The compounding power of micro wins in investing

Thandi Skade, communications manager at Allan Gray

Most investors fail to achieve their financial goals not because they lack good intentions, but because these goals can feel emotionally demanding. This is particularly true for long-term goals, such as saving for retirement. But by harnessing the power of micro wins, big financial goals are certainly within your reach, asserts Thandi Skade, communications manager at Allan Gray.

“Given the unpredictable nature of financial markets, the long-term horizons associated with investing and the absence of instant gratification, investment plans that rely on motivation alone are vulnerable to distractions and inertia,” states Skade. “However, those anchored in momentum tend to be more resilient.”

Psychologists and behavioural scientists draw an important distinction between motivation and momentum that is particularly insightful in long-term investing; motivation may trigger action, but momentum is what sustains it. “Motivation fades, while momentum endures,” Skade emphasises.

The power of micro wins

So, how do investors turn their initial motivation to invest into sustained momentum? “By relying on small actions that are easy to repeat – a concept known in behavioural science as micro wins,” explains Skade.

Research shows that completing a manageable task – such as finalising your monthly budget or making an initial contribution to an investment – triggers the release of dopamine (the feel-good hormone), which encourages repetition.

“While the financial impact of a single micro win may be modest, the behavioural impact is not,” she comments. “Each small success provides psychological reinforcement, which, in turn, increases the likelihood of repeating the behaviour and gradually turning intention into habit.”

Three paths, varying outcomes

If micro wins help sustain behaviour in everyday life, can they be applied to our approach to long-term investing?

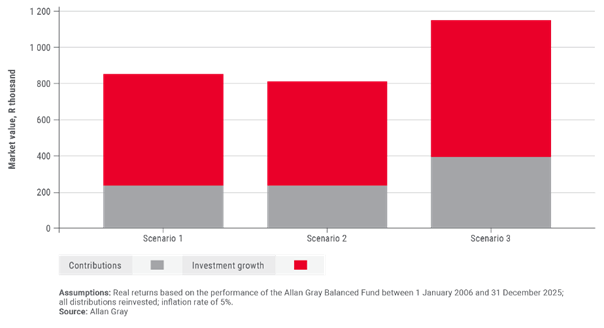

To test this principle, Allan Gray compared three contribution behaviours of the Allan Gray Balanced Fund over a 20-year period from 2006 to 2025, assuming identical market conditions, an inflation rate of 5% and that all financial gains would be reinvested (see Graph 1).

In Scenario 1, an investor contributes R12,000 as a lump sum at the start of each year (equivalent to R1 000 per month without escalation), resulting in a final investment value of R857,248.

In Scenario 2, the investor instead contributes R1,000 monthly via debit order with no escalation. This automated approach delivers a slightly lower final value of R815,275.

In Scenario 3, the investor combines automation with a 5% annual escalation to keep pace with inflation. This disciplined and inflation-aligned strategy produces a significantly higher final value of R1,153,962.

Viewed together, the scenarios highlight three important insights. “Firstly, small actions are behaviourally powerful even when their immediate financial impact appears modest. Scenario 1’s upfront investment approach benefits from early market exposure but relies on a single high-effort decision. Scenario 2 exchanges some of the potential upside for a system that is psychologically easier for investors to sustain in the long term.

“Secondly, adding a layer of progression, in the form of annual inflation-adjusted debit order contributions, amplifies the effect, protects purchasing power and enables capital to compound alongside the behaviour,” Skade explains.

Finally, with more than two-thirds of the final values generated from investment growth, our analysis underscores the impact of consistent behaviour in compounding returns over time, adds Skade.

Graph 1: The power of compounding

Progress over perfection in practice

According to Skade, translating micro wins into action doesn’t require dramatic changes or flawless execution. “The aim is not to optimise every decision, but to design defaults that make steady progress easier,” she maintains.

Below are her top three ideas to get the most of micro wins in investing:

- Make consistency the default: Regular debit orders are one of the simplest ways to turn intention into action. This matters because decision fatigue is a real phenomenon, and even well-intentioned investors are more likely to delay or disengage when repeated effort is required.

- Let progress happen gradually: Small, incremental and scheduled annual escalations, whether linked to time, salary increases or inflation, allow progress to compound without demanding noticeable lifestyle changes.

- Rebound from lapses: If life happens and you find yourself needing to pause contributions, it is psychologically important to treat the interruption as temporary, not a failure, and to resume your contributions as circumstances allow.

“If a crisis forces you to stop your monthly contributions, treat it as a temporary setback and resume your debit order as soon as possible,” she recommends.

“This year, as we focus on our financial resolutions, let the quiet power of consistency compound, and allow time to do the heavy lifting,” concludes Skade.