Political football

Izak Odendaal, Old Mutual Wealth Investment Strategist

The 2026 FIFA World Cup has been a welcome distraction, but the “Football Unites the World” motto is a stretch. The world seems more divided than ever, and more uncertain. The US, a co-host, remains at war with Iran, though a fragile ceasefire has allowed oil supplies to start normalising and energy prices have declined rapidly. The reason the present geopolitical environment feels so uncertain is not so much that there are more conflicts between states – most are usually often overlooked in the Western media in anyway – but because the Western countries are involved, either directly or indirectly. More specifically, the US has gone from being the anchor of the so-called “rules-based international order” to a source of instability, while Europe must deal with Russian revanchism on its doorstep. This sense of geopolitical instability is further driven by domestic political upheaval. Arguably, the traditional left-right political spectrum that dominated politics in the 20th century is now a matrix. Politicians are not only defined by whether they believe in free markets (right) or government intervention (left), but also by whether they are mainstream politicians who believe in institutions, or populists who want to tear up the system.

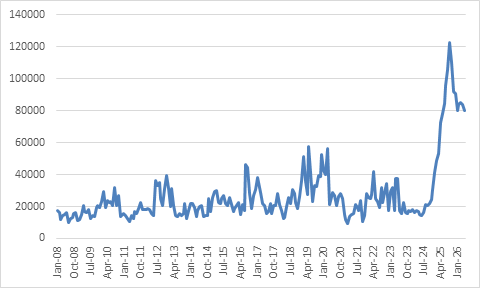

Chart 1: World Uncertainty Index

Source: worlduncertaintyindex.com

Bregets, I’ve had a few

Take the UK as an example. Within the space of a few days, it commemorated the 10th anniversary of the Brexit referendum while also learning that it would soon have a new prime minister. The two are linked, as the Brexit vote and rise of populism have reshaped British politics, probably ending the 100-year-old two-party system. There have been six prime ministers in the past decade – soon to be seven – compared to only eight over the previous 50 years. Populism has long stalked Latin America and elsewhere, but the Brexit vote to leave the European Union in June 2016 was probably the first time it forcefully emerged in the English-speaking world. It was a classic exercise in scapegoating, blaming Britain’s problems on the bureaucratic elite in Brussels and migrants, while offering a single quick-fix solution: leave the EU and everything will get better. Instead, many things deteriorated and today a majority believe that leaving the EU was a mistake. With characteristic British humour, this Brexit regret is known as “Bregret”. There was no immediate post-Brexit recession, but there is little doubt that the UK economy is smaller today than it might have been had it remained within the EU. Moreover, the timing of the vote couldn’t have been worse, since the world has changed. Brexiteers thought they could turn the country into a free-trading champion, but the global free trade agenda has been under attack from US President Trump, the other symbol of populism.

There are different definitions of populism, and different variants across time and place. Broadly speaking, however, populist movements tend to share the same playbook:

- A strong, charismatic leader who argues that he (usually a man) is the embodiment of the nation.

- An “us versus them” narrative where “the people” are positioned against a corrupt elite or outsiders (immigrants or ethnic minority groups), with the latter blamed for the country’s problems.

- A disdain for democratic checks and balances, since the leader or the movement represents the “true will” of the people.

- “Silver bullet” economic policies are put forward to address complex problems, but they ultimately make things much worse over the long term.

- A sense of nostalgia for an imagined past. Trump’s “Make America Great Again” harks back to better days, while the Brexit mantra “Take Back Control” reflects a time when Britain was supposedly in control of its own destiny.

The rise of populism in the West is, of course, a multi-faceted phenomenon. However, there is broad agreement that at least four key trends are at play:

- De-industrialisation, driven by the rise of China and other outsourcing hubs as well as automation, saw the decline of well-paying manufacturing jobs for low-skilled workers. These losses have been concentrated in “Rust Belt” communities.

- A loss of trust in institutions, particularly following the 2008 Financial Crisis, when there was the broad and not entirely unfounded view that the bankers responsible for the calamity were bailed out, while ordinary people were left to suffer (a case of privatising the gains but nationalising the losses).

- A sense that the culture is shifting, whether through social issues or more immigrants who look, speak and worship differently. This creates fertile ground for politicians to stoke “culture wars” and divide the population, amplified by social media echo-chambers.

- Rising inequality and a sense that the system is rigged in favour of elites. It took a hundred years between John D. Rockefeller becoming the first billionaire and Jeff Bezos becoming the first centibillionare (worth $100 billion) in 2017. Remarkably, it took only another nine years before Elon Musk became the first trillionaire. It is not just about tech moguls, however. In many Western countries, there is a more mundane but equally frustrating form of inequality as expensive housing markets lock young people into a lifetime of renting, while benefitting older homeowners. According to the Office of National Statistics, the average London home cost the equivalent of 4.4 years of average annual income in 1995. Three decades later, that figure had risen to 10.6 years.

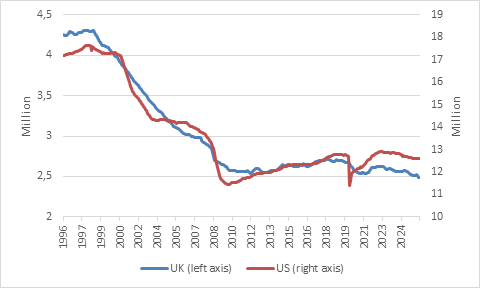

Chart 2: De-industrialisation: the decline in manufacturing jobs

Source: LSEG Datastream

None of these causes of populism and political division show clear signs of improving, meaning that politics could get even more challenging over time. If artificial intelligence (AI) disrupts labour markets to the extent its proponents argue it will, popular anger could rise further. AI could also be a handy tool for sowing misinformation and further undermining trust. Immigration, a big driver behind support for far-right parties across Europe and the MAGA movement in America, will likely become even more of a vexed issue.

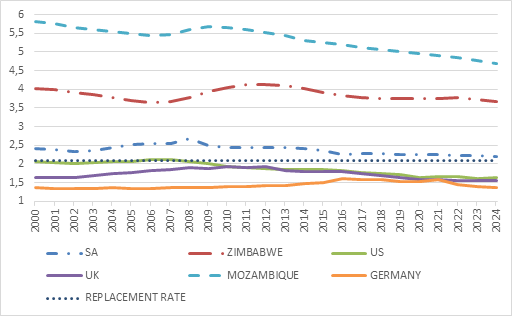

This is because birthrates across the Northern Hemisphere have fallen well below replacement levels. Immigration is the only way to ensure a stable, never mind increasing, labour force. Countries face a choice: limit immigration in the name of social cohesion and shrink or grow through accepting more immigrants. The challenge then becomes assimilation, something European countries have struggled with.

Chart 3: Birth rates in selected countries

Source: World Bank

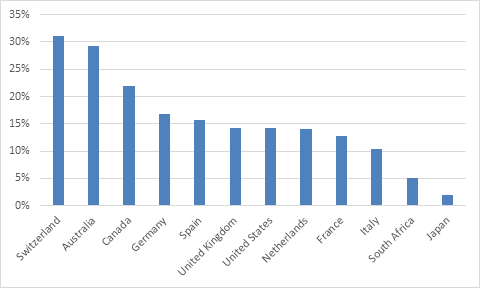

Immigration is an emotive topic in South Africa too. The country is on edge this week ahead of planned anti-immigrant protests, amid concerns that tensions could escalate given the history of xenophobic violence over the past 20 years. Of course, the labour market dynamics are very different. In rich countries, migrants tend not to compete with locals, often doing the low-skilled jobs locals do not want. In South Africa there is intense competition for low-skilled work, but it should be acknowledged that migrants also bring entrepreneurial drive and talent. The government acknowledges that the country’s borders have been far too porous, though the estimated foreign-born population of 3 million people is relatively small compared to richer and older countries.

Chart 4: Foreign-born population as share of the total

Source: OECD, Stats SA

A crackdown on migrants risks a different type of backlash. If the rest of the continent develops a negative view on South Africa over alleged xenophobia (many people from other African countries pointedly supported Bafana’s opponents), it reduces the country’s soft power on the continent. This could also create headwind for South African businesses. Since the country’s economic future is intertwined with the rest of Africa, this does tremendous damage.

Risk and opportunity

This issue is also not going to get easier. Sub-Saharan Africa is the only region in the world still experiencing rapid population growth. Its young and growing population is a tremendous opportunity for South African businesses, but we must assume most African countries will fail to produce enough jobs for burgeoning labour forces, which will lead to ongoing out-migration, including to South Africa. Therefore, there is fertile soil for populism across the continent, and in South Africa.

Simply put, the risk remains that a lack of meaningful economic growth and job-creation in South Africa leads the electorate to embracing populist politicians – or that mainstream parties turn to populist policies to outflank them. The structure of the South African political system helps. A coalition environment will by nature include many different voices. Even if populist parties form part of the governing coalition, their impact will be diluted. In presidential systems such as the US and much of Latin America, it is easier to win by a small margin and then claim to be the only true representation of the nation.

Nonetheless, a rise in populism would likely be negative for the economy and financial markets, which is why investors already demand a risk premium in South African bonds and equities. While greater political maturity and faster economic growth can reduce the premium, it is unlikely to disappear in what remains the most unequal society in the world and fertile soil for populism. The more intriguing question is if such an “inequality discount” will rise in other markets.

Investment implications

in closure, a few investment implications for South African investors. The last point argues for sufficient diversification. Local politics can take a turn for the worst again, and international exposure is the best hedge against this. By the same token, it should be clear that this is far from the only country where people are unhappy. Overexposure to South African assets is risky, but when valuations are attractive – such as now, broadly speaking – investors can still lean into domestic asset classes.

The broader question is what sort of risk premium or valuation buffer investors should demand for investing everywhere. There isn’t space in this article to tackle global government debt levels, for example, but one of the ways in which governments have been able to absorb popular anger in the West has been through borrowing and spending more. When that is no longer an option, the political fallout could be severe. Another example is AI, where it doesn’t seem to be on many investors’ radar screens that a political backlash could happen that will be negative for shareholders.

Nonetheless, it should also be pointed out that despite the upheaval of the past decade, investment returns have been good. Focusing on the headlines and betting against the market was also not a good idea. For instance, while UK stocks have lagged the US market, they haven’t been specifically hurt by Brexit since many are multinationals, also benefiting from a weaker pound.

Finally, geopolitics evolves and technology changes, while human nature doesn’t. We still make important investment decisions in using brains that evolved on the African Savanna over hundreds of thousands of years. Our mental tools to understand this complex landscape are the same ones that helped us avoid predators and find food or mates, while our emotion state often swings between greed and fear. Even in a turbulent world, the biggest risk most investors face are themselves.