Iran conflict: Asset-allocation and macro views from Schroders

Macro: What the conflict means for global growth and interest rates – David Rees, Global Head of Economics, Schroders

We have been concerned about global inflation risk in the economy for some time, and have pushed back strongly against the slow-growth narrative, particularly in the US, because we felt that fundamentals were good. Our view is that the economy is vulnerable to price shocks that can become ingrained through labour markets, for example through wage bidding, and a stagflationary environment can emerge.

While a brief spike in oil prices would have little lasting effect on inflation (as energy prices would need to be sustained higher over weeks or months before we see it push CPI meaningfully higher), higher sustained energy inflation would squeeze real incomes, weigh on growth and raise doubts about whether central banks, such as the US Federal Reserve, can continue easing monetary policy.

If we do get an inflationary shock and headline inflation pushes up, it may give central banks pause for thought as it becomes difficult to justify rate cuts when inflation is starting to push higher, meaning rate cuts are less likely. To get rate hikes, we would need to see these pressures becoming ingrained in wages and second-round effects where inflation becomes embedded.

Commodities: Implications for oil and other commodities – Malcolm Melville, Fund Manager, Commodities, Schroders

Prior to the recent Iranian attacks, oil was cheap by historical standards at mid $60s per barrel (bbl). Inventories were high and oil market participants were not expecting events that would push oil prices higher. The consensus for the rest of this year was that oil prices would fall.

In the wake of the attacks, oil prices have risen. The Iranian response has been broader and more aggressive than in past incidents, such as last year’s 12-day war in June which saw prices spike to $78/bbl and then quickly reverse.

Strait of Hormuz critical for numerous commodities

A key difference now is that the Strait of Hormuz – one of the world’s most critical shipping chokepoints – appears virtually closed. There have been attacks on vessels in the area, as confirmed by UK Maritime Trade Operations. This creates a more complex and fragile dynamic than in previous short-lived episodes.

The strait is a narrow and highly exposed passage through which flows approximately:

- 20% of global oil supply

- 20% of global LNG

- Significant volumes of fertiliser (e.g. 33% of urea)

- 7% of global aluminium supply

A prolonged disruption would therefore affect multiple commodity markets, not just crude oil. A key question is how long the current conflict might last. President Trump has mentioned a four-week timeframe.

Sourcing alternative oil supply unfeasible

If the shipping via the Strait of Hormuz remains impaired for a long period, sourcing replacement oil supply will be extremely difficult. OPEC has announced a 200,000 b/d increase but this is immaterial relative to the scale of potential disruption.

Iran produces 3.4 million barrels per day (b/d) and exports 1.7 million b/d, largely to China – these are the flows that are most immediately at risk. China may seek to replace these with Russian oil, which is otherwise subject to sanctions. Another factor to watch is if India begins buying Russian oil again.

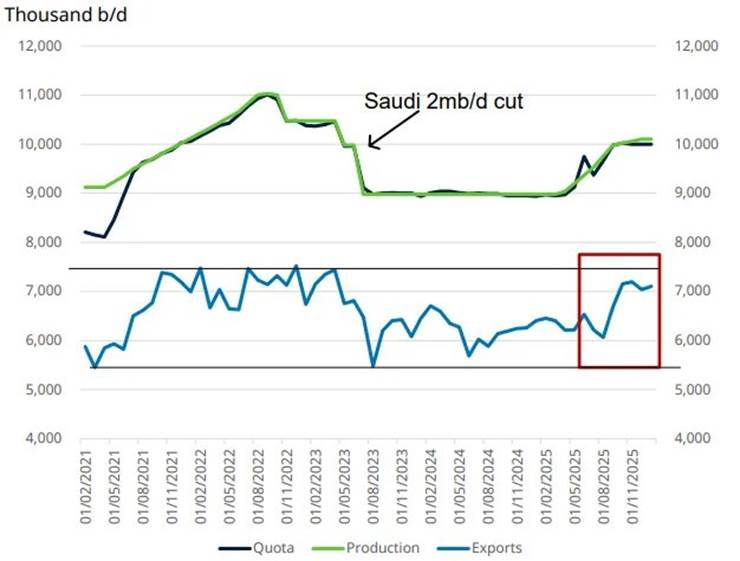

Disruption to shipping via the Strait of Hormuz would impact Saudi Arabia’s ability to export oil. Saudi Arabia exports 7–7.4 million b/d and could theoretically reroute volumes via its East–West pipeline. However, the pipeline has never operated at full capacity before and this would also require re-routing shipping, which would take time.

There is also the issue that Saudi exports are already close to their maximum levels. It seems unlikely that they have much flexibility to increase these, even if they are able to export via the pipeline rather than the Strait of Hormuz

Saudi Arabian exports close to maximum:

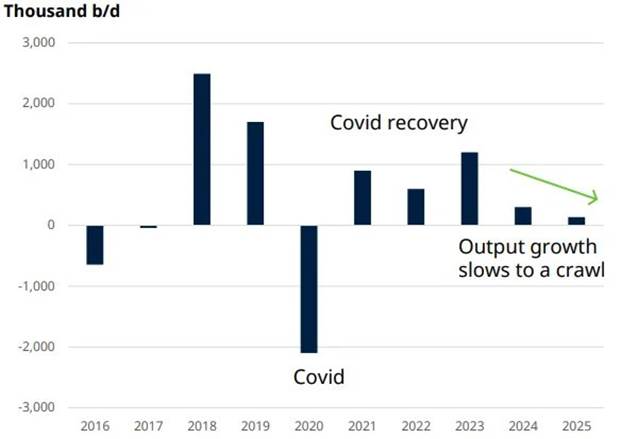

The US is not in a position to supply more oil to replace barrels held up by disruption. US shale growth has stalled and top-tier acreage is increasingly depleted. Even higher prices would not generate an immediate supply response given capital discipline and high investment hurdles.

Annual change in US oil production

In short, if the strait remains disrupted, there is no credible source of rapid replacement supply, leaving the market exposed to a meaningful deficit.

Oil prices likely to climb higher if conflict persists

Every day the conflict continues, 20 million barrels of oil are being lost – an unprecedented level of supply interruption. If disruption persists for several weeks, oil prices are at risk of accelerating sharply higher. Each additional week of impairment would likely increase market concern about sustained supply loss. A longer-lasting disruption could drive prices toward extreme historical levels.

Our estimates suggest that if access to the Strait of Hormuz is restricted for a period of four to five weeks, the oil price could rise to levels around $100-$120/bbl Oil did reach $120/bbl on Monday 9 March before falling back to around the $90 mark. If the conflict is prolonged for months, we could see prices rise above previous all-time highs, up to $150-$200/bbl.

Emerging Market Impacts - Philip Robotham, Head of Client Group, Schroders South Africa

The rapidly evolving situation is likely to sustain upward pressure on oil prices, keep geopolitical risk premia elevated, and potentially weigh on global risk appetite. Gold and commodities would likely remain supported under such a scenario.

Many emerging market (EM) economies have spent years adjusting their balance of payments positions and reducing their reliance on short-term foreign capital. This has helped them weather a number of external shocks in recent years and we believe they should be able to withstand current geopolitical dislocations.

We anticipate that the shifts in oil production may benefit some EMs – for example, the big producers, such as Brazil, Angola and Nigeria. Importers such as South Africa may find oil production shifts more challenging.

Multi-asset: Rethinking diversification – Remi Olu-Pitan, Head of Multi-Asset Growth and Income

Periods of geopolitical and macro uncertainty, such as the latest events in the Middle East, reinforce a core multi-asset principle: diversification must be deliberate and forward-looking.

Building portfolios with inherent hedges – including measured exposure to commodities and avoiding excessive concentration in any single sector – can materially improve resilience. When portfolios are structured proactively, investors are often in the more advantageous position of deciding where to take profits during market stress, rather than being forced to reactively cut losses.

In recent years, traditional assumptions have been tested. Bonds have not always behaved as reliable diversifiers, particularly during inflation shocks, and the long-standing strength of the US dollar has periodically come into question.

This is an environment where inflation will be under pressure to move higher – a very dangerous environment for government bonds because of elevated commodity prices. Conversely, solid global growth fundamentals support equities.

Incorporating real assets such as gold and broader commodities can play an important stabilising role. These exposures can provide diversification benefits when markets reprice and can help portfolios navigate supply-driven shocks or renewed inflation volatility. Thoughtful allocation to real assets therefore strengthens overall portfolio robustness when traditional hedges prove less dependable.