much.

As with any investment, the starting point should always be the goal of the investor, their overall financial position, liquidity needs, tax position and tolerance for risk. Every asset class plays a role in a portfolio to meet the investor’s goal: cash brings stability and liquidity, equities bring growth, bonds provide income, etc. What role should Bitcoin fulfil in a typical portfolio? Given its volatile and speculative nature, that role is likely to be small.