Equity earnings are on the up, with emerging markets leading the way

Duncan Lamont, CFA, Head of Strategic Research at Schroders

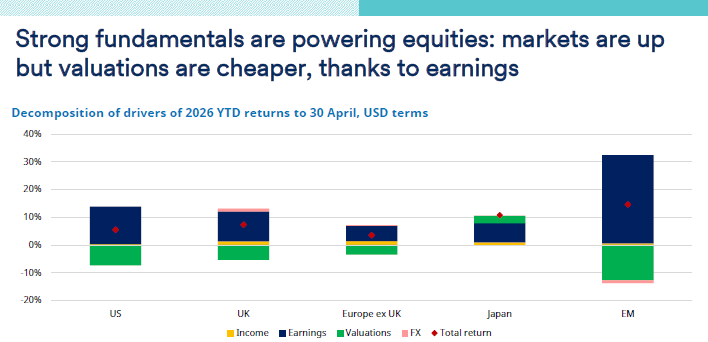

Strong earnings growth has been the story behind equity returns over the past decade, and continues to underpin global markets today. Although markets are up, valuations in several regions have become cheaper as earnings growth has accelerated.

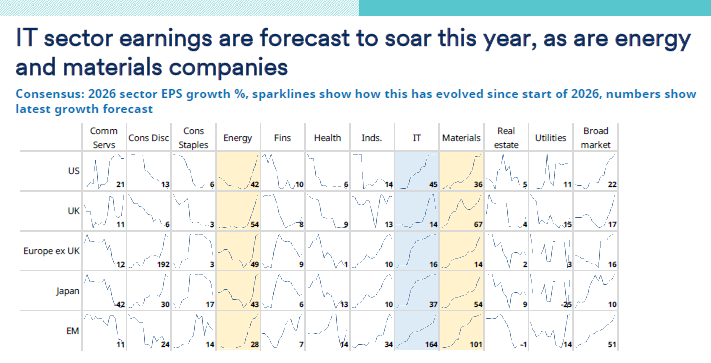

The outlook for earnings growth remains broadly positive across all major regions, with emerging markets forecast to lead in 2026. The information technology (IT) sector is expected to deliver particularly strong earnings this year, alongside energy and materials companies. However, the outlook begins to diverge in 2027, with rapid IT earnings growth expected to continue while energy earnings are forecast to weaken.

Despite the broader picture of elevated market valuations, emerging markets, the UK and Europe continue to trade on relatively undemanding valuations relative to next 12 months’ earnings. Smaller companies also remain on depressed valuations relative to larger peers.

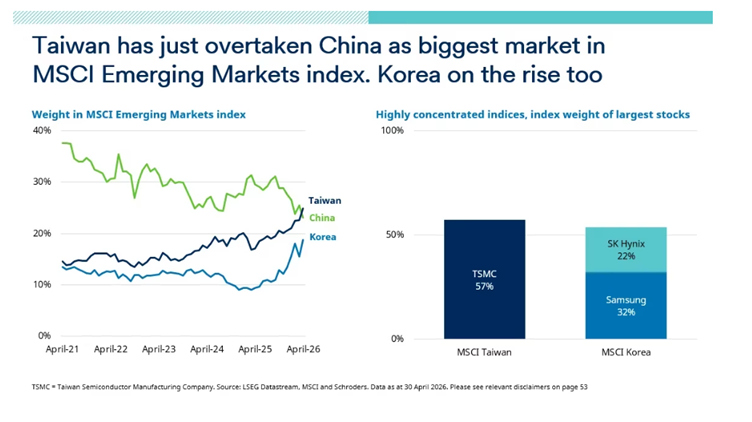

Taiwan surpasses China in MSCI Emerging Markets Index weighting

The growing dominance of technology-related earnings is also reshaping emerging markets indices. Taiwan recently overtook China as the biggest market in the MSCI Emerging Markets Index, while Korea’s weighting has also continued to rise.

These are highly concentrated markets, with TSMC accounting for 57% of MSCI Taiwan, while Samsung and SK Hynix make up 54% of MSCI Korea. All three companies are closely correlated with the AI trade, highlighting the extent to which investors’ emerging markets exposure is increasingly tied to a relatively small number of technology stocks.

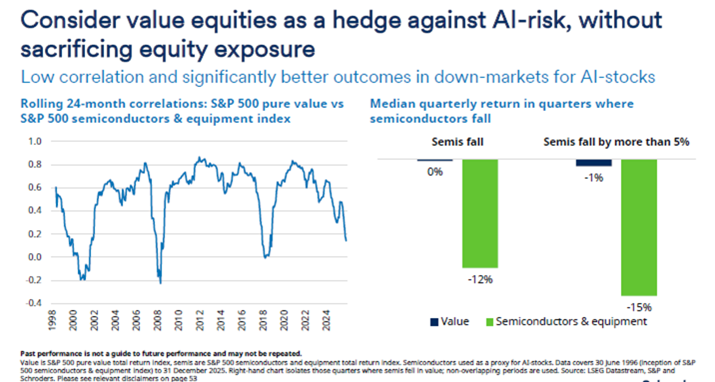

Value equities as a hedge against AI concentration risk

This concentration raises a broader portfolio construction question. For investors heavily exposed to AI-driven growth, diversification within equities is becoming more important. One potential counterbalance is value investing. Historically, value equities have exhibited lower correlation to technology-heavy segments and have tended to be more resilient during periods when these stocks come under pressure.

However, a passive approach to value investing is unlikely to shield investors from AI concentration risk. Most indices still retain meaningful allocations to large technology names, including the “Magnificent Seven”. This overlap can dilute the diversification benefits investors might expect from a value allocation. Investors seeking a genuine hedge to AI-driven concentration risk may therefore need to look beyond standard passive approaches and consider more selective implementations of value strategies.