Missiles, markets and murk

Izak Odendaal, Old Mutual Wealth Investment Strategist

In summary

- The oil price has surged in the wake of US and Israeli attacks on Iran.

- This will put downward pressure on global growth and upward pressure on inflation, but the impact depends on how long prices stay high.

- Markets are likely to be very volatile until there is some indication of the conflict easing, meaning investors will have to be vigilant and patient.

The Middle East is ablaze again. The US and Israel have attacked Iran, and it has retaliated by launching missiles and drones into neighbouring countries. This is first and foremost a humanitarian crisis, but it also has implications for the global economy. The longer the war drags on, the more pronounced the impact on economic activity. Though it seems increasingly unlikely, a speedy resolution should leave little lasting scars on key international financial metrics. Either way, Iran itself will never be the same again.

The reason why conflict in this part of the world matters so much is simply because the Middle East is the world’s biggest oil-producing region, and that includes Iran itself. Moreover, the geography of the Gulf creates a unique chokepoint in the Strait of Hormuz, a narrow maritime channel that carries about 20% of global seaborne crude. Around a hundred ships, mostly oil tankers, usually pass through the Strait every day. However, it is now effectively closed, largely because insurance companies refuse to cover vessels that travel through it.

This also impacts other goods produced in the region, such as plastics, fertilisers and aluminium. Moreover, the Gulf is a global hub for air travel, with around 500,000 passengers passing daily through the Abu Dhabi, Dubai and Qatar airports in normal times. This means that millions of travel plans have been disrupted, reaching the farthest corners of the earth. Nonetheless, oil is the key variable to watch.

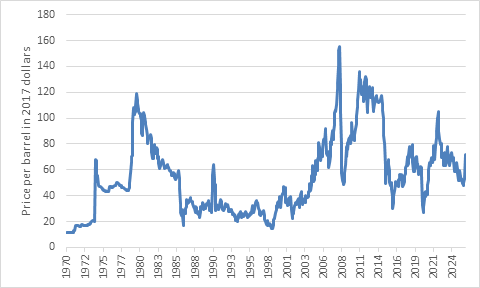

Chart 1: Brent Crude oil price adjusted for US inflation

Source: LSEG Datastream, as of 9 March 2026

Given the risks to oil supply, the spike in the price of crude is not surprising, though it is from a low base, since global oil markets appeared to be well-supplied around the start of the year. Brent crude oil jumped above $100 per barrel on Monday morning, a level last seen in 2022, but not yet extreme by historical standards when adjusted for inflation as chart 1 shows. Previous oil price spikes related to geopolitical crises were more severe, including in 1973 (Yom Kippur War), 1979 (Iranian Revolution), 1990 (Iraq invasion of Kuwait) and 2022 (Russian invasion of Ukraine). The biggest surge, leading up to 2008, was not due to war but part of the broader commodity super-cycle, and notably the narrative of “Peak Oil Supply.”

The outlook for the oil price remains very uncertain, but risks are tilted to the upside. Iran was already weakened militarily, politically and economically before the attacks and is fighting against the largest and most advanced force the world has ever known with depleting stocks of missiles. However, we’ve seen in Ukraine how an underdog can endure for longer than expected. When Iraq invaded Iran in 1980, the war lasted eight years. Moreover, even if Iran is defeated in the conventional military sense, smaller decentralised militias can carry on fighting with cheap drones, rocket launchers and speedboats, causing damage to energy infrastructure. From investors’ point of view, it is particularly worrying that there doesn’t appear to be clarity about the American war aims, making it difficult to gauge when and how the conflict might end.

This stands in contrast to the June 2025 “Twelve Day War”, when the US and Israel had the clear goal of destroying Iran’s nuclear capability and Iran chose not to escalate. An uneasy ceasefire was quickly priced in, and calm returned to financial markets. Today the market is looking for an offramp from this conflict, and none are yet in sight.

Pain at the pump

Higher fuel prices will weigh on global growth, since households and businesses will have less money to spend on other things. The longer the conflict drags on, the bigger the chance of serious damage to energy infrastructure in the region, ongoing price pressures and negative consequences for the global economy. The increased uncertainty might also result in spending decisions being postponed. As a rule of thumb, a sustained $10 per barrel increase in the oil price reduces global economic growth by about 0.1 to 0.2 percentage points. That doesn’t sound like much, but 0.1% of $100 trillion annual global economic output is a lot and will amount to lower earnings for a broad range of sectors, though of course there are winners and losers, both across industries and countries. Moreover, this heuristic does not incorporate feedback loops from financial market distress. There is a difference between a smooth $10 increase in oil prices, and a sudden spike which triggers panic selling in financial markets (more on this below).

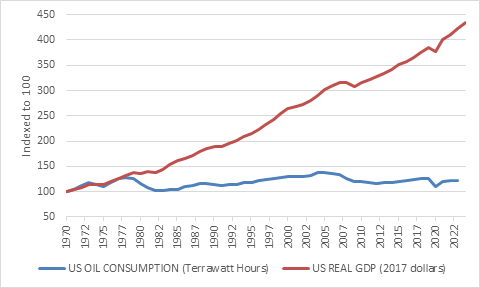

Chart 2: US oil consumption and GDP

Source: Our World in Data

Some countries will be better off than others. The US is a top oil producer, and Russia will emerge as a winner. European economies once again face an energy price squeeze, as do many Asian countries. Most of the oil and gas flowing through Hormuz headed towards the East.

Overall, it should be noted, the world uses less oil today to generate economic activity, both because of the growing importance of services and more efficient energy use. Every unit of economic activity requires much less oil today compared to the 1970s. Put differently, as chart 2 shows, the sustained increase in US real GDP over the past four decades occurred without an increase in oil consumption, with a similar picture in other countries. High real oil prices in the 1970s and again in the early 2000s encouraged efficiency, and this spike might too if it lasts. The ongoing gradual shift to renewable energy and electrified transportation will eventually reduce the dependence of the rest of the world to volatile oil-producing regions like the Middle East. Drivers of electric vehicles can already observe this episode with a bit of smugness.

Inflation

When it comes to inflation, the rule of thumb is that a $10 per barrel increase will push global inflation rates up by about 0.4 percentage points, all else equal. Again, there are many moving parts. Many countries have seen their currencies weaken, compounding the problem. The most important question, however, is how businesses respond in terms of absorbing higher fuel prices or passing them on to consumers.

Central banks will typically not react to the immediate or first-round impact of oil price changes. If oil stays around $100, it will amount to a sizable once-off increase in the price, but the oil inflation rate falls to zero after 12 months, and there is no need for a central bank to respond. They will instead focus on the second-round effects, the passthrough from higher energy costs to the prices of other goods and services. For instance, does a retailer raise the price of milk, chocolates or toilet paper because it has become more expensive to transport those goods from the warehouse to the store? If yes, there is a second-round effect that the central bank wants to clamp down on.

The most recent energy crisis, following Russia’s invasion of Ukraine four years ago, happened against the backdrop of rising demand but snarled-up supply chains worldwide as Covid lockdowns ended. In other words, there were already inflationary pressures, and firms could blame external factors when raising prices. It was a recipe for inflation, which is exactly what we got in spades. Today’s environment is different, without pent-up demand or global supply chain issues, and with central banks largely cutting interest rates. This should blunt the impact of the oil price spike.

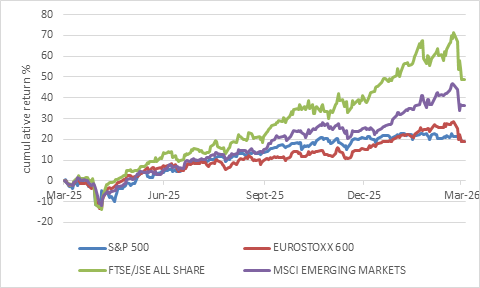

Chart 3: Global equity markets over 12 months in dollars

Source: LSEG Datastream

Bonds, barrels and bombs

Beyond oil, the initial response on financial markets was muted, presumably because investors were still anchoring off last year’s Twelve Day War. Towards the end of the week, however, hopes of a speedy resolution faded, and the reality of severe risks to global energy supplies sank in.

It is no surprise that equities fell. Not only was there an unexpected shock – after all, negotiations between the US and Iran were still underway when bombs started falling – but markets must also reprice expectations of future earnings growth. Many companies now face margin pressure from lower sales growth and higher input costs. Panic selling can quickly feed on itself, since many traders are forced to close positions or raise cash, putting further downward pressure on share prices. This is a very normal response from the equity market, especially since it comes in the wake of a strong run since April 2025.

The US dollar gained as it typically does in times of stress as investors flee to its perceived safety. Since buyers must fork out more dollars for each barrel of oil, the higher oil price also raises demand for dollars in the short term. This can compound selling in other markets, as bonds and equities and even gold are sold to raise cash.

The stronger dollar in turn weighed on the returns of equity markets outside the US, with the emerging market equities particularly hard hit during the week. Longer-term, however, this episode is likely to further confirm the growing sense that America is no longer a steady anchor in the global system, but rather a source of uncertainty. This seems bearish for the dollar.

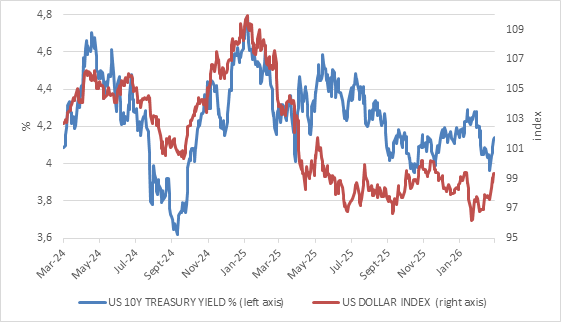

Chart 4: US 10 year and dollar

Source: LSEG Datastream

While equities behaved as expected under the circumstances, the sell-off in bonds was more of a surprise. While not dramatic, developed market bond yields still rose over the past week (bond prices and yields move in opposite directions). Historically, investors typically flee to the safety of the bond market. Not even a disappointing US employment report on Friday afternoon could support the bond market, as would normally have been the case. Rather, it appears that inflation concerns are in the driving seat for now (alongside the dash for cash described above).

Apart from the direct impact of the oil price, wars tend to be inflationary in general. They repurpose manpower and material that could be used elsewhere in the economy and destroy productive capabilities, thereby putting upward pressure on prices. Again, however, it will all depend on the scale and duration of the conflict.

Rising bond yields, a stronger dollar and weaker equity markets amount to a tightening of financial conditions, which if sustained, can weigh on economic growth even if central banks are unlikely to raise interest rates.

Closer to home, South Africa is a safe distance from the conflict but will not escape unharmed. It is an oil importer, and the country’s financial markets are very sensitive to changes in global risk appetite. The rand’s fall last week, for instance, was very typical. Indeed, given the scale of the shock, an even bigger decline would not have come as a surprise. The softer rand in turn compounds the increase in the dollar price of oil. Like other central banks, the Reserve Bank is likely to look through the immediate impact on inflation and instead monitor second-round effects. Expected interest rate cuts will be postponed but not necessarily cancelled. The one silver lining (a gold lining to be precise) is that the shifting geopolitical currents that lead to conflicts like these should provide ongoing support for precious metals prices, though these will also be volatile.

Fluid and murky

In conclusion, the situation remains fluid and the outlook murky. This newsletter might even be out of date by the time you read it. The economic and financial market effects of this crisis will depend largely on how long it lasts for, and that is unknowable at this stage. This will cause further market volatility. It is unnerving for investors, also because it is yet another signal that geopolitical order as we knew if for many decades, is over. Nonetheless, trying to time the market around these sorts of events – this is not the first and surely not the last – is likely to do more harm than good since good news might be days away, or it can take months. No one knows. The most sensible approach now is to remain patient and let diversification do its magic