Cooperation, Competition and Conflict

Izak Odendaal, Old Mutual Wealth Investment Strategist

The first formal treaty between the United States and China was signed in 1844 in rather unseemly circumstances. After Britain won significant concessions from the Qing Empire in the First Opium War, America also wanted similar favourable terms. This led to the Treaty of Wangxia, signed between a rising power, the US, and a collapsing one. It confirmed US access to the five treaty ports (Guangzhou, Xiamen, Fuzhou, Ningbo, and Shanghai) where Westerners enjoyed special rights, including, to the chagrin of Chinese, extraterritoriality, meaning that Westerners accused of crimes could not be tried by Chinese authorities. It kicked off a period known in China as the “Century of Humiliation”, including another Opium War, Japanese invasion, civil war, and in 1949, the communist revolution.

Cordial

In contrast, last week’s meeting between Presidents Donald Trump and Xi Jinping in Beijing occurred against a much more cordial backdrop, resulting in statements of friendship and cooperation. Considerable underlying tensions remain, however. Today, China is the resurgent power, challenging the role of the US as sole global superpower. China maintains close ties with Russia, putting it at odds with Western support for Ukraine, while it is also Iran’s biggest customer. Taiwan remains a major sticking point, with China strongly insisting on an eventual reunification while the US supports the status quo. Taiwan’s current role as the world’s leading producer of high-end semiconductors puts it at the centre of the artificial intelligence (AI) boom, making the situation particularly delicate.

The US has been trying to protect its lead in artificial intelligence and other technologies by preventing China’s access to the top-of-the-range chips. On the other hand, China leads in many of the technologies related to the green transition and is by far the biggest producer of solar panels, batteries, wind turbines and electric vehicles. It is basically the Saudi Arabia of clean energy, and since AI is so electricity-intensive, this might ultimately give it an advantage. China also produces 80% to 90% of total global supply of several “rare earth” minerals, critical inputs to a wide range of key military and industrial technologies. This gives it significant bargaining power in its dealings with any country, including the US.

The world’s factory

In fact, China is by far the biggest producer of many goods the world needs and wants, both basic and high-tech. As a result, its trade surplus (exports minus imports) is the biggest of any country, ever, coming in at over $1 trillion last year. There is an uncomfortable echo here. The Opium Wars forced China to accept imports of the drug from Britain and other colonial powers because then as now China had a trade surplus. The Western world wanted Chinese products, but the feeling wasn’t mutual, so gold and silver flowed east in remarkable quantities. Forcing China at the point of a gun to import opium, with devasting social consequences, was a means to balance the lobsided trade relationship.

Trump imposed tariffs on China in his first term to improve the modern trade imbalance, and his successor, Joe Biden, kept most of those in place. Hawkishness on China has become a rare bipartisan topic in Washington. In his second term, Trump went even further, and at one point the tariff on Chinese goods was 145%. After talks, carve-outs and ultimately, the Supreme Court’s intervention, the effective tariff on Chinese imports is closer to 25%, still considerably higher than in the past.

As a result, Chinese exports to the US have declined sharply. At its peak in 2017, almost a quarter of US goods imports by value came from China. By April of this year, it was only 8%, though there is likely to be a fair amount of rerouting through third countries like Vietnam.

While the rest of the world has largely not followed Trump in raising trade barriers on China, that doesn’t mean they don’t want to. Industries across Asia, Europe, and elsewhere are facing intense pressure from Chinese imports. The motor industry is taking particular strain as China transformed from a car importer to the biggest exporter by volume in the past few years.

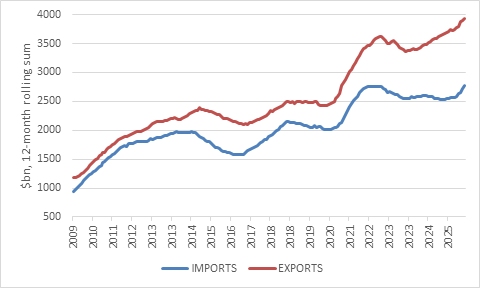

Chart 1: China’s exports and imports by value

Source: LSEG Datastream

This export strength is impressive, and the relative decline in imports partly reflects a switch to homegrown brands. However, the trade surplus nonetheless hides a weakness, namely a lack of domestic demand. This is partly a deliberate choice. As is well known and often discussed, China’s economic model has structurally favoured investment over consumption, with households taking home a smaller share of national income than countries at a similar stage of development. Meanwhile, resources were poured into building world-class infrastructure and manufacturing capabilities. However, a sizeable share of the investment spending was also channelled into residential real estate, leading to an epic bubble that burst in 2022.

The collapse of the property bubble continues to reverberate throughout the economy. Fewer apartments being sold also implies fewer fridges, televisions and beds, a portion of which would have been imported. If imports had broadly kept pace with exports, Chinese consumers would be the owners of an additional $100 to $200 billion in goods from overseas. Instead, consumer confidence is battered by historic standards, though somewhat better compared to a year ago.

Chart 2: Chinese consumer confidence

Source: LSEG Datastream

Yuan too few

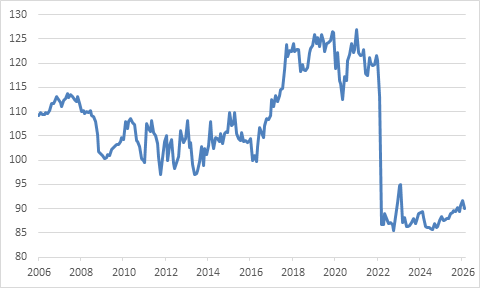

Another reason behind the import weakness – and export strength – is an undervalued currency, also a longstanding bugbear of the US government. A country with such a large trade surplus would ordinarily see upward pressure on its currency. Even after appreciating somewhat in recent years, the yuan remains generally weak on a real trade-weighted basis.

Chart 3: China real trade- weighted exchange rate

Source: OECD

A weak currency typically stimulates exports and constrains imports, a reason why Trump is keen on a softer dollar and a stronger yuan. It would help balance the trade relationship between China and the rest of the world and raise the purchasing power of Chinese households, who would be able to afford more foreign goods and services and overseas holidays.

The yuan exchange rate is managed by the People’s Bank of China (PBOC), and therefore its level is a choice, not a fait accompli. It makes sense that the yuan would be allowed to rise over time, though probably very gradually as the PBOC tends to pursue stability above all else. A stronger currency will assist Beijing in its desire to position the yuan as an alternative to the dollar, since one of the best ways to get foreigners to hold yuan would be if they think that it – and by implication other Chinese assets – will rise in value over time. Global use of the yuan is still small, and far out of proportion with China’s share of international trade. This will require a relaxation of capital controls, however.

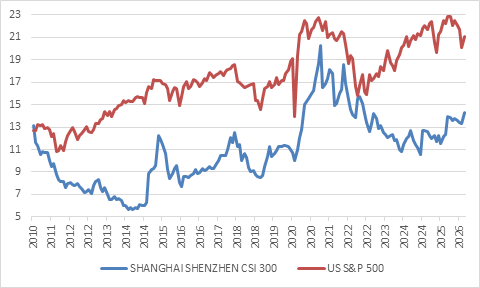

This brings us to a final comparison between the US and China, namely equity markets. As much as China can confidently project itself on the global stage as an economic, military and technological superpower, market valuations tell a different story. Conversely, any talk of US decline under Trump’s mercurial leadership is also contradicted by the S&P 500, which has marched to new record levels even as the war in Iran remains unresolved and the Strait of Hormuz closed.

Chart 4: Forward Price: Earnings Ratios

Source: LSEG Datastream

Chinese equities trade at a large discount to the US, more so if one considers that the 10-year US government bond yield closed just shy of 4.5% last week, while the Chinese equivalent was only 1.7%. This implies a substantial ‘equity risk premium’ in Chinese equities, while US equities carry little margin of safety.

Some of this reflects the unpredictable regulatory changes that earned China the “uninvestable” label around 2021. Since then, however, authorities have shifted their attitudes towards Chinese equity markets. Beijing long views equity markets as a sideshow that attracts speculation, whereas the serious business of funding economic development fell on the banking system. However, banks are now constrained by struggling property exposure, while the example of other countries, notably the US tech sector, has shown how equity markets can fund innovation and growing companies. They also act as an engine of wealth creation for households, important in a country with an ageing population and patchy social security coverage. Therefore, regulators are now keen to foster a “slow bull market” of gradually rising equity values that can support economic development and help Chinese families save for retirement. To support this, corporate governance standards have been raised, and listed companies are encouraged to pay regular dividends. This is a long-overdue shift to a more shareholder-friendly environment. Despite China’s phenomenal economic performance, listed companies failed to turn GDP growth into profit growth and equity returns have been lacklustre. In contrast, the main reason the S&P 500 trades at a premium is probably the consistent earnings per share growth delivery, well ahead of any other major market. Further weighing on the profitability of China’s industrial companies has been overcapacity and cutthroat competition, something policymakers are also trying to address through “anti-involution” campaigns.

For equity investors outside China, the trifecta of a cheap currency, low valuations and increased policy support should be appealing. China’s weight in the main global equity benchmarks compiled by the likes of the MSCI and FTSE Russell has declined to only around 3%, out of proportion with its share of total global economic output and innovation.

There are risks too. The country’s poor demographic profile is well-known, largely a function of the now-abandoned one-child policy. Only 7.9 million babies were born last year, the lowest number since the Communist Party took over in 1949. Life expectancy has increased considerably over time and now exceeds the US – a major achievement – which slows the population decline. However, the workforce is shrinking nonetheless, and this will weigh on long-term GDP growth rates (again, what matters for equity investors is not GDP but profits). However, it will also spur innovation and technological adoption. China was responsible for half of the world’s installation of industrial robots in 2024, according to the International Federation of Robotics, and for the first time, the majority of those robots were supplied by local firms. China’s approach to artificial intelligence also seems to be aimed towards practical applications rather than trying to build the most cutting-edge models, as is the case in Silicon Valley where winner-takes-all is the mantra. Time will tell which approach works better.

Chart 5: Total debt-to-GDP ratios

Source: Bank for International Settlements

A second risk is high total (i.e. combined household, government, corporate and financial sector) debt levels, which exceed the US when expressed as a share of GDP. Of note is how quickly it increased, clearly an unsustainable pace. China has a much higher savings rate than the US or any large economy for that matter, and most of the debt is domestic. Therefore, the problem is an internal distributional issue rather than an existential problem. Nonetheless, in a slowing economy, servicing all this debt becomes difficult and someone will have to absorb the associated losses.

Perhaps the biggest risk is the relationship with the US. Both sides are trying to reduce reliance on the other, and on this score, China might be ahead somewhat. However, both economies remain deeply intertwined and the idea of a complete decoupling is fanciful. Therefore, a sharp rupture over Taiwan or another flashpoint could result in a deep market sell-off, not just inside China, but across the world. If the US was to implement sanctions on China, any financial institution would have to comply or risk being cut off from the dollar system. The US retains significant leverage in this respect, something China knows very well.

No one would win from such a conflict, and therefore last week’s summit between Trump and Xi was important even if there were no major policy developments or breakthrough agreements on sticky issues. Smiles and handshakes don’t solve deep-seated disagreements but means that communication channels remain open. Strategic rivalry between the world’s superpowers is inevitable but can be managed. Both sides, and the world, can only lose if this rivalry turns to outright conflict.