Life at $100

By: Izak Odendaal, Old Mutual Wealth Investment Strategist

In summary:

· Oil prices remain elevated as the war in Iran enters its third week

· High oil prices will weigh on South African economic growth and raise inflation

· This episode reinforces the need for South Africa to build domestic economic resilience.

Winston Churchill, a man who knew a thing about war, including from his time in South Africa, warned about the “malignant Fortune, ugly surprises, awful miscalculations” that always accompany military adventurism. Perhaps US and Israeli leaders have forgotten this as their war with Iran enters its third week.

Investors’ hopes for a speedy resolution similar to last year’s Twelve Day War have evaporated. Iran’s leadership has shown little sign of giving up the fight. It has scant hope of defeating the US militarily but can win the political battle if high fuel prices weigh on the minds of American voters leading up to the November mid-term elections. The new Supreme Leader, son of the slain Ayatollah Khamenei, said that Iran must continue to throttle maritime traffic through the Strait of Hormuz. This means as much as 20% of global oil and gas supplies are trapped. The International Energy Agency, set up to coordinate the response of Western nations to the 1970s oil shocks, called it the “largest disruption in history to oil supplies”. It arranged a release from strategic oil reserves across several countries, but the price of a barrel of Brent crude oil still ended at around $100 last week.

This will hit some countries harder than others, and the longer the war drags out, the bigger the impact will be. Russia is a big winner, especially now that sanctions on its oil sales have temporarily been eased, making Ukraine a big loser. China has been stockpiling oil for months and can ride out the storm. India, however, is far more vulnerable, being particularly dependent on natural gas. Most European nations are net energy importers, but the US is an exporter. This week we’ll focus on South Africa, an importer of crude oil and refined petroleum products.

Pain at the pump

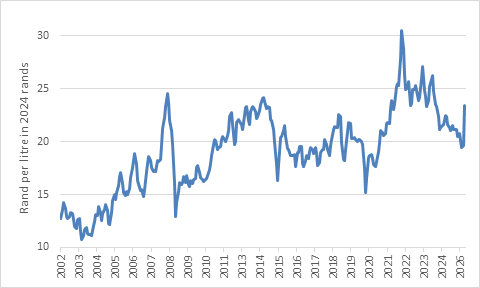

South African motorists are in for a rude shock on 1 April and it won’t be an April Fool’s joke. Retail fuel prices in South Africa adjust on the first Wednesday of each month, and data from the Central Energy Fund points to a R4 per litre increase in the petrol price and an almost R7 per litre jump in diesel. It will be the largest monthly increase this century in both cases. In a country where most people drive to work in their own cars or in minibus taxis, this will erode disposable incomes. Similarly, most goods are transported by road, not rail, and this will eat into the margins of big and small businesses. However, it should also be noted that incomes rise over time. Paying R24 per litre today is more affordable compared to five or ten years ago. Chart 1 shows that the real (inflation-adjusted) petrol price with the expected April increase will be high, but not extreme by historical standards. The worst period was the three years following Russia’s invasion of Ukraine in February 2022. Not only did the oil price surge, but the rand was particularly weak, falling from R14.55 per dollar to R19.85 at its lowest in April 2025.

Chart 1: South Africa inflation-adjusted petrol price with expected April increase

Source: Central Energy Fund, Stats SA, author’s calculations

The weakness of the rand over this period was partly due to domestic dysfunction as severe loadshedding crippled the economy, but also because the US dollar surged as the Federal Reserve increased interest rates. These two compounding factors are absent for the time being. The local economy is performing better (more on that below) and there is no indication of the Fed hiking. This is because there was a general rise in US inflation across goods and services between 2021 and 2023, not just higher energy prices. Housing inflation peaked at 8% in early 2023, as did non-housing service inflation. These two categories, accounting for 60% of the inflation basket, are currently running around 3% and are declining. The increase in energy inflation will complicate matters for the Fed, nonetheless, and it will postpone or prevent expected interest rate reductions.

The situation is similar for the SA Reserve Bank, who always notes that it doesn’t respond to the first-round effect of oil price movements, but focuses on the second round. That means monitoring “core” inflation, which excludes food and fuel, to look for signs of passthrough from petrol and diesel into other prices. Unlike the Fed, it must also take exchange rate movements into account. A weaker rand will not only exacerbate higher dollar oil prices but will also put upward pressure on a range of imported items and threaten inflation expectations. However, so far, the rand has been reasonably well behaved given how it usually reacts to negative global shocks. Part of the support comes from elevated precious metals prices, but recent days have also seen iron ore and coal prices increase.

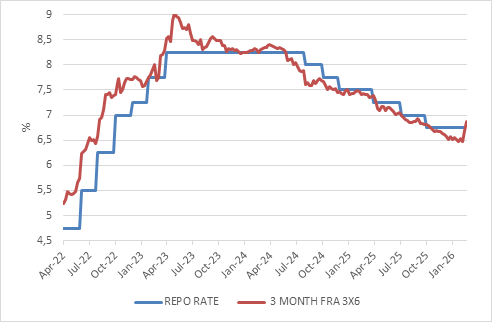

Chart 2: South Africa interest rates

Source: LSEG Datastream

Nonetheless, the rand has been on the back foot and fixed income markets have scaled back expectations for lower interest rates. In fact, the volatile forward rate agreement market is now pricing in the possibility of a rate increase, though this is still very premature. A lot would have to go wrong before the Reserve Bank considers raising interest rates, but it is highly unlikely to cut rates in the current environment. Even if oil rises further, a real possibility, it will stabilise at some point. Even if oil hits $150 dollar but stays there, its inflation rate will fall to zero after 12 months. It would be a mistake for central banks to overreact given that high energy costs tend to reduce spending on non-energy items, leading to some downward pressure on their prices.

Of interest

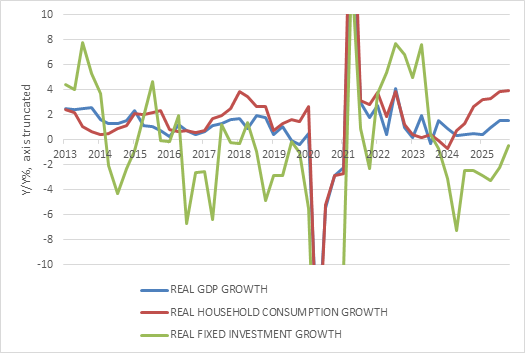

Interest rates, both the Reserve Bank’s policy rate and yields in the bond market, have already declined notably since peaking in early 2024. This contributed to solid gains in consumer spending before the war broke out. Last week’s fourth quarter gross domestic product data showed that household final expenditure grew by almost 4% year-on-year. From this high base, it was always going to moderate, but the looming cost-of-living increase will accelerate the decline.

Chart 3: South Africa economic growth

Source: Stats SA

For the overall economic growth rate to rise from the 1.5% year-on-year rate in the fourth quarter (1.1% for the full 2025 calendar year), growth in fixed investment spending must accelerate from a contraction last year to sustained growth.

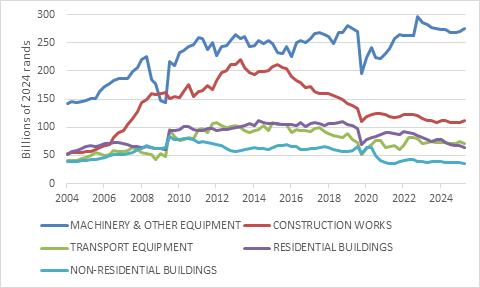

Chart 4 breaks down the components of fixed investment (formally known as gross fixed capital formation). About two-thirds of this comes from the private sector. Machinery is the biggest area by far. This includes machines used in factories and mines but also computers and more recently, equipment related to the renewable energy build-out. This has shown a general uptrend over the years and a tentative recovery over the past two quarters. The same cannot be said for the other categories. Spending on construction works has almost halved over the past decade, partly due to the completion of Kusile and Medupi, Eskom’s two much-delayed mega coalfired power stations. This category also includes roads, bridges, dams and other forms of infrastructure, and illustrates the decline of public sector capex amid budgetary pressures. Together with the decline in spending on both residential and non-residential buildings, this has decimated the construction industry, one of the most labour-intensive sectors.

Looking ahead, spending on transport equipment should rise as private freight train operators start implementing their concessions on Transnet’s rails. The residential property sector is interest rate-sensitive and will even need lower rates to get going after a decade of stagnation. Improvements in local government delivery are also necessary. The non-residential building sector is somewhat less rate-sensitive but has been held back by an oversupply in shopping malls and office buildings. The latter seems to be easing as more workers return to office (though a good way of saving on fuel costs would be for CEOs to let staff work at home over the next few months). It is the construction works category that has the biggest hope of recovering over the next few years given the concerted effort by policymakers to get partnerships with the private sector going to rebuild the country’s infrastructure. This includes the announcement last week that the World Bank will back a new Credit Guarantee Vehicle to derisk infrastructure projects for private investors, with the aim of unlocking as much as $10 billion in total spending.

Optimism versus pessimism

Across all components, boards of directors will only approve capital outlays if projects can deliver an expected return above a required hurdle rate. The decline in interest rates means the hurdle rates will also be lower. The more interest rates decline – unlikely in the short term, but realistic over the medium term – the more projects can get the green light, but only if company directors are confident about the future. As much as these decisions are guided by spreadsheets, the final call comes down to psychology. Ultimately, it depends on whether the people who make the decisions are optimistic or pessimistic about the economic outlook.

Chart 4: Components of real fixed investment spending

Source: Stats SA

The sense of optimism will be dented by the crisis in Iran but will ultimately be determined by expectations for the domestic economy. Therefore, this geopolitical episode is an urgent reminder to South African policymakers to accelerate the reforms needed to make the country a more attractive investment and business destination. As if on cue, a new analysis from the International Monetary Fund highlighted that running a business in South Africa, particularly navigating the regulatory environment, is “significantly more burdensome, fragmented, and costly than in peer economies”. The country must get its own house in order to reduce exposure to global market sentiment and geopolitical risks.

For ordinary investors, psychology also plays a big role in long-term investment success. Those who can sit through market turbulence and stick to a strategy usually outperform those who repeatedly change course. These are unsettling times and markets are likely to be volatile for some time to come. Indeed, things might even get worse before they get better, in the sense that US President Trump might only back down if the oil price is high enough to hurt him and the Republican Party politically. Similarly, Iran might only capitulate if its own oil exports are blocked, which will worsen global oil supplies. At the same time, change could come much sooner. After all, psychology also plays a big role in politicians’ decision-making. The slightest hint of good news will see markets quickly recovering. This is why trying to time the market is so fiendishly difficult, and “time in the market” is far more effective. Since we started with a Churchill quote, it will be fitting to also end with one: "You will never reach your destination if you stop and throw stones at every dog that barks".