Fighting the next war

Izak Odendaal, Old Mutual Wealth Investment Strategist

It is often said that central banks fight the last war. This phrase takes on a different meaning when there is an actual war underway, with major implications for the global growth and inflation outlook. The last week has seen a further escalation of fighting in the Gulf, with heavy hits on oil and gas facilities that sent energy prices soaring even further. Hopes for a speedy resolution of the conflict are fading by the day. With the Strait of Hormuz still largely closed and energy infrastructure targeted by missile and drone strikes, upward pressure on the oil price has increased. The Brent crude oil benchmark closed above $110 per barrel last week, but the prices of other grades of crude and some refined products, like jet fuel, have soared even more.

It seems that only a deliberate de-escalation of the fighting by the US and/or Iran can calm energy markets. There have been mixed messages from US President Trump on this score. Sustained fighting lasting months rather than weeks will see the oil price retest the all-time 2008 high. It is against this difficult backdrop that several central banks held policy meetings last week, with the South African Reserve Bank set to take its turn this week.

Backward looking

The reason central banks are accused, sometimes unfairly, of fighting old battles is that they tend to be scarred by the mistakes they made. As the worst of the Covid pandemic faded, central banks in the developed world remained focused on the prior decade of persistently low inflation. In doing so, they missed how rapidly inflationary pressures were building. Inflation was rising steadily and across a broad front even before Russia invaded Ukraine in February 2022, sending food and energy prices surging. After initially dismissing inflation as “transitory”, monetary policymakers were forced into catching up by hiking interest rates aggressively. Higher interest rates sent markets crashing in 2022 and compounded the misery of the cost-of-living shock for households.

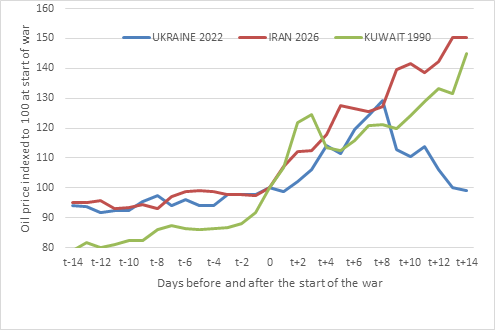

If central banks were to “fight the last war” today, they would fear the inflation impact of oil prices more than the economic growth knock and start raising rates. It would be an error, since the backdrop is different to 2022. The Middle Eastern supplies much more oil than Russia, therefore the potential of the oil price shock is larger, as chart 1 shows, but the broader environment is different.

Chart 1: Brent oil price movements in times of war, $

Source: LSEG Datastream

Punchdrunk

Central banks have effective tools to respond to demand-led inflation. As the late Federal Reserve Chairman McChesney Martin famously quipped, central banks must take away the punchbowl just as the party gets going. Supply shocks are a different matter, and this is probably the worst supply shock in decades. Central banks can do nothing about oil supply – they don’t drill wells or build pipelines. Therefore, the textbook response to inflation caused by fuel price spikes is to focus on the behaviour of firms and consumers. If companies pass on higher transport costs to consumers, inflationary pressures can broaden, known as the second-round effect. This will depend on several factors, with the main one being the duration of the oil price spike. Most companies will be reluctant to immediately hike prices, but they can only absorb higher transport costs for a few months. Beyond that, the margin pressure becomes too intense.

When companies start raising prices, there is a risk that it becomes self-sustaining if consumers in turn start believing that higher inflation is here to stay. Central banks therefore pay attention to the long-term inflation expectations of participants in the economy. If households, businesses and workers believe that inflation will eventually settle down again, there is little to worry about. However, if these expectations become unmoored, central banks are more likely to act decisively, taking away the punchbowl to prevent the party from even starting.

In practical terms, it means watching how “core” inflation behaves, more than headline inflation. Core inflation excludes volatile food and fuel prices, not because they don’t matter to consumers – on the contrary – but because they are volatile and tell us little about underlying inflationary pressures. Headline inflation rates across the world will rise sharply in the next few months, but it is the increase in core inflation that will come under scrutiny.

Mostly sideways

With this general backdrop in mind, we can turn to how monetary policymakers in individual markets are responding. Most will sit on the fence until there is a better sense of how the situation is evolving. One exception is the Reserve Bank of Australia (RBA), which hiked for the second time in a row last week. This is not primarily due to oil prices. Australia is a big gas exporter and therefore benefits somewhat from this crisis. Rather, it hiked due to underlying inflationary pressures that are unique to Australia. However, this is a reminder that interest rate cycles do turn eventually. As recently as 12 months ago, the RBA was still lowering interest rates.

Japan is the only other major economy in a hiking cycle, although its central bank left interest rates unchanged at its scheduled policy meeting. It is gradually lifting interest rates after decades of near-zero levels but is careful not to undermine the nascent economic recovery. Compounding the impact of higher oil and gas prices – Japan is one of the biggest energy importers – is a weak yen, which is trading near 30-year lows against the dollar.

The European Central Bank (ECB) has a bad reputation when it comes to oil and interest rates. In July 2008, as the world stood on the brink of economic calamity, the ECB hiked as the oil price was hitting a record level of $150 per barrel. It was forced to reverse course a mere three months later when it launched an aggressive rate-cutting cycle. It repeated the error in 2011, when oil was again above $100, hiking rates twice on the eve of the eurozone fiscal crisis, which soon saw it cutting rates down to zero, and eventually, into negative territory.

The ECB must be careful not to repeat those two mistakes. Europe is also a net importer of oil and gas, and it was the surge in gas prices that really choked the economy in 2022. Gas is a much more fragmented market than oil because so much of it is delivered via pipelines rather than by sea. At its worst, European gas prices jumped a hundredfold in 2022 when Russian supplies were cut, delivering a serious economic blow, but also feeding into inflation. Today’s gas price increase is steep, but nowhere near as bad.

Moreover, on the eve of the war in Iran, Eurozone inflation was well-behaved near the 2% target, and the ECB was expected to be on an extended pause. In other words, unlike 2022, there were few other inflation risks when the crisis hit.

This is not quite the case in the United Kingdom, where inflation has been above 2% for most of the past four years. The Bank of England’s Monetary Policy Committee (MPC) unanimously left its policy rate unchanged at 3.75% with Governor Andrew Bailey warning that it was “ready to act” on inflation if needs be. It is far too early to say whether rate hikes are likely, but the possibility is now firmly out in the open.

US inflation was also somewhat worrying even before the missiles started flying. Sharply higher import tariffs raised goods inflation in the US last year, but services inflation has also been sticky around 3%. The US central bank, the Federal Reserve, nonetheless lowered interest rates last year due to concerns that the labour market was losing its vigour, which can ultimately result in higher unemployment rates. The Fed has a unique dual mandate to maintain both stable inflation of 2% and low unemployment.

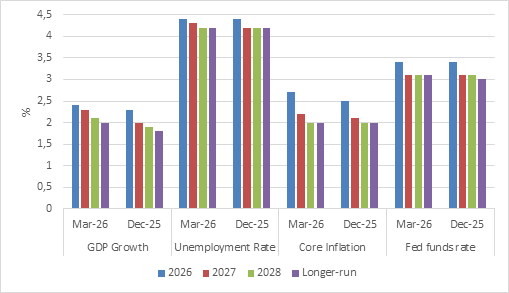

Like the above central banks that kept their policy rates unchanged last week, the Fed also did nothing, as expected. However, its views on inflation were more hawkish than the market expected. Fed officials are also more optimistic about economic growth this year, as summarised by the quarterly dot plot. Assessments of 2026 GDP growth were raised to 2.4% from 2.3%. The US is the world’s largest oil and gas producer, and while its car-loving consumers will take a knock from higher gasoline prices, the fossil fuel industry will benefit. If growth is indeed this solid, there is no need for lower rates.

The dot plot expectation for 2026 core inflation was increased to 2.7% from 2.5% in December. The dot plot still points to a single rate cut in this cycle, but the market has basically priced out the possibility of lower rates this year. Chair Powell noted in the post-meeting press conference that some officials believe that the next move in the cycle will be a rate hike.

Chart 2: Summary of US economic projections (dot plot)

Source: US Federal Reserve

Central banks are not fortune tellers. The Fed’s dot plot in December 2021, on the eve of Russia’s invasion of Ukraine, pointed to gentle interest rate increases. It expected the Fed funds rate to rise from 1% to 2.5% over the following three years. Instead, rates lifted to a peak of 5.5% in 2024, including three jumbo 75 basis point hike in 2022.

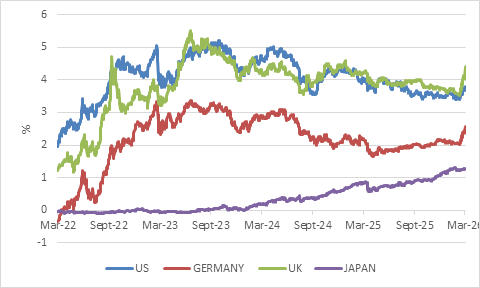

Chart 3: 2-year government bond yields, %

Source: LSEG Datastream

Investors also don’t have crystal balls but must nonetheless try to price in the most likely future scenario in real time. The rapid increase in government bond yields, especially shorter-dated yields, points to a notable shift in interest rate expectations towards no further interest rate cuts and the possibility of hikes. These in turn push up corporate borrowing costs too, as well as mortgage rates in the US. In other words, there has been a broad if undramatic tightening of financial conditions that will do some of the central banks’ inflation-fighting work for them.

Calm before the storm

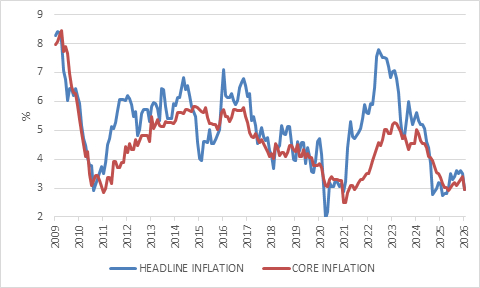

The same is true in South Africa, though bank lending plays a larger role in our economy, meaning changes in the repo rate ultimately do most of the heavy lifting. The South African Reserve Bank’s MPC will meet this week and is likely to keep the repo rate at 6.75% for the foreseeable future. There is some comfort in the fact that, on the eve of this global shock hitting its shores, South Africa’s inflation picture was benign and called for further interest rate cuts. Headline consumer inflation came in lower than expected in February, with a year-on-year reading of 3%. Core inflation was also 3%.

Of course, this predates the surge in global oil prices. Petrol inflation was -10% year-on-year in February but will jump to around 20% in April once the roughly R5 per litre petrol price hike goes through. Fuel’s direct weight in the CPI basket is quite small at 3.8%, meaning that it will directly add between 0.5 and 1 percentage points to inflation in the coming months, with the number rising towards the end of the year due to base effects. However, it is the other 96% of the CPI basket that the Reserve Bank will monitor closely for passthrough from higher transport costs to consumer prices.

Chart 4: South African inflation

Source: Stats SA

The behaviour of the rand-dollar exchange rate will also play a role in inflation, inflation expectations, and the Reserve Bank’s reaction. The Reserve Bank’s commitment to its new 3% target and its inherent conservatism means it will likely favour inflation overgrowth if pushed, though it is far too early to talk about rate hikes. Given the absence of pre-existing inflationary pressures and the need to water South Africa’s economic green shoots, raising interest rates could well be a policy error, akin to again fighting the last war.

Sitting tight

In conclusion, most central banks are sitting tight for now. These are policymakers with decades of experience, access to large teams of researchers, and with the latest data at their fingertips. However, they are just as unable to predict what happens in the next few weeks as anybody else. The conflict can simmer down, in which case oil prices will ease off, or it can escalate, leading to further petrol price pain. If you don’t know what to do, doing nothing is also doing something. That is worth remembering when thinking about your own portfolio too.