One battle after another

Izak Odendaal, Old Mutual Wealth Investment Strategist

The year started on an optimistic note for the local economy, with expectations of faster growth, lower inflation and falling interest rates. The Government of National Unity (GNU) seemed to be settling in after a few challenges last year, while the February Budget was well-received by the market, showing a gradual improvement in South Africa’s fiscal position.

Since then, it has been one battle after another, to steal the title of this year’s big Oscar winner. The record increase in petrol and diesel prices has clouded growth and inflation while the political direction is also unsure following the Constitutional Court hearing on the “Phala Phala” matter. South Africa has also featured in the hantavirus story, but largely positively given the quality of medical care offered to the victims. There is no indication that this will turn into another global pandemic, but after 2020 everyone is on heightened alert. The past few days have seen storms batter the country, and a national disaster has been declared.

Legal earthquake

Let’s start with the Constitutional Court’s landmark ruling, delivered on the 30th anniversary of the adoption of the constitution. It determined that Parliament was wrong in December 2022 when it buried the Section 89 report on the dollars that were stolen from President Ramaphosa’s game farm three years prior. It ordered that the report be considered by an impeachment committee set up by the Speaker of Parliament. If this committee finds grounds for impeachment, which could take us into next year, a two-thirds vote in the National Assembly will be needed to remove the President. Although the ANC no longer holds a majority in Parliament, its 159 of 400 seats in the National Assembly would be enough to block an impeachment vote. It will also be interesting to see how the other GNU parties respond, especially in the lead-up to the November local government election. President Ramaphosa could still take the original Section 89 to court for judicial review, which means this matter could still drag on well into next year. His term of office as ANC president will end late 2027, while the 2029 general election is still far off.

Several scenarios now loom. One is that Ramaphosa fights back and uses the courts and other means to delay proceedings for as long as possible until his term runs out anyway. The second is that he chooses to resign, rather than be dragged through an unseemly process. This would propel Deputy President Paul Mashatile into the hot seat. A third possibility is that impeachment proceedings continue but ultimately fail to meet the two-thirds threshold. In each of these scenarios, there is also the possibility that some GNU partners decide to jump ship, and a new ruling coalition emerges.

Chart 1: World Bank Rule of Law score against per capita income, selected countries

Source: LSEG Workspace

Markets don’t like political uncertainty in the short term. Over the longer term, however, rule of law matters more. It is crucial for economic development and well functional capital markets, and as chart 1 shows, it is strongly correlated with higher levels of national income. The fact that South Africa has an independent judiciary remains a major strength and the Constitutional Court has again demonstrated that it does its work without fear or favour. There are increasing doubts over whether one can say the same of the US Supreme Court, for instance. But in South Africa, the principle that no one is above the law still holds.

Policy, not politics

The main question for investors is about policy, not politics or personalities. None of the scenarios described above imply a dramatic shift away from the current policies aimed at fiscal consolidation, unbundling of state monopolies, fostering greater private investment in key network industries, and generally improving state capacity and lowering the cost of doing business.

There is a broad cross-party consensus that the country needs faster economic growth, and several key reforms have already been legislated. However, a new president or new coalition government could shift the emphasis in one way or another. Unfortunately, the crucial but uncompleted reforms needed to address corruption and underperformance of the police, as revealed by the Madlanga Commission, could be a victim of politics. This is the main reason why South Africa’s rule-of-law score isn’t higher.

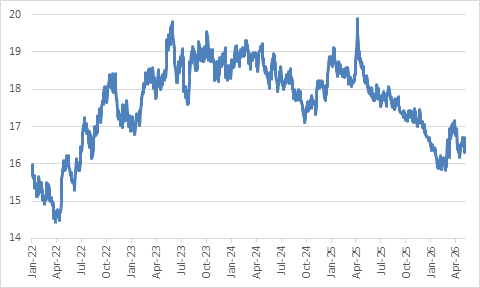

Chart 2: Rand dollar exchange rate

Source: LSEG Datastream

Muted markets

The market reaction following Friday’s Court ruling was muted, with local bonds and equities largely trading in line with global benchmarks, while the rand was only a touch weaker. The ruling wasn’t a big surprise, and perhaps markets are just less jittery when it comes to South African politics than in the past, recognising that in a coalition era, it is less important who the president is. Of course, there are also other developments happening in the rest of the world. The first Friday of the month is when US employment data is released, one of the most important pieces of information informing the global economic and interest rate outlook. It showed solid jobs growth (115,000 in April), which means consumer spending should remain well supported in the world’s largest economy. The other is the Gulf War, where a fragile ceasefire still holds, and cautious talks between the US and Iran continue, though President Trump has rejected Iran’s latest offer. The oil price has been very volatile over the past few weeks as the odds of deescalation in the conflict has ebbed and flowed, but it remains around $100 per barrel. While elevated, it is not intolerable for the world economy. However, should the Strait of Hormuz remain closed for several weeks more, the oil price is likely to rise as stockpiles are depleted and shortages emerge. The availability of associated products like jet fuel would similarly become constrained, in turn hampering the transport of other critical products around the world.

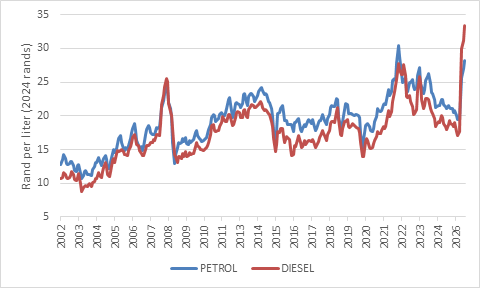

Chart 3: SA retail petrol and diesel prices, adjusted for inflation

Source: Central Energy Fund, Stats SA

Retail fuel costs have already jumped in South Africa, with the monthly adjustments in April and May leading to higher petrol and diesel prices. The country is generally in a better condition to absorb the blow compared to 2022, when the war in Ukraine caused a similar spike in global oil prices. An improved fiscal situation means the South African government will forego R17 billion in tax revenue and has offered relief in the form of a temporary reduction in the fuel levy for the months of April, May and June.

Chart 3 shows the petrol and diesel price adjusted for inflation to allow for a fair comparison over time. It includes the tapering of fuel levy relief from June onwards. Both are very high, but the diesel price has increased the most and is at an all-time high in real terms. Therefore, on a relative basis, the hit is greater on companies and farmers than on households. However, as in the rest of the world, producers will ultimately pass on some of these higher input costs to consumers. It is just a question of how much, something the Reserve Bank will monitor closely.

Money markets have already priced in the likelihood of the Reserve Bank hiking rates twice to reinforce its commitment to achieving the 3% inflation target. Apart from the impact of global fertilizer shortages due to the closure of Hormuz, the risk of a severe El Nino event this year could result in rising food inflation. Food and fuel are regular household purchases, making increased prices highly visible to consumers, thereby risking a de-anchoring of inflation expectations.

However, any rate increases are likely to be modest and possibly unnecessary. They certainly won’t affect fuel prices, which is a classic supply shock. Inflation was on target at 3% on the eve of the war, and the Reserve Bank’s policy rate was elevated at 6.75%, a real interest rate of almost 4%. Again, this contrasts with 2022 when the real policy rate was negative, and the Reserve Bank had to play catch up. The rand also weakened substantially in 2022 and 2023, as chart 2 shows, whereas this year it has been relatively stable. The latter is important, since the rand-dollar exchange rate is also a very visible variable that feeds into people’s perceptions of future inflation.

While few want higher interest rates, the bigger picture matters. The Reserve Bank aims to bring inflation down to 3% on a sustained basis. This requires a degree of faith on the part of South Africans, namely we should all believe that the Bank is committed to its goal and we should have 3% in the back of our minds when we are negotiating with our landlords, for instance, or when unions table salary demands.

Short-term headwinds, long-term tailwinds

Higher fuel costs and potentially higher interest rates mean that economic growth in 2026 will undershoot the forecasts made at the start of the year. Instead of 1.5% growth in 2026, it is more likely to be around 1.2%. This is clearly not a recessionary level. In the meantime, South Africa still benefits from elevated precious metals prices and recorded a R31 billion trade surplus in March. Consumer spending is likely to come under pressure, but perhaps it might be more resilient than many fear, with higher income consumers benefiting from strong investment returns over the past three years. For instance, April’s new vehicles volumes were 13% higher than a year ago, despite the fuel price jump.

Since South Africa is a net fuel importer (though a net energy exporter due to its abundant coal reserves), the Gulf War is a headwind for the local economy. However, the broader geopolitical context could still prove to benefit the country. Shipping in the Middle East will carry a risk premium for a long time, making the longer journey around the Cape a viable alternative. This presents an economic opportunity and reminds the rest of the world of the country’s strategic importance. Secondly, the Gulf crisis is likely to reemphasise the importance of energy security, and indeed security of supply of a broad range of important raw materials. While equity investors are getting carried away with artificial intelligence again, it cannot happen without copper, steel, lithium, silver and many obscure “rare earth” minerals. Many people were surprised to learn that helium is not just used for party balloons but is a key ingredient in manufacturing semiconductors and that Qatar is a major supplier, with its output trapped behind the Hormuz blockade. South Africa happens to be an emerging producer.

The tech boom of the past decade or so also means that the global mining sector was starved of capital and did not invest enough in exploration and expansion to meet the future need for raw materials. While not necessarily a “supercycle,” this points to commodity resurgence already visible in precious metals. South Africa is and will be a beneficiary. For instance, the Financial Times reported that despite otherwise frosty relations, the US and South African governments held preliminary talks last week to discuss minerals cooperation.

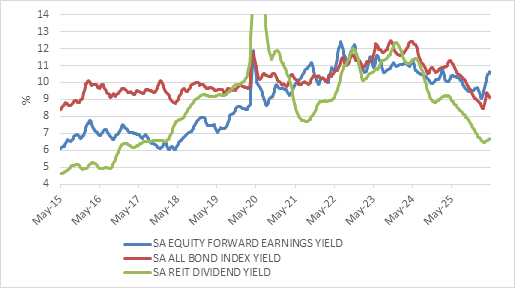

Chart 4: SA equity, bond and property yields, %

Source: LSEG Datastream

For now, the global environment remains fragile, with investors closely watching and hoping for a breakthrough that would see the Strait of Hormuz opened. At the same time, markets must now also contend with increased domestic political uncertainty, which could lead to market volatility for the rest of the year. However, there are longer-term fundamental tailwinds for South African asset classes, supported by attractive valuations. The Reserve Bank is determined to anchor inflation at 3%, but bond, equity and property yields are currently above even pessimistic inflation assumptions. This suggests that the real return outlook for patient local investors remains solid.