Fragility and resilience

Izak Odendaal, Old Mutual Wealth Investment Strategist

The announcement of a brittle two-week ceasefire between the US and Iran last week brought relief, but fresh uncertainty emerged after direct talks collapsed and US President Trump announced a naval blockade. Energy prices remain elevated, hitting poorer countries hardest. The Gulf War triggered the fifth major worldwide crisis in a mere six years, following Covid-19, the post-pandemic supply chain chaos, the Russian invasion of Ukraine and the subsequent surge in food and energy prices, and last year’s US tariff shock. The optimistic view of these crises would be that the global economy demonstrated remarkable resilience, bouncing back each time and generally outperforming gloomy forecasts. This is partly due to policy interventions cushioning each shock, but also because of increased flexibility and adaptability, supported by technology. An obvious example is how seamlessly millions of people could switch to working from home in 2020. It is worth bearing this inherent resilience in mind when worrying about the current crisis.

Nonetheless, these five episodes highlight underlying fragilities in the global economy, areas of weaknesses that, whether through accident or by design, can cause widespread economic disruption. Some of these vulnerabilities are a by-product of globalisation and the creation of very complex supply chains. These were highlighted in the immediate post-pandemic period, but also last year, when Trump significantly increased US import tariffs. In his mind, tariffs help American producers, but the reality is that they, like manufacturers everywhere, rely on imported inputs. Making those inputs more expensive is counterproductive.

Others are deliberate. China made a strategic decision years ago to control most of the world’s processing capacity of rare earth minerals, essential in military and industrial applications. When China threatened to block exports of these minerals last year in response to US tariffs, Trump backed down. China has followed a similar approach to Japan in the past and could weaponize rare earths against other countries too.

In turn, the US controls a major lever of its own, the dollar. One of the most effective ways of targeting a country is to cut it out of the global dollar system. The mere threat of doing so is enough to stop any bank anywhere from doing business with a targeted entity. No major financial institution can survive without access to dollars, because the world still runs on dollars. It is to global commerce what oil is to internal combustion engines.

The link is not accidental. The fact that oil is priced in dollars is a big support for global dollar use. Indeed, the recent strength of the dollar against other currencies is precisely because each barrel now costs $40 to $50 more than three months ago, and buyers outside the US must now purchase more greenbacks to buy oil.

Chart 1: Trade-weighted US dollar index

Source: LSEG Datastream

In turn, the oil sellers, especially in the Middle East, have tended to recycle those dollars in the US financial system since they earn too much to spend at home. This “petrodollar” system is unlikely to unravel quickly but the war could add impetus to its fraying. Most Gulf oil and gas heads towards Asia, not the US. Switching to other currencies, notably the Chinese yuan, could be beneficial in some cases. However, this comes with the drawback that the yuan is not fully convertible and that Chinese interest rates are currently much lower than in the US.

Gulf oil producers will now have to spend more at home, repairing war damage and shoring up defensive capabilities. This will probably limit the amount they invest in the US, suggesting that the glacial process of “de-dollarisation” will be accelerated. This does not mean the dollar is dethroned, given its structural advantages, but that it loses ground on the margin. Since the dollar is still very strong in historical terms, it has room to decline in value in foreign exchange markets over time.

Revenge of geography

The other chokepoints in the global economy are down to geography and physics. Technology means we are not the prisoners of geography we once were. We can fly over mountains and communicate via satellites and shoot missiles at our enemies from great distances. But even today, it can be prohibitively expensive to move bulky objects over land. Despite oil hitting triple digits, trucking it out of the Middle East has not been seriously considered.

While there are a few important pipelines, most of the region’s oil and gas is shipped out through the Straits of Hormuz, since transporting anything on water is cheaper. It is Iran’s location that allows it to choke maritime traffic on this key channel, now and into the future. One possible outcome would be that it charges tolls on passing ships, which would not have a significant impact on the world economy, but would be a strategic defeat for the US since the Strait was toll-free before the war. Geography also means that despite America’s overwhelming advantage in conventional firepower, Iran could hold on. The advantage is asymmetric: the US would have to move thousands of troops over vast distances to occupy enough land to ensure the Strait stays open, just as the brutal Gulf summer months loom. Iranian militias only need to shoot a few rockets from mountain outposts to keep it closed.

Other maritime channels like the Bosphorus, Malacca and the Red Sea are also potential chokepoints, and a source of geopolitical leverage. Other nations could now follow Iran’s example. Indeed, Ukraine has recently targeted Russia’s Baltic oil terminals.

South Africa is also adjacent to one of the most important East-West global transit routes. It cannot impede the increased traffic around the Cape of Good Hope but can benefit by providing services to passing ships. South Africa is, however, also a victim of geography. Most of the world’s great industrial centres are next to oceans, lakes or large rivers. South Africa is a rare exception with its industrial heartland, Gauteng, built on top of rich gold reefs, not near a navigable body of water. Goods must be moved hundreds of kilometres overland, meaning that transport costs are structurally higher compared to other countries. To overcome this requires a top-notch network of road and rail. The national highways are in decent shape, but regional roads are not, and the railway system underperforms its nameplate capacity after years of underinvestment and mismanagement. Reforms are underway to improve rail and port capacity through private sector investment.

Revenge of the kilojoule

It is often said that economic activity is simply the transformation of energy. Even in our hyper technological world, the basic physical reality of energy cannot be ignored. Indeed, none of this technology is possible without energy, and artificial intelligence is particularly electricity thirsty. The availability of reliable electricity is emerging as a major bottleneck in the expansion of AI datacentres (but also remember that the biggest producer of key chips, Taiwan, is also a geopolitical flashpoint).

The reason the Middle East matters so much to the global economy is because it is the source of around a quarter of global oil supplies. Wars in other parts of the world simply do not get the same attention. It is not a coincidence that many oil-producing regions are volatile, and the world’s reliance on oil means that instability in these places has implications well beyond their borders. Oil drove geopolitics for much of the post-war era, arguably starting in 1953 with a US and UK sponsored coup in Iran after it nationalised Western oil assets.

Thanks to the shale revolution the US is now the world’s largest oil producer. Many international relations commentators thought that this will allow it to extricate itself from the Middle East. That day might come, but clearly not yet. Being an energy superpower has not yet dampened US adventurism abroad, as attacks on Venezuela and Iran suggest.

The Trump administration has doubled down on fossil fuel dependence, under the “drill, baby, drill” mantra. That is all well and good, given the vast reserves of the US, but it does mean that Trump is locking the US economy into a 20th century technology. The White House has actively tried to block, discourage and defund renewable energy production.

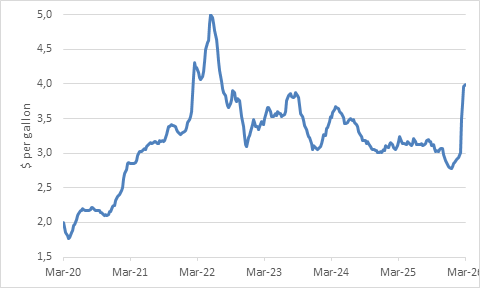

US oil producers obviously benefit from higher prices, but a motorist from North Carolina or Wisconsin paying $4 per gallon for gasoline has the same number of votes as a Texas oil billionaire. At this rate, the November mid-term election risks being a referendum on fuel prices, and the outlook for the Republican Party is not good.

Chart 2: US retail gasoline price

Source: LSEG Datastream

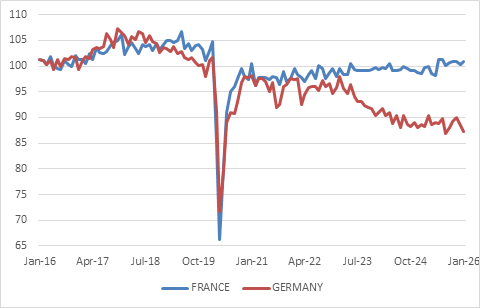

Of the large economies, Europe is particularly exposed in the current crisis, as it imports oil for transport and gas for electricity. The war in Ukraine and Russia’s deliberate weaponization of oil and gas prices was a rude shock for the European economy, particularly Germany. Its industrial sector relied on cheap piped Russian gas, especially after shortsighted decisions a few years prior to decommission nuclear plants. Four years after the outbreak of the war, German industrial output has still not recovered, and with cheap gas probably gone for good, seems to be structurally impaired. France, in contrast, gets 70% of its energy from nuclear, and was not nearly as hard hit. Its 57 nuclear reactors were mostly built over 25 years following the 1974 oil shock in a deliberate attempt to gain energy independence. For similar reasons, we may be on the cusp of a global nuclear renaissance. It is a reliable and low carbon source of energy, but the upfront costs and long lead times mean it could take decades before the dream is turned into reality.

Chart 3: German and French industrial production

Source: LSEG Datastream

The world’s third and fourth biggest economies – India and Japan – find themselves in a similar situation of having to import oil for transportation and gas (and coal) for electricity generation. As in 2022, many Asian countries appear to have turned to coal to plug the gap. The war is therefore an environmental disaster. It is also likely to spur oil and gas exploration and development activity outside the Middle East (Namibia is one likely winner).

Nonetheless, the fastest and cheapest way for most countries to achieve energy security is by ramping up renewable energy combined with battery storage and increased adoption of electric vehicles (EVs). No enemy can block the wind or sunshine.

This suggests that the real winner from the Gulf War is China. Though it is a large oil producer – bigger than Iran, in fact – it is a net importer. But it deliberately positioned itself as the leader in renewable energy, dominating the production of solar panels, batteries, EVs and more. China is not only the main exporter of these technologies but also implements them at home with gusto.

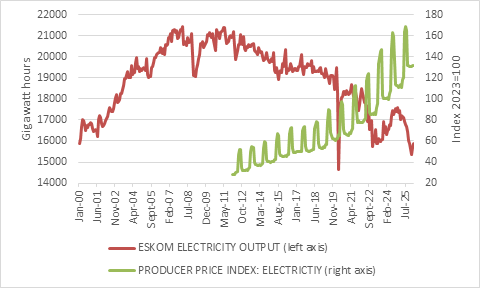

Chart 4: South Africa’s electricity production and cost

Source: LSEG Datastream

If there is one country that understands the importance of reliable energy, it is South Africa. “Loadshedding” was part of the daily vocabulary for a decade but thankfully seems to be a thing of the past. Since 2022, private companies are allowed to generate as much electricity as they want, and this policy change has been spectacularly successful. Hundreds of billions of rands are being invested in new generation projects, mostly solar and wind, and the pipeline of future projects is long. The challenge now is transmission, since the best locations for solar and wind energy are in the Northern and Eastern Cape respectively (geography strikes again) and connecting them requires more grid capacity. Here too there is substantial scope for private investment. The local electricity market is undergoing more change now than probably in the first 100 years since Eskom’s founding in 1923.

South Africa remains heavily reliant on coal-fired electricity, and it is one of the world’s largest coal producers and exporters. This means it has not faced double fuel and electricity shocks, though electricity is expensive regardless of the war, and a headwind to industrial activity. It also means South Africa is one of the world’s largest carbon emitters on a per capita basis. This is a long-term vulnerability once European countries (and others) start applying “carbon tariffs” on imports produced with fossil fuels. No wonder that many large local businesses are starting to source electricity directly from wind and solar farms.

Risks and opportunity

What is the key take-out for investors? Clearly, the ongoing uncertainty created by the Gulf War is unnerving. Most of the attention is on the short-term impact – i.e. the daily moves in the oil price – and with reason. The longer it remains high, the more stagflationary pressures build worldwide. However, there will also be longer-term implications if we think in terms of years instead of months. Much of this will surprise us, but some of it will simply be old realities coming to the fore again. Importantly, before we get too pessimistic, these shifts will create substantial new investment opportunities along the way.