Middle East Conflict in 2026: Implications and Positioning

By Reza Hendrickse, Portfolio Manager at PPS Investments

Geopolitical tensions in the Middle East have escalated sharply following coordinated US and Israeli strikes on Iran and Iran’s subsequent retaliation across the region. Recent developments have included attacks on military bases, energy infrastructure and heightened threats to shipping routes through the Strait of Hormuz. As with all major geopolitical events, the range of possible outcomes is wide, and the situation remains fluid. While markets have reacted swiftly, it is still too early to determine whether the conflict will escalate further or ultimately de-escalate.

Macro-economic and geopolitical considerations

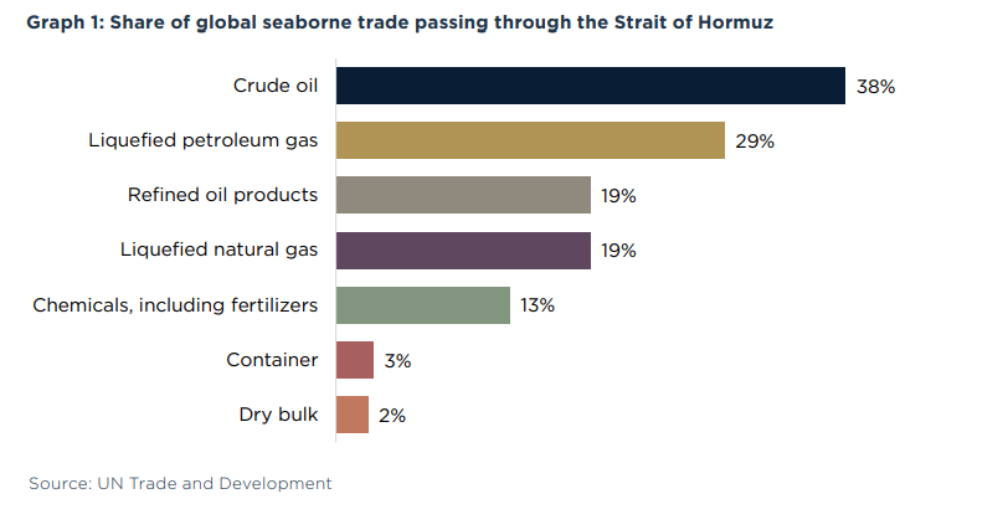

From a macro‑economic perspective, the most important variable is the oil price. History shows that conflicts in the Middle East only tend to have a sustained negative impact on global growth when they result in a material and prolonged disruption to energy supply. Chart 1 highlights the importance of the Strait of Hormuz, as a material amount of the world’s energy and fertilizer passes through it. Even without full closure, disruptions to shipping, rising insurance premiums and operational delays have a large impact.

The inflation implications are equally important. A sustained increase in oil and gas prices would place renewed pressure on global inflation, disrupting central banks’ ability to cut rates. Supply‑driven energy shocks have historically pushed headline inflation higher and, if persistent, risk feeding into second‑round effects such as wages and broader price setting behaviour. This is why markets are less focused on the initial spike in oil prices and more on the duration of the disruption.

A mitigating factor is that the global economy today is structurally less oil‑intensive than it was during previous decades, and global energy supply is more diversified. This may help limit the economic fallout if disruptions remain temporary. However, the longer shipping routes remain impaired or infrastructure remains under threat, the greater the risk that higher energy costs will weigh on household consumption, corporate margins and overall economic growth.

Global and South African Market reaction

Financial markets have reacted in a way broadly consistent with previous periods of geopolitical stress. Volatility has risen sharply, oil prices have been highly volatile, and investors have shifted toward perceived safe‑haven assets. Risk appetite has softened and the US dollar has strengthened as investors have sought relative safety. Gold prices have also been supported, while bond markets have struggled as inflation risks have been repriced higher.

Global equity markets have pulled back, with the MSCI All Country World Index now broadly flat year‑to‑date, reflecting uncertainty rather than outright pessimism. South African markets have largely mirrored these global developments. The FTSE/JSE Capped All Share Index has given back a portion of this year’s gains but remains positive year‑to‑date.

The local bond market has sold off meaningfully, with the 10‑year government bond yield rising as global risk aversion and higher oil prices have fed into inflation concerns. The rand has weakened against the US dollar, reflecting both global risk‑off sentiment and South Africa’s status as a net oil importer.

For local investors with diversified global exposure, the weaker rand has provided an important buffer. Offshore assets have declined by less in rand terms than in hard‑currency terms, once again highlighting the diversification benefits of global exposure during periods of stress.

How are we positioned

We have not made any knee‑jerk changes to portfolio positioning in response to recent events. The impact on markets has not yet been sufficient to warrant a material change in our overall risk stance.

Against this backdrop, our approach remains anchored in long‑term outcomes rather than short‑term headlines. We entered this period cautiously risk‑on relative to our strategic asset allocation, though portfolios remain well diversified across asset classes, regions and risk drivers. That said, we continue to monitor developments closely.

Our allocations to inflation‑linked bonds and global bonds help provide diversification benefits during the recent market volatility. These exposures are designed to help portfolios navigate environments where inflation risks rise and traditional asset class correlations can shift. Should South African bond yields spike further, we would look to close our current underweight, as valuations would become increasingly compelling and provide an attractive long‑term entry point.

On the equity side, markets have not yet fallen far enough to justify increasing our equity overweight at this stage. Our base case remains that volatility is likely to persist and, over time, create selective opportunities to add to risk assets where valuations are attractive. South Africa remains one such area where valuations are more supportive relative to global peers.

Conclusion

Diversification, a long‑term horizon and a clear understanding of objectives are the most effective tools for navigating uncertainty. While geopolitical events can influence short‑term market movements, long‑term investment outcomes are driven far more by maintaining a consistent strategy than by reacting to every bout of volatility.